Securing a comfortable retirement means knowing exactly which costly financial products to avoid, as hidden fees and complex structures can easily drain your lifetime savings. While U.S. households work diligently to balance daily budgets against long-term investing goals, the financial industry markets dozens of retirement vehicles designed more for broker commissions than your wealth growth. Economic pressures and changing tax policies make every dollar critical, demanding you scrutinize the tools promising guaranteed returns. By examining the specific investments that credentialed financial planners refuse to put in their own portfolios, you gain a practical roadmap to protect your hard-earned assets. Shedding these toxic products ensures your capital works efficiently, giving you the financial freedom you actually deserve.

The Economic Realities Squeezing Retirement Savings

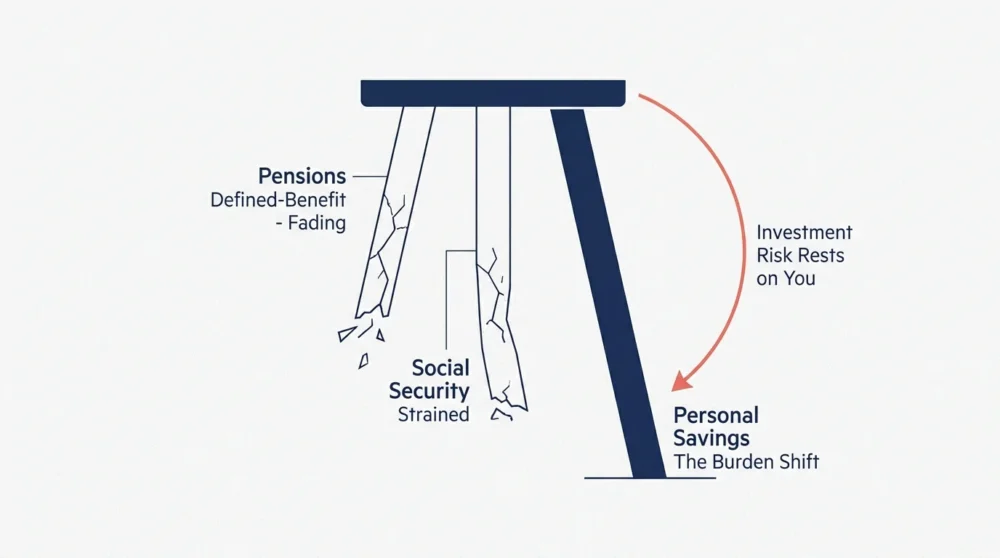

Modern retirement planning requires navigating a landscape vastly different from the one your parents experienced. The traditional three-legged stool of retirement—pensions, Social Security, and personal savings—has wobbled severely. With the shift from defined-benefit pensions to defined-contribution plans like the 401(k), the entire burden of investment risk now rests squarely on your shoulders. This monumental shift creates fertile ground for financial salespeople pitching products that promise safety but actually erode your purchasing power over time.

Recent economic data highlights exactly why protecting your capital matters more than ever. Persistent inflation continues to pressure household budgets, forcing many families to juggle credit card debt payoff alongside their retirement contributions. According to Federal Reserve data on household retirement readiness, a significant portion of non-retirees feel behind on their savings goals. When you feel behind, you become vulnerable to aggressive marketing campaigns touting guaranteed income or market-beating returns. Financial planners see the aftermath of these purchases daily: portfolios weighed down by illiquid assets, exorbitant surrender charges, and massive underperformance compared to simple benchmark indexes. Understanding what the experts refuse to buy provides you with a powerful shield against wealth-destroying mistakes.

