Securing enough money to live comfortably in your later years requires aggressive planning and a thorough understanding of exactly what actions destroy long-term wealth. Rising inflation and volatile markets constantly threaten your purchasing power, making it crucial to avoid the specific traps that quickly drain portfolios. Wealthy retirees maintain their financial independence by deliberately rejecting common money behaviors that ordinary investors accept as normal. By shifting your mindset and replacing these nine wealth-draining habits with data-backed strategies, you protect your assets against economic shocks and ensure your money outlasts your life expectancy. Recognizing these destructive patterns early allows you to make immediate adjustments, preserving your capital and compound growth for the decades ahead.

The Economic Snapshot: Why Retirement Planning Requires Unforgiving Discipline

The financial landscape shifts rapidly beneath the feet of modern investors. Decades ago, workers could rely on defined-benefit pension plans to provide a steady, predictable income stream from their departure from the workforce until the end of their lives. Today, the burden of funding retirement falls squarely on your shoulders through defined-contribution plans like 401(k)s and individual retirement accounts. According to data from the Federal Reserve Survey of Consumer Finances, personal wealth building now demands active, educated management rather than passive reliance on an employer.

Beyond the structural shift in how we save, macroeconomic pressures create formidable hurdles. Inflation acts as a silent tax on your purchasing power, meaning the cash you carefully saved twenty years ago buys significantly less at the grocery store today. When you combine this loss of purchasing power with increasing life expectancies, the mathematical challenge becomes clear. You are no longer saving for a brief ten-year rest period; you are funding a multidimensional lifestyle that could easily span three decades. Thriving in this environment requires you to ruthlessly eliminate inefficiencies in your budget and stop making the unforced errors that erode portfolio growth.

