Navigating retirement taxes requires shifting your focus from April 15 to a year-round schedule filled with hidden penalties. You likely spent decades mastering the standard W-2 filing season, but leaving the workforce introduces a labyrinth of distinct deadlines governing mandatory withdrawals, estimated payments, and healthcare premium surcharges. Missing these specialized cutoffs can trigger steep fines—sometimes consuming twenty-five percent of your expected distributions—and permanently inflate your Medicare costs. With the Internal Revenue Service enforcing strict timelines on retirement accounts, ignorance operates as an expensive liability. Mastering these seven easily overlooked deadlines ensures you keep your savings intact, avoid unnecessary government penalties, and optimize your cash flow during your golden years.

The Economic Snapshot: Shifting Policies and Rising Pressures

The economic landscape for retirees is shifting rapidly, driven by inflation adjustments and legislative overhauls like the SECURE 2.0 Act. The transition from earning a steady paycheck to living off accumulated assets fundamentally alters how the government calculates your tax obligations. During your career, your employer automatically deducts taxes, shielding you from continuous tax management. In retirement, that responsibility falls entirely on your shoulders. Federal data indicates growing complexity in senior finances; according to a report on the economic well-being of U.S. households, managing withdrawals efficiently operates as a primary stressor for older adults. You must synchronize your distributions with changing tax brackets and shifting penalty structures. If you fail to map out a precise annual strategy, you risk surrendering your hard-earned wealth to the government.

7 Crucial Tax Deadlines You Cannot Afford to Miss

Deadline 1: Your Initial Required Minimum Distribution

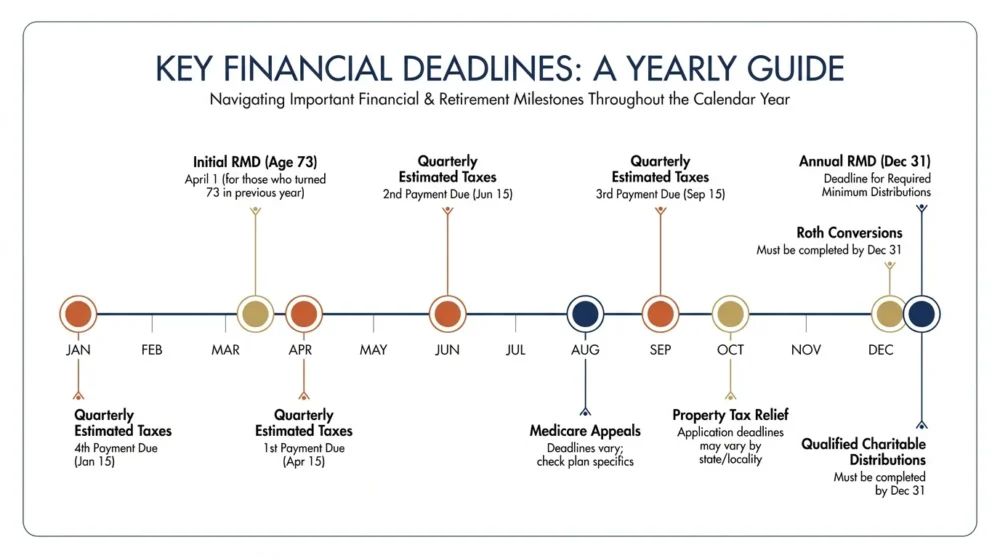

Your first mandatory distribution features a unique grace period that frequently traps new retirees in a costly tax squeeze. Under current law, you must begin taking withdrawals from traditional IRAs and 401(k)s when you reach age 73. The government grants you until April 1 of the following year to take this inaugural distribution. While delaying this initial payout defers taxes, it creates a dangerous compounding effect. If you wait until April 1, you must still take your second required distribution by December 31 of that exact same year. Forcing two substantial distributions into a single calendar year easily pushes your income into a higher tax bracket and artificially increases your overall financial burden.