Product 1: Variable Annuities with Excessive Riders

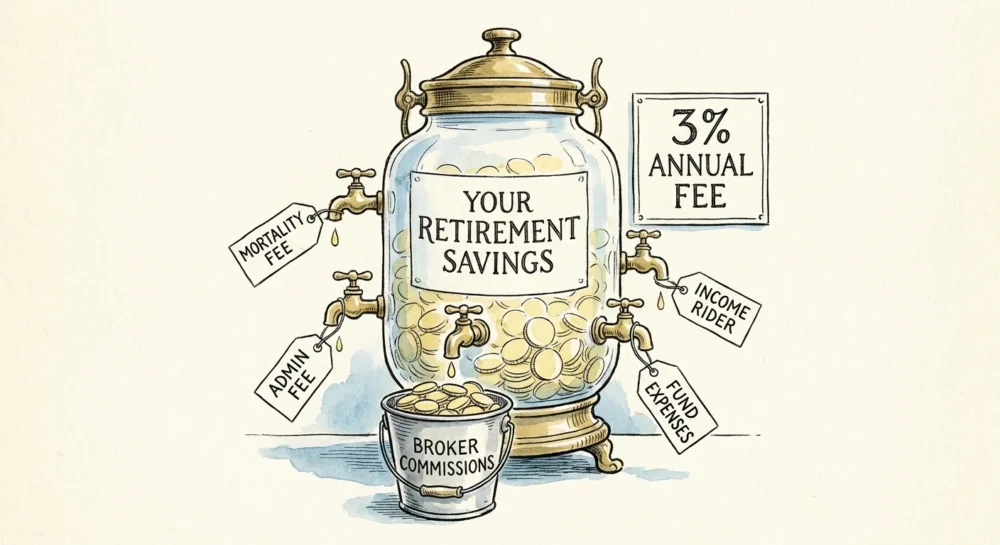

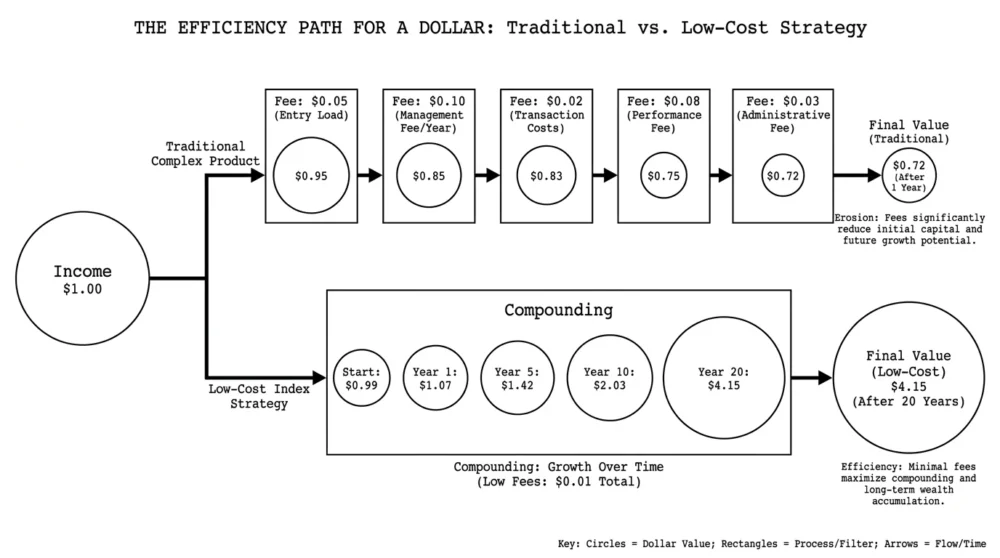

A variable annuity is an insurance contract where your premiums are invested in sub-accounts similar to mutual funds, with payouts dependent on market performance. Salespeople often pitch them heavily by tacking on income riders that promise a guaranteed minimum withdrawal benefit. Certified Financial Planner professionals routinely avoid these products due to their staggering fee structures. When you combine mortality and expense charges, administrative fees, underlying fund expenses, and the cost of the income riders, total annual fees frequently exceed three percent. Losing three percent of your portfolio every year to fees mathematically decimates your compound growth over a two-decade retirement.

Beyond the excessive fees, variable annuities lock up your cash flow through steep surrender charges. If you face a medical emergency and need to withdraw your funds in the early years of the contract, the insurance company will penalize you heavily—sometimes taking up to ten percent of your withdrawal. Financial experts prefer managing market risk through a diversified portfolio of low-cost index funds and reliable fixed-income securities, maintaining total liquidity without paying a middleman for an expensive guarantee.

Product 2: Non-Traded Real Estate Investment Trusts

Real estate provides excellent portfolio diversification, but non-traded Real Estate Investment Trusts represent a highly inefficient way to access this asset class. Unlike publicly traded REITs bought and sold on the stock exchange throughout the day, non-traded REITs do not trade on a secondary market. This structure creates an enormous liquidity trap. If you need your money back quickly to cover unexpected retirement expenses, you simply cannot sell your shares without jumping through bureaucratic hoops and accepting a discounted redemption price.

Furthermore, the upfront costs for non-traded REITs routinely range between ten and fifteen percent. If you invest a hundred thousand dollars, up to fifteen thousand dollars immediately disappears to cover broker commissions and organizational fees before a single dime goes toward purchasing property. The Securities and Exchange Commission guidance on non-traded REITs consistently warns retail investors about these high upfront costs and the difficulty of valuing the underlying assets. Experts choose low-cost, publicly traded real estate index funds instead, keeping their principal fully invested and completely liquid.