9 Habits Rich Retirees Completely Avoid

Habit 1: Carrying High-Interest Consumer Debt Into Retirement

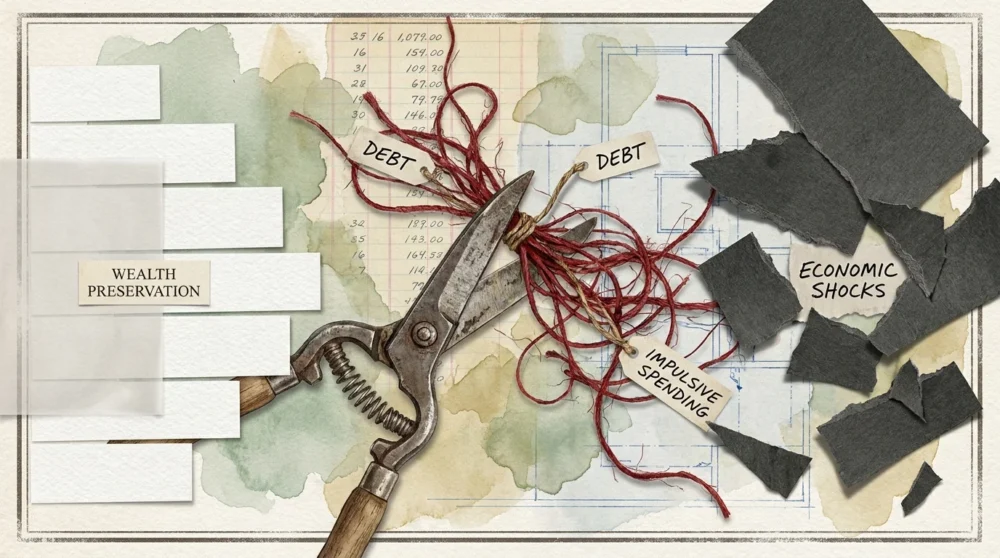

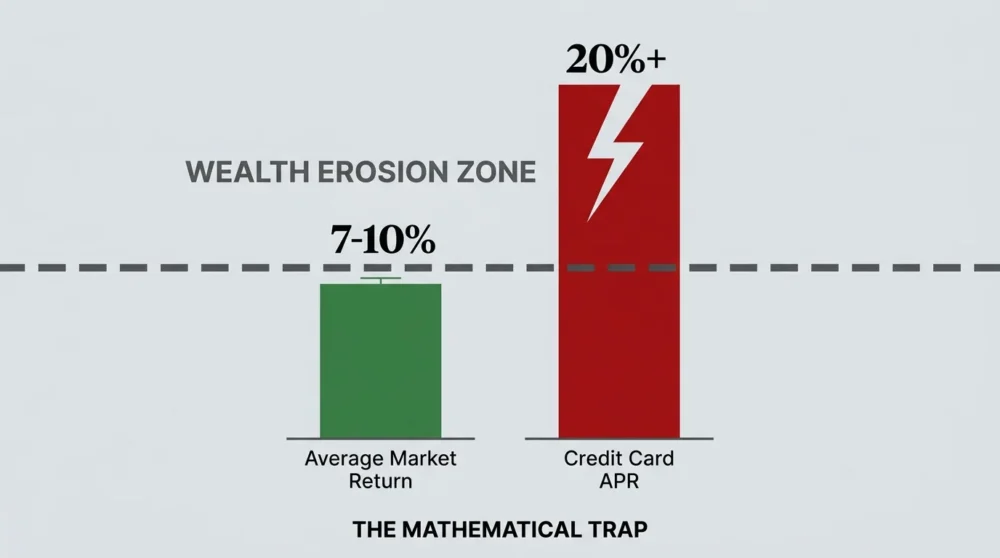

Financially successful retirees view high-interest consumer debt as a relentless emergency that must be eliminated immediately. Entering your retirement years with revolving credit card balances creates a devastating mathematical disadvantage. When you carry credit card debt at an annual percentage rate of twenty percent or higher, the interest compounds against you much faster than your investment portfolio can grow. You cannot reasonably expect to earn an average market return of seven to ten percent while simultaneously bleeding twenty percent in interest charges. Wealthy individuals aggressively pay down auto loans, personal loans, and credit card balances well before they stop working, ensuring that their fixed income goes strictly toward their lifestyle and investments rather than servicing banking fees.

Habit 2: Funding Adult Children at the Expense of Personal Security

Empathetic parents naturally want to help their children navigate early adulthood, but writing blank checks for weddings, down payments, or recurring living expenses destroys retirement timelines. Successful retirees understand the airplane oxygen mask principle—you must secure your own financial stability before attempting to rescue anyone else. When you pull money out of your investment accounts to fund an adult child’s lifestyle, you lose the initial capital and the decades of compound growth that money would have generated. If you exhaust your retirement savings trying to act as the family bank, you ultimately become a financial burden to your children in your later years. Generosity must always remain within the strict boundaries of your comprehensive financial plan.

Habit 3: Underestimating the True Cost of Modern Healthcare

Assuming that Medicare covers all medical expenses is a dangerous misconception that frequently bankrupts unprepared seniors. The Bureau of Labor Statistics tracks medical care inflation, revealing that healthcare costs historically outpace the general inflation rate by a significant margin. Medicare features premiums, deductibles, co-pays, and strict limitations on coverage—particularly excluding routine dental care, vision, hearing aids, and crucially, long-term custodial care. Affluent retirees anticipate these massive expenses by heavily funding Health Savings Accounts during their working years, investing the contributions, and letting them grow tax-free. They also run detailed projections to ensure their portfolios can withstand the shock of unexpected medical emergencies without liquidating core assets.

Habit 4: Falling for the Allure of Speculative Investments

You will never find a financially secure retiree risking their core nest egg on unpredictable stock tips, volatile cryptocurrency schemes, or speculative real estate ventures pitched at dinner seminars. Building and preserving wealth requires profound boredom; it relies on consistent, diversified investments in broad market index funds rather than attempting to strike it rich overnight. Speculative investments carry an exceptionally high risk of total capital loss, an outcome that is impossible to recover from when you no longer have a salary to replenish your accounts. Rich investors protect their capital by adhering to strict asset allocation models, prioritizing reliable dividend growth and steady market returns over the adrenaline rush of chasing the next big trend.