Deadline 2: Annual Required Minimum Distributions

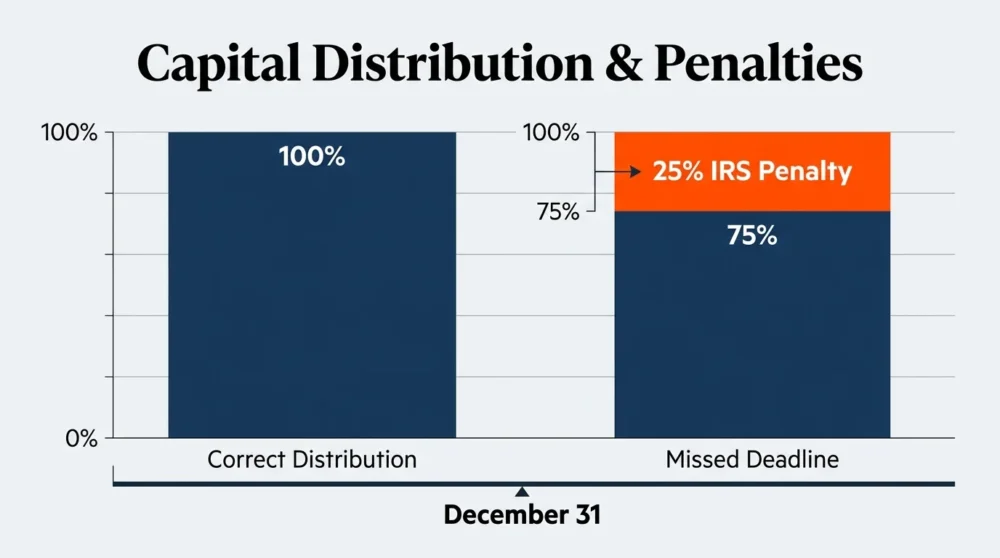

Once you navigate your first distribution, all subsequent withdrawals must exit your accounts by December 31 each year. Retirees routinely miss this cutoff due to holiday distractions or administrative delays at brokerage firms. Do not wait until the final week of December to initiate your transfer; financial institutions often require several business days to settle cash and execute trades. The federal penalty for missing this deadline dropped recently from a catastrophic fifty percent to twenty-five percent of the undistributed amount. Despite the reduction, surrendering a quarter of your withdrawal to the Internal Revenue Service remains a massive unforced error. Set up automated withdrawals early in the fourth quarter to bypass this stress entirely.

Deadline 3: Quarterly Estimated Taxes

Leaving the workforce means leaving behind automatic paycheck withholding, placing you directly into the realm of estimated tax payments. If you rely on taxable investment accounts, gig work, or business income, the government expects you to pay taxes as you earn that income. These payments fall due on April 15, June 15, September 15, and January 15. Retirees who attempt to settle their entire tax bill the following April frequently discover underpayment penalties tacked onto their balance. To protect your cash flow, estimate your annual tax liability and distribute those payments across the four quarterly deadlines. Alternatively, you can elect automatic withholding directly from your Social Security benefits to simplify your calendar.

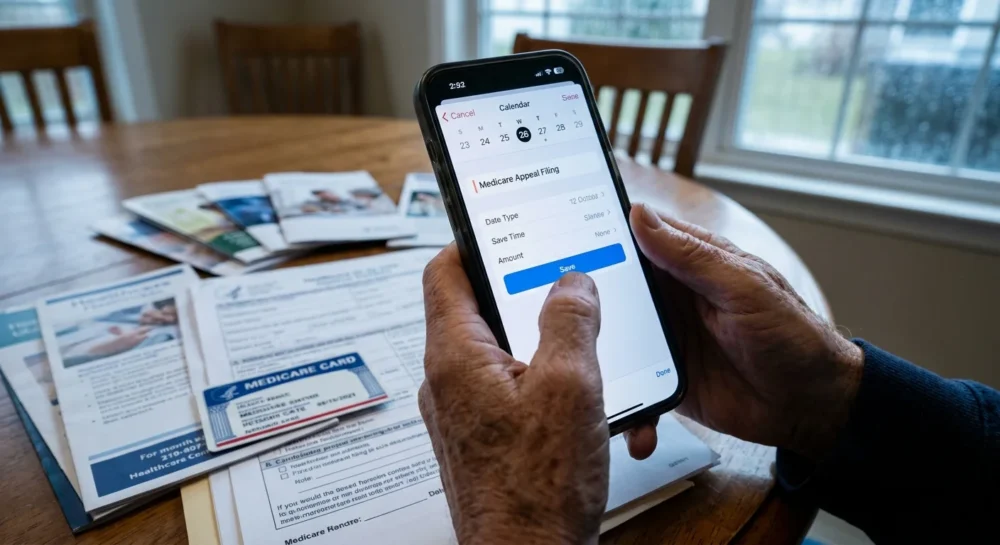

Deadline 4: Medicare Premium Appeals

The Income-Related Monthly Adjustment Amount represents a hidden tax that catches affluent retirees off guard. The government bases your Medicare premiums on your adjusted gross income from two years prior. Because of this lookback period, your premiums during your first year of retirement might reflect your peak earning years. If you experience a life-changing event—such as retiring and losing your salary—you have exactly sixty days from receiving your initial determination notice to file an appeal. Submitting Form SSA-44 allows you to bypass the surcharge. Missing this window forces you to pay inflated healthcare premiums for an entire calendar year. Follow the Social Security Administration guidelines to file your documentation immediately.

