You can build substantial wealth without winning the lottery or securing a six-figure salary. The secret lies in making tiny, consistent financial moves that compound dramatically over time, turning spare change and strategic habits into lasting financial freedom. As stubborn living costs continue to squeeze household budgets and market volatility tests investor patience, prioritizing these incremental steps becomes your strongest defense against economic uncertainty. Instead of waiting for a sudden windfall to fix your finances, you can deploy small amounts of capital right now to optimize your cash flow, eliminate costly debt, and capture market returns. Understanding the quiet power of these accessible strategies transforms everyday financial decisions into a robust foundation for long-term prosperity.

The Economic Snapshot Squeezing Household Wealth

American households are currently navigating a turbulent financial landscape defined by elevated interest rates and unpredictable living costs. While inflation has cooled from its recent historical peaks, the cumulative effect of rising prices continues to drain discretionary income, leaving many families feeling financially paralyzed. According to recent consumer data, personal savings rates have fluctuated significantly as households redirect their earnings to cover the basic necessities of housing, food, and transportation. This persistent economic pressure often creates a psychological barrier to investing; when your monthly budget feels stretched to the absolute limit, the idea of setting aside money for the future can seem entirely out of reach.

However, this high-rate environment presents a unique dual reality for consumers. On one side of the ledger, borrowing costs for credit cards and personal loans have surged, making debt more expensive than it has been in decades. On the flip side, the exact same interest rate dynamics have created a generational opportunity for savers. For the first time in over fifteen years, risk-free savings vehicles are generating substantial, inflation-beating yields. You do not need thousands of dollars to take advantage of these economic conditions. By making targeted, calculated adjustments to how you manage your cash flow, credit, and market exposure, you can capitalize on current yields while actively insulating yourself from future economic shocks.

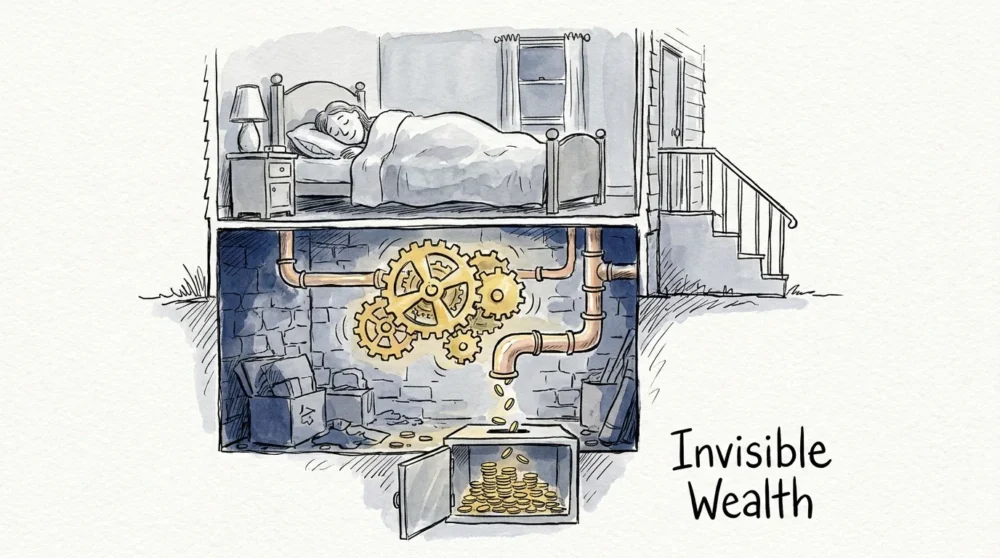

Cash Flow Strategies That Build Invisible Wealth

Optimizing your daily cash flow is the bedrock of any successful financial plan. Small tweaks to how you store and spend your money can generate surprisingly large returns without requiring any additional labor on your part.