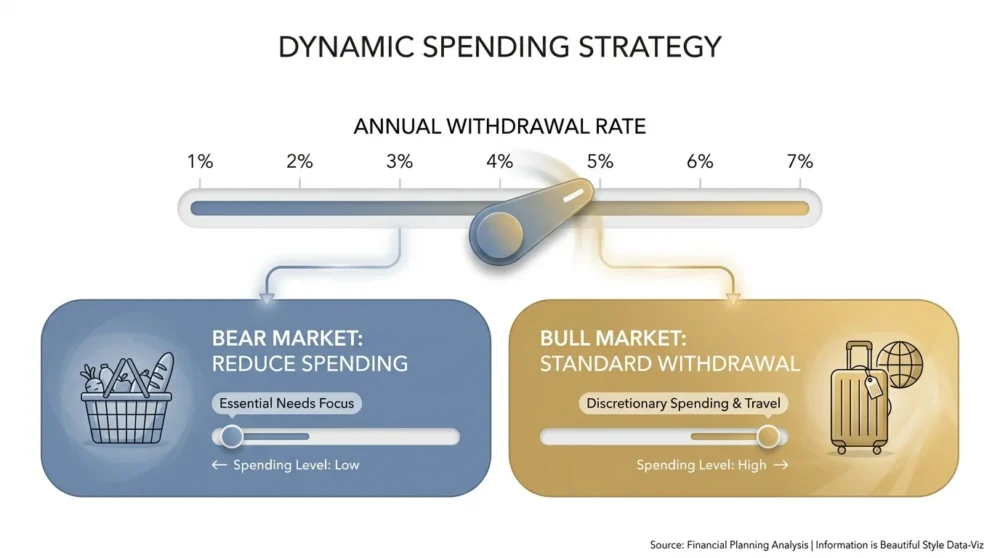

Habit 5: Remaining Rigid With Annual Withdrawal Rates

For years, the financial industry popularized the four percent rule, suggesting you could safely withdraw four percent of your portfolio in your first year of retirement and adjust for inflation annually. However, blindly following this rule regardless of market conditions is a habit wealthy individuals avoid. They understand the concept of sequence of returns risk—the danger of experiencing a severe market downturn in the early years of retirement. If you withdraw a fixed amount while your portfolio is drastically down, you are forced to sell a larger number of shares, permanently damaging the portfolio’s ability to recover. Instead, agile retirees employ dynamic withdrawal strategies, tightening their belts and reducing withdrawals during bear markets to preserve their capital.