Deadline 5: Qualified Charitable Distributions

For philanthropically minded seniors, the Qualified Charitable Distribution offers a powerful strategy to lower taxable income, but the transaction must clear completely by December 31. This strategy allows you to transfer up to 105,000 dollars directly from your IRA to an eligible charity. Crucially, this satisfies your mandatory withdrawal requirement while keeping the entire amount off your adjusted gross income. Retirees often mistakenly write a personal check to a charity in late December, assuming they can reimburse themselves. That sequence ruins the tax benefit; the funds must travel directly from your custodian to the charity. Initiate your transfers by late November to guarantee settlement before the year closes.

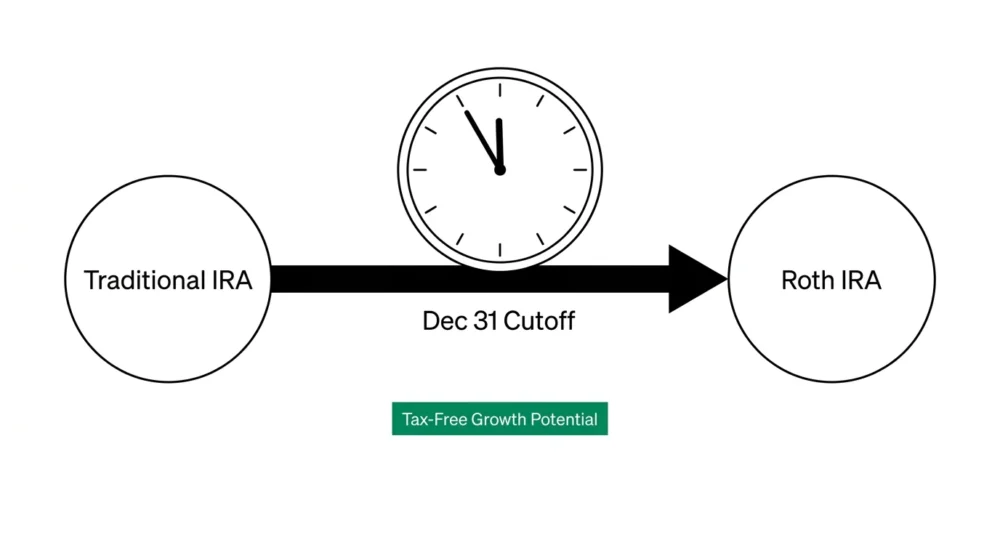

Deadline 6: Roth IRA Conversion Cutoffs

Converting traditional retirement funds to a Roth IRA provides a strategic way to lock in current tax rates and generate tax-free growth. Unlike regular IRA contributions, which you can make up until the April tax filing deadline, Roth conversions must be finalized by December 31 of the calendar year you want the conversion recorded. If you intend to execute a conversion to fill up the remainder of your current tax bracket, you must finalize your income projections and execute the transfer before the new year rings in. Proactive planning alongside a credentialed advisor ensures you execute the transfer at the most advantageous moment without missing the absolute cutoff.

Deadline 7: Local Property Tax Relief Windows

While federal taxes dominate financial planning, local property taxes pose an escalating threat to seniors living on fixed incomes. Many municipalities offer substantial property tax relief programs exclusively for residents over age 65, including assessment freezes or homestead exemptions. The deadlines to apply for these protections vary wildly by county—some land in early spring, while others align with late autumn tax assessments. Failing to submit your annual renewal paperwork instantly strips you of these protections, resulting in unexpected escrow shortages. The Consumer Financial Protection Bureau encourages older adults to actively investigate local municipal resources, as local governments rarely advertise these vital exemptions.