1. Automating Transfers to High-Yield Savings

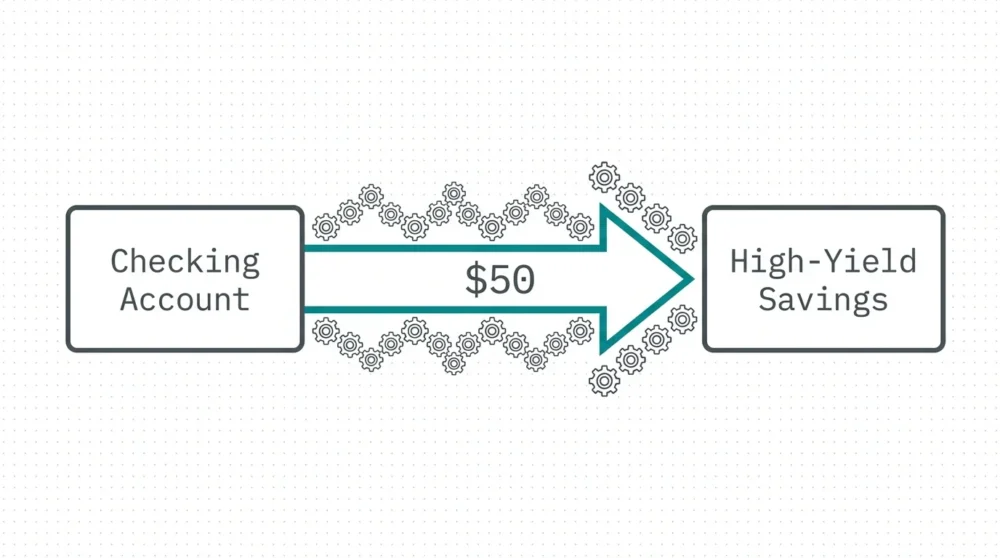

The simplest investment you can make is moving your emergency fund out of a traditional brick-and-mortar bank paying pennies in interest and into a high-yield savings account. Online banks operate with significantly lower overhead costs, allowing them to pass those savings onto you in the form of higher annual percentage yields. By setting up an automated transfer of just fifty dollars per paycheck, you create a system that pays you a passive return while shielding your cash from impulse purchases. The Federal Deposit Insurance Corporation provides guidance on ensuring these online institutions carry the same federal protections as your local branch, guaranteeing your money is entirely safe while it works for you behind the scenes.

2. Building a Certificate of Deposit Ladder

When you have cash you know you will not need for several months, tying it up in a Certificate of Deposit is a zero-risk investment that locks in current high interest rates. Instead of putting all your savings into a single long-term certificate, you can build a CD ladder by purchasing several smaller certificates that mature at different intervals. For example, buying a three-month, six-month, and nine-month certificate ensures you regularly regain access to a portion of your funds. As each certificate matures, you can either spend the cash if an emergency arises or reinvest it into a new, longer-term certificate. This strategy captures premium interest rates while maintaining a steady cadence of liquidity.

3. Investing in Energy-Efficient Home Improvements

Not all lucrative investments happen in the stock market; some of the most reliable returns are found right inside your own home. Spending a small amount of money on a smart thermostat, LED lighting, or weatherstripping for your doors and windows pays an immediate, guaranteed dividend in the form of lower utility bills. Unlike market investments, which fluctuate daily, reducing your baseline living expenses provides a permanent boost to your monthly cash flow. Over a single year, these minor hardware store purchases often pay for themselves; over a decade, they can save you thousands of dollars that can be redirected toward your retirement portfolio or debt payoff goals.

Strategic Credit and Debt Management

In an era of high borrowing costs, aggressively managing your liabilities is mathematically identical to earning a high, risk-free rate of return. Every dollar of interest you avoid paying is a dollar that stays in your pocket.