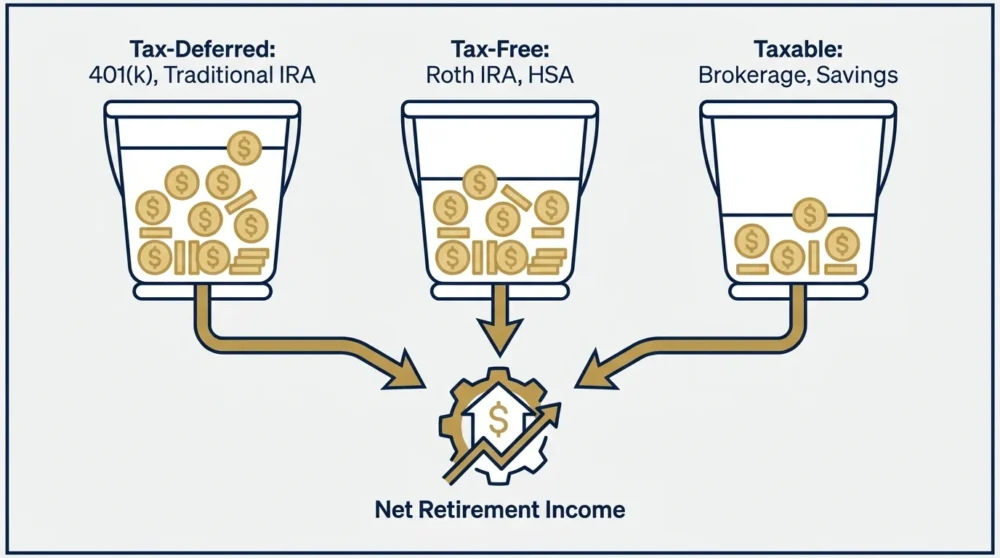

Habit 6: Ignoring the Mechanics of Tax Diversification

Taxes represent one of your largest expenses in retirement, yet ordinary investors rarely plan for them until it is time to file their returns. Keeping all your savings in traditional, tax-deferred accounts creates a massive impending tax liability. When the government forces you to take distributions, the resulting income spike can push you into a higher tax bracket and trigger Medicare premium surcharges. Wealthy retirees proactively build tax diversification by utilizing a strategic mix of traditional IRAs, Roth IRAs, and standard taxable brokerage accounts. This deliberate structuring allows them to control exactly how much taxable income they report each year, keeping their tax obligations mathematically optimized. Understanding the IRS regulations on required minimum distributions prevents unnecessary penalty taxes.

Habit 7: Holding Disproportionate Amounts of Cash on the Sidelines

While maintaining a robust emergency fund provides vital psychological comfort, hoarding an excessive amount of cash destroys your purchasing power over time. Inflation constantly erodes the value of stagnant money; a dollar sitting in a zero-interest checking account loses a fraction of its utility every single month. Financially savvy retirees keep a precisely calculated amount of cash—typically enough to cover one to two years of living expenses—in high-yield savings accounts or short-term treasury bills. Every dollar beyond that designated safety net is aggressively deployed into investments that outpace inflation. They view excessive cash not as safety, but as a guaranteed long-term loss.

Habit 8: Permitting Unchecked Lifestyle Creep

An increase in net worth should not automatically trigger a corresponding increase in luxury spending, yet many people inflate their lifestyles every time their portfolio jumps. Upgrading to massive luxury vehicles, expanding into larger homes that require exorbitant maintenance, and frequently dining at high-end restaurants quickly drain capital that should be compounding. Rich retirees master the art of deliberate spending. They purchase reliable vehicles and drive them for a decade, they downsize their primary residences to lower property taxes and utility costs, and they ruthlessly cut expenses that do not bring them genuine joy. Their financial independence stems from keeping their overhead low, regardless of how large their brokerage accounts grow.

Habit 9: Neglecting Essential Estate and Beneficiary Updates

Failing to explicitly dictate what happens to your assets upon your death creates chaos, legal battles, and massive tax burdens for your surviving family members. Ordinary investors frequently draft a simple will and assume the task is complete, oblivious to the fact that beneficiary designations on retirement accounts and life insurance policies legally override whatever is written in a will. Wealthy retirees treat estate planning as a living, breathing component of their financial strategy. They establish revocable living trusts to bypass the costly and public probate process, and they review their beneficiary designations annually to ensure the documents align perfectly with their current family dynamics.

Strategy Pillars for Lasting Wealth Building

Mastering Cash Flow Management: The foundation of all financial independence rests on knowing exactly where your money flows. You must track your expenses meticulously and automate your savings. Treat your monthly investment contributions with the same urgency as a mortgage payment, removing the temptation to spend the money before it reaches your brokerage account.

Optimizing Credit Usage: Use credit cards exclusively as a tool for security and rewards, never as a crutch for overspending. Pay your statement balances in full every single month to avoid interest charges. This disciplined approach builds an elite credit score, which lowers your insurance premiums and guarantees the best possible terms if you ever need to finance a strategic real estate purchase.

Deploying Strategic Investments: Asset allocation dictates your success. Build a globally diversified portfolio using low-cost index funds or exchange-traded funds. Balance your equities with fixed-income assets based on your specific timeline and risk tolerance, intentionally ignoring the daily noise of the financial news cycle.