Strategy Pillars: Constructing a Resilient Retirement Financial Plan

Mastering tax deadlines represents just one component of a holistic retirement strategy. You must build a financial architecture that integrates cash flow management, credit optimization, and asset protection. Start by addressing your daily cash flow. Automating your tax withholdings directly from your IRA distributions acts as an invisible shield against estimated tax penalties. By treating your retirement accounts like a traditional employer that handles the withholding process on your behalf, you eliminate the stress of quarterly payments.

Your approach to debt significantly impacts your tax reality. Carrying high-interest consumer debt into retirement forces you to take larger taxable withdrawals simply to meet monthly minimums. This aggressive withdrawal strategy artificially inflates your taxable income, potentially pushing you into higher brackets. Prioritize eliminating toxic debt. Additionally, protect your portfolio from sudden market downturns right before a major tax deadline. Maintaining a cash buffer equivalent to one year of living expenses ensures you never have to liquidate equities at a steep loss to satisfy a government obligation.

Expert Voices: Professional Guidance on Senior Finance

Certified Financial Planner professionals consistently observe that the transition into retirement causes significant administrative friction for new retirees. Without a corporate human resources department handling the calendar, individuals must become their own chief financial officers. Economists and tax experts recommend implementing a forward-looking tax calendar rather than reacting retroactively every April. Professionals advise setting quarterly meetings with yourself or your advisor to project your year-end income, assess your progress toward required minimums, and evaluate whether a Roth conversion makes mathematical sense. Proactive engagement with your financial data prevents the panic of realizing you missed a critical window by just a few days. Automation and early execution provide the strongest defense against the complexities of the modern tax code.

Risk and Compliance: Dodging Scams and Navigating Tax Thresholds

The heightened stress surrounding tax deadlines creates a lucrative environment for financial fraudsters targeting older adults. Criminals frequently deploy sophisticated phishing emails and aggressive phone calls impersonating government agents. They claim you missed a mandatory filing deadline and threaten immediate asset seizure unless you pay a fine using wire transfers or digital gift cards. You must remember that the federal government never initiates contact regarding missed deadlines through threatening phone calls. Official correspondence arrives exclusively through the standard postal service.

Beyond outright fraud, you face the continuous risk of out-of-date compliance. Tax brackets, standard deductions for seniors, and withdrawal tables undergo regular adjustments. Relying on strategies from five years ago guarantees compliance failures today. Maintaining a relationship with a credentialed fiduciary or tax professional helps you navigate these evolving regulations safely and ensures your retirement assets remain thoroughly protected.

Frequently Asked Questions

Question: Can I delay my first mandatory distribution if I am still working?

Yes, under certain conditions. If you continue working past age 73 and do not own more than five percent of the company, you can generally delay withdrawals from that specific employer’s 401(k) until you officially retire. However, this exception does not apply to traditional IRAs; you must still take withdrawals from those accounts based on standard federal deadlines.

Question: How do I request federal tax withholding on my Social Security benefits?

You can establish automatic withholding by mailing Form W-4V to your local Social Security office. You can select to have seven, ten, twelve, or twenty-two percent of your monthly benefit withheld. This simple administrative step drastically simplifies your tax life and often eliminates the necessity of calculating and submitting quarterly estimated payments.

Question: Will missing a quarterly tax payment automatically result in a penalty?

Not automatically, but it is highly likely if you owe substantial taxes at year-end. The government uses a safe harbor rule. If you pay at least ninety percent of your current year tax liability or one hundred percent of your previous year tax liability through withholdings and estimated payments, you avoid the penalty. Relying on this rule requires careful calculation.

Question: What happens if I miss the sixty-day window to roll over a retirement account?

Missing the sixty-day indirect rollover window represents a critical error. The government will treat the entire distributed amount as taxable ordinary income for that year. To avoid this perilous deadline, you should always utilize a direct institution-to-institution transfer, which bypasses the sixty-day rule entirely and ensures the funds never enter your personal checking account.

Your Next Step Challenge

Translating this knowledge into protection requires immediate action. First, gather your statements and verify the exact age you must begin your mandatory distributions. Write that specific year and the corresponding April 1 deadline in your permanent financial records. Next, conduct a comprehensive audit of your income sources to determine if you need to set up quarterly estimated payments or if you can simplify your life by electing automatic withholding on your pension and Social Security benefits. Finally, reach out to your municipal tax assessor this week to secure the exact application dates for senior property tax exemptions in your county. Do not let administrative procrastination erode the wealth you spent a lifetime accumulating; take control of your tax calendar today and secure the financial independence you earned.