Product 3: Proprietary Mutual Funds

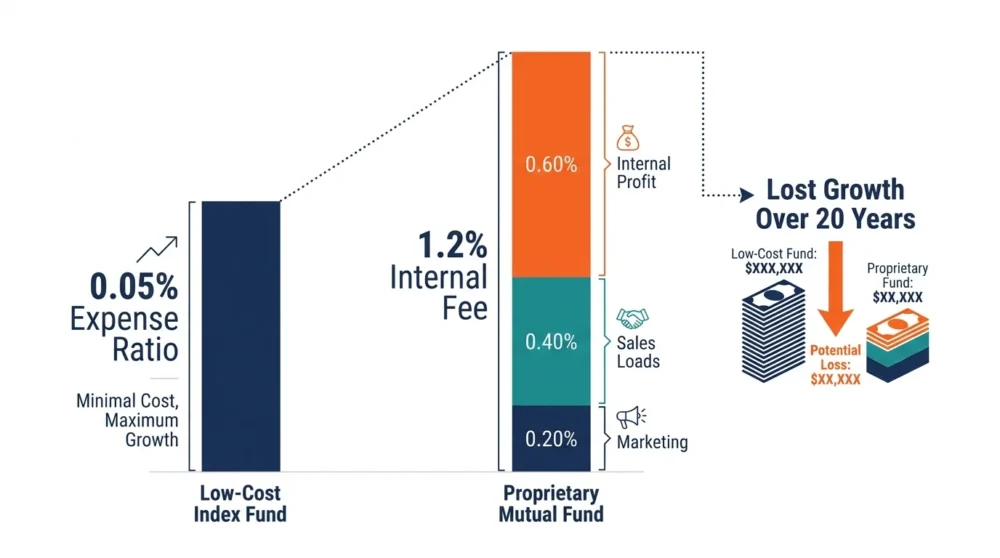

When you walk into a large, brand-name brokerage firm, the advisor will likely recommend a suite of mutual funds managed in-house by their own institution. These proprietary mutual funds present a massive conflict of interest. The advisor receives incentives, higher payouts, or pressure from management to steer your retirement capital into the firm’s own products rather than recommending the absolute best funds available on the open market.

Proprietary funds frequently carry elevated expense ratios and 12b-1 fees, which are ongoing charges passed onto you strictly to cover the fund’s marketing and distribution costs. Financial experts refuse to pay a fund to market itself to other people. Instead, independent advisors build portfolios using open-architecture platforms, selecting the lowest-cost, most efficient exchange-traded funds and mutual funds from across the entire industry, regardless of which company manages them.

Product 4: Whole Life Insurance for Pure Investment

Insurance agents continually market whole life insurance as a dual-purpose retirement vehicle, promising a death benefit paired with a tax-advantaged cash value accumulation account. While permanent insurance has niche utility for ultra-high-net-worth estate tax planning, it serves as a remarkably poor retirement investment for the average U.S. household. The premiums for whole life policies cost vastly more than a comparable term life policy, often draining cash flow that you could otherwise direct toward a 401(k) or Roth IRA.

The internal rate of return on the cash value component of a whole life policy typically lags far behind the broader stock market, especially during the first decade when commissions and administrative costs consume almost all your premium payments. Financial experts follow a much simpler, more profitable strategy: buy cheap term life insurance to protect your family during your working years, and invest the massive difference in premiums directly into low-cost index funds. This strategy separates your wealth-building mechanism from your risk-management tools, providing greater flexibility and significantly higher lifetime returns.

Product 5: Target-Date Funds with High Expense Ratios

Target-date funds offer a fantastic set-it-and-forget-it strategy for retirement investors, automatically shifting from aggressive stocks to conservative bonds as you age. However, experts strictly avoid actively managed target-date funds with high expense ratios. Some fund families build their target-date portfolios by bundling together their most expensive, actively managed mutual funds, resulting in an aggregate expense ratio that eats away at your long-term gains.

A target-date fund charging an expense ratio of point-seven-five percent drains vast sums of money over thirty years compared to an index-based target-date fund charging point-zero-eight percent. Financial professionals exclusively utilize target-date funds built on a foundation of passive index funds. When reviewing your workplace retirement plan, you must look under the hood of your target-date fund to ensure you are paying for efficient asset allocation rather than subsidizing a team of active managers attempting to beat the market.

Product 6: Complex Structured Notes

Structured notes represent unsecured debt obligations issued by major financial institutions, with returns linked to the performance of an underlying asset, index, or derivative strategy. Banks market them aggressively as a way to capture market upside while maintaining downside protection. Financial experts refuse to touch them due to their extreme opacity, high embedded fees, and immense credit risk.