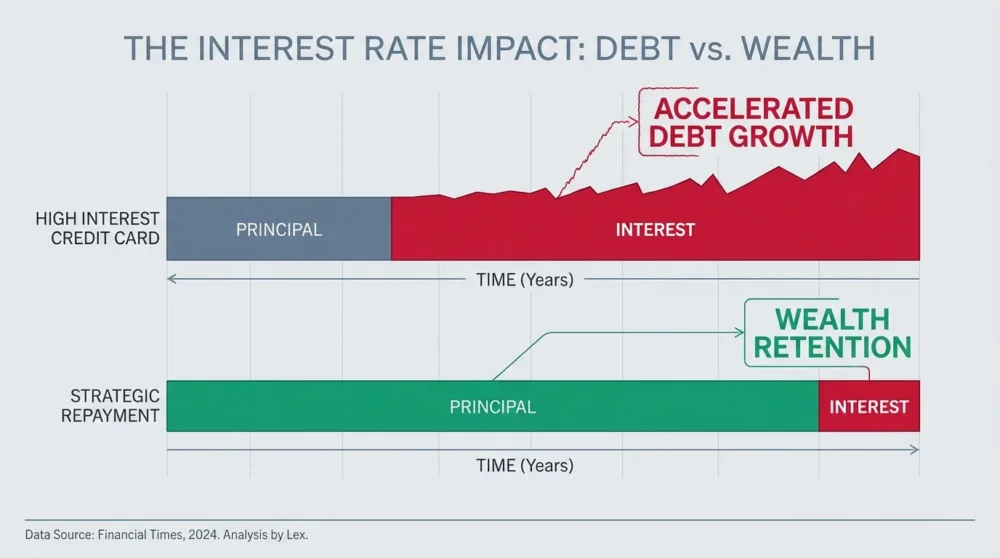

4. Making Micro-Payments Toward Debt Principal

If you carry a balance on high-interest credit cards, the math works heavily against you. Credit card companies calculate interest based on your average daily balance, which means making multiple small payments throughout the month reduces your interest burden faster than waiting to make one lump-sum payment on the due date. Funneling an extra ten dollars a week toward your principal balance might feel insignificant, but it accelerates your amortization schedule and chips away at the compounding interest. Financial planners frequently advocate for this approach because it creates psychological momentum; seeing your balance decrease in real-time keeps you highly motivated to stay on track.

5. Freezing Your Credit Reports

Protecting your financial identity requires an investment of about fifteen minutes, but it pays off by preventing catastrophic fraud. Placing a security freeze on your credit files with the three major bureaus restricts access to your data, making it nearly impossible for identity thieves to open new fraudulent accounts in your name. The Federal Trade Commission outlines the simple steps required to freeze and unfreeze your credit for free. This preventative measure acts as an invisible shield around your financial reputation, saving you from the devastating loss of time, money, and credit score points that typically accompany identity theft.

Accessible Market Investing for Long-Term Growth

Historically, the stock market has been the most powerful engine for out-pacing inflation and generating generational wealth. Today, the barriers to entry have been completely eliminated, allowing anyone to become an investor with spare change.

6. Capturing the Full Employer Match

If your workplace offers a retirement plan with matching contributions, contributing enough to secure that full match is the most lucrative small investment you will ever make. An employer match is literally free money; if your company matches your contributions up to three percent of your salary, you are earning an immediate one hundred percent return on every dollar you invest up to that limit. There is no legal investment on earth that guarantees a one hundred percent return. According to the Internal Revenue Service rules regarding retirement contributions, these funds also grow tax-deferred, meaning your money compounds faster because you avoid immediate capital gains taxation on your annual growth.

7. Utilizing Fractional Shares

A single share of a major technology company or an index fund can cost hundreds or even thousands of dollars, which historically locked everyday people out of high-quality investments. The advent of fractional share investing has revolutionized the market by allowing you to purchase a tiny slice of a stock based on a dollar amount rather than a whole share count. If you only have twenty dollars to invest, you can use a brokerage platform to buy twenty dollars worth of an index fund that tracks the S&P 500. This ensures your money is fully invested and working for you immediately, allowing you to benefit from the broader economy’s long-term upward trajectory.

Protecting Your Wealth and Earning Power

Building wealth is only half the battle; ensuring that your progress is not derailed by unexpected life events is equally crucial. Small defensive investments secure the financial foundation you are working so hard to build.

8. Securing Term Life Insurance

If anyone relies on your income to pay the rent, buy groceries, or cover debts, purchasing a term life insurance policy is a mandatory small investment. Unlike whole life insurance, which is often expensive and mixed with complex investment vehicles, term life insurance is incredibly straightforward and affordable. For a healthy individual in their thirties, a policy providing half a million dollars in coverage might cost less than a monthly streaming subscription. This tiny monthly premium transfers the catastrophic financial risk of your premature passing to an insurance company, ensuring your family will not face bankruptcy or eviction during their darkest hour.