Implementing Bulletproof Protections: One lawsuit or medical crisis can wipe out decades of diligent saving. Shield your wealth by purchasing adequate term life insurance, maintaining comprehensive health coverage, and securing a personal liability umbrella policy. Protecting your downside risk guarantees that your wealth-building trajectory remains uninterrupted by unforeseen disasters.

Expert Voices on Maintaining Financial Readiness

Certified Financial Planner professionals consistently emphasize that successful retirement requires behavioral discipline far more than complex mathematical formulas. The true value of working with a fiduciary advisor lies in having an objective third party step in to prevent you from making emotional decisions during market panics. Economists regularly point out that investors who attempt to time the market invariably miss the best performing days, permanently stunting their portfolio’s growth. The consensus among financial experts is clear: those who build lasting wealth focus entirely on the variables they can control—their savings rate, their asset allocation, their tax strategies, and their investment fees—while accepting that market volatility is simply the price of admission for long-term gains.

Risk and Compliance: Defending Your Nest Egg

As you accumulate wealth, you inevitably become a target for sophisticated financial scams and aggressive marketing tactics. The Consumer Financial Protection Bureau data on elder financial exploitation highlights the alarming frequency with which older Americans are defrauded through wire scams, phantom debt collection, and fraudulent investment pitches. Defending your nest egg requires acute skepticism. Never provide personal information over the phone to inbound callers, freeze your credit reports at all three major bureaus to prevent identity theft, and verify the credentials of any financial professional before signing a contract. Additionally, you must stay vigilant regarding banking limits. Ensure your cash reserves remain fully protected under the legal FDIC deposit insurance rules, utilizing multiple banking institutions if your liquid cash exceeds the federal insurance thresholds.

Frequently Asked Questions

How much cash should a retiree realistically keep on hand?

The exact amount depends heavily on your fixed income sources and personal risk tolerance, but a robust baseline involves keeping one to three years of basic living expenses in liquid, high-yield accounts. This strategic cash buffer prevents you from having to sell off your stock investments during a market crash just to pay for groceries or keep the lights on.

Is it mathematically beneficial to pay off a mortgage before retiring?

The decision to pay off a mortgage blends mathematics with psychology. If your mortgage carries a rock-bottom interest rate of three percent, investing that extra cash in the market typically yields a higher mathematical return over time. However, eliminating your largest monthly expense dramatically lowers your required withdrawal rate in retirement, providing profound psychological relief and significantly reducing your sequence of returns risk.

How do I assist my adult children without sabotaging my own retirement?

You must prioritize your own financial independence first. If you choose to provide assistance, do so through structured, non-recurring gifts rather than ongoing monthly subsidies. Offer to match their IRA contributions or help fund a one-time educational expense, explicitly communicating that this support will not compromise your core retirement assets. Never co-sign loans or drain your 401(k) to solve their temporary financial hurdles.

What are the consequences of missing a required minimum distribution?

Failing to take your required minimum distribution from tax-deferred accounts triggers a steep excise tax enforced by the IRS. Historically, this penalty was fifty percent of the amount not withdrawn, though recent legislative changes have reduced this rate. If you miss a distribution due to a reasonable error, you must immediately take the required amount and file a specific IRS form to request a penalty abatement, providing a detailed explanation of the oversight.

Your Immediate Action Plan

Reading about financial discipline provides no benefit unless you translate that knowledge into immediate, deliberate action. Within the next forty-eight hours, pull up your banking and investment dashboards and conduct a ruthless audit of your recurring expenses, canceling subscriptions and memberships that drain your cash flow. Next, log into your workplace retirement portal and your personal brokerage accounts to verify that your beneficiary designations perfectly match your current intentions. Finally, scrutinize your credit card statements to ensure you are not carrying balances that charge exorbitant interest rates, and redirect any idle cash sitting in zero-interest checking accounts into a high-yield savings vehicle or broad market index fund. Taking these definitive steps today fortifies your financial foundation, allowing you to build the resilient, lasting wealth required for a stress-free retirement.