9. Paying for Independent Financial Guidance

Navigating tax codes, investment selection, and retirement planning can quickly become overwhelming. Paying for a couple of hours with a fee-only Certified Financial Planner is a one-time investment that pays off for decades. Unlike advisors who earn commissions by selling you specific mutual funds or insurance products, fee-only fiduciaries charge a flat hourly rate to look at your entire financial picture and provide unbiased, objective advice. They can help you optimize your tax strategy, balance your portfolio, and identify blind spots in your budget. The Consumer Financial Protection Bureau advises consumers to explicitly ask about an advisor’s fiduciary status before engaging their services, ensuring your financial professional is legally bound to act strictly in your best financial interest.

Navigating Risks, Scams, and Regulatory Hurdles

As you deploy these small investments, you must remain vigilant against individuals and organizations seeking to exploit your financial ambitions. The internet is flooded with unregulated financial influencers promising guaranteed, double-digit returns through obscure cryptocurrency schemes or secret trading algorithms. You should immediately view any investment that promises high returns with zero risk as a fraudulent enterprise. Legitimate investments inherently involve some degree of risk, and historically average market returns hover around eight to ten percent annually before inflation. Anything promising significantly more is likely a scam designed to drain your hard-earned capital.

Furthermore, you must pay close attention to the regulatory limits surrounding tax-advantaged investment accounts. The government places strict annual contribution caps on Individual Retirement Accounts and workplace plans. Overcontributing to these accounts can trigger harsh tax penalties and require complex paperwork to reverse the error. You should also be aware of the tax implications of high-yield savings accounts and certificates of deposit; the interest you earn is considered taxable income and must be reported to the federal government each year. Maintaining accurate records and consulting with a qualified tax professional will ensure your wealth-building strategies remain fully compliant with all current tax laws.

Frequently Asked Questions About Small Investments

How much money do I actually need to start investing?

You can begin investing with as little as one dollar. The advent of modern brokerage applications and fractional share trading has completely eliminated minimum balance requirements. Your primary focus should be on establishing the habit of regular contributions, even if the dollar amounts are tiny. Over time, as your income grows and your budget stabilizes, you can scale up your contributions while relying on the foundational habits you have already built.

Should I prioritize paying off my debt or investing in the market?

Your strategy depends entirely on the interest rate attached to your debt. If you are carrying credit card balances with interest rates exceeding twenty percent, you should aggressively route all your spare cash toward eliminating that debt. There are no reliable market investments that will out-earn a twenty percent interest burden. However, if your only debt consists of a low-interest mortgage or manageable student loans, you can comfortably make your minimum payments while simultaneously investing in the market to capture long-term compound growth.

Are micro-investing applications safe to link to my bank account?

Yes, reputable micro-investing platforms utilize bank-level encryption to secure your data and are heavily regulated by federal authorities. You should always verify that a brokerage app is registered with the Securities and Exchange Commission and is a member of the Securities Investor Protection Corporation. This membership ensures your invested funds are protected against the failure of the brokerage firm itself, though it does not protect against normal market fluctuations and losses.

How will taxes impact the returns on these small investments?

Taxes play a significant role in your net returns. Interest earned from high-yield savings accounts and certificates of deposit is taxed as ordinary income in the year it is received. When you sell stocks or fractional shares for a profit, you will owe capital gains taxes. Holding your investments for longer than one year allows you to qualify for long-term capital gains tax rates, which are significantly lower than ordinary income tax rates. Utilizing tax-advantaged retirement accounts can legally shelter much of your growth from immediate taxation.

Your Next Step Challenge

Reading about financial optimization is intellectually satisfying, but true wealth is built through decisive action. Your challenge right now is to pick just one of the nine strategies outlined above and execute it before your head hits the pillow tonight. If you currently hold your emergency fund in a traditional bank, spend fifteen minutes opening a high-yield savings account and setting up an automatic recurring transfer. If you have workplace retirement benefits, log into your human resources portal to verify you are contributing enough to capture every single cent of your employer match.

Do not allow the pursuit of the perfect financial plan to paralyze you from making good financial progress today. Wealth building is rarely about securing massive windfalls or executing flawless market timing; it is about stringing together thousands of tiny, correct decisions over a timeline of decades. Take action on one small investment today, let the mechanics of compound interest work in the background, and watch as your quiet financial habits transform your future.