When you purchase a structured note, you do not actually own the underlying stocks or indexes; you simply hold a promise from the issuing bank to pay you back according to a complex formula. If the issuing bank goes bankrupt, you become an unsecured creditor and could lose your entire investment, regardless of how well the stock market performed. The pricing formulas heavily favor the issuing bank, allowing them to extract hidden fees before determining your final payout. Experts prefer straightforward investments where the relationship between risk and reward remains transparent and easily measurable.

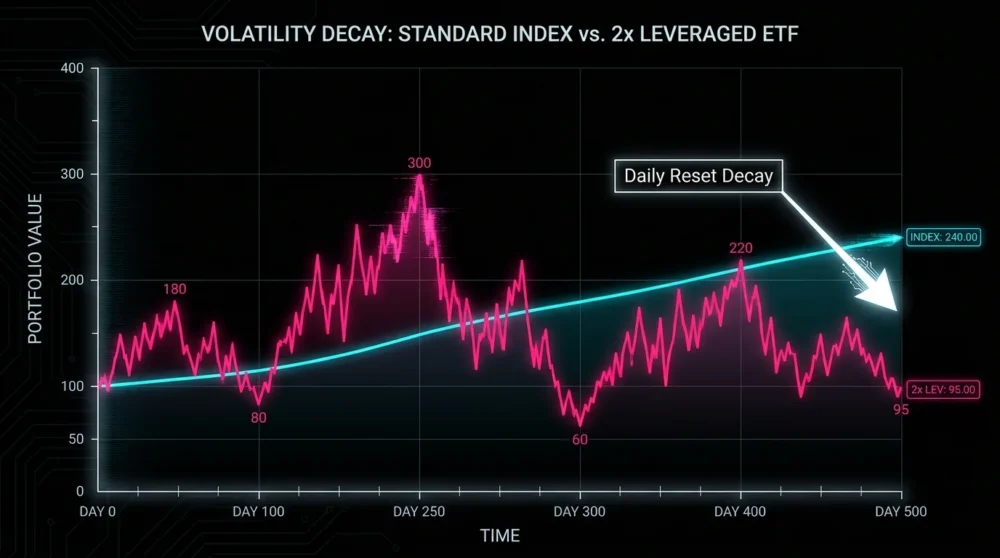

Product 7: Leveraged and Inverse ETFs

Exchange-traded funds revolutionized retirement investing by lowering costs, but the financial industry quickly created toxic variations designed for day traders. Leveraged ETFs use financial derivatives and debt to amplify the returns of an underlying index, while inverse ETFs attempt to deliver the exact opposite return of a benchmark. These products reset their exposure on a daily basis, making them mathematically disastrous for long-term retirement holds.

Due to the compounding effect of daily resets and the high cost of the underlying derivatives, a leveraged ETF will almost certainly deviate significantly from its benchmark over a period of months or years. You can easily lose money holding a leveraged bull ETF even if the underlying index eventually goes up. The SEC alerts regarding leveraged exchange-traded funds emphasize that these products require daily monitoring and are entirely unsuitable for a buy-and-hold retirement portfolio. Experts leave these highly volatile instruments to institutional traders and speculators.

Product 8: Timeshares Sold as Retirement Assets

Sales presentations frequently frame vacation timeshares as an investment in your future retirement lifestyle, locking in today’s prices for tomorrow’s vacations. In reality, timeshares represent a depreciating liability that rapidly drains your available cash flow. The upfront purchase price is only the beginning; the true financial damage comes from the rapidly escalating, perpetual maintenance fees you must pay every single year, regardless of whether you actually use the property.

Timeshares possess practically zero resale value. The secondary market is flooded with desperate owners willing to sell their timeshares for a single dollar just to escape the crushing burden of the annual maintenance contracts. Committing a portion of your fixed retirement income to an inescapable, rising liability violates every principle of sound financial planning. Experts recommend renting vacation properties as needed, preserving your capital and maintaining the flexibility to travel wherever and whenever you desire.

Product 9: Gold IRAs with Astronomical Markups

Precious metals can serve as a minor hedge against inflation, but the aggressively marketed Gold IRA industry operates on a business model that strips wealth from unsuspecting retirees. Television and radio advertisements use economic fearmongering to convince you to roll over your entire 401(k) into a self-directed IRA filled with physical gold and silver coins. While holding physical gold in a retirement account is technically legal, the hidden costs make it a mathematically dreadful choice.

Gold IRA companies routinely charge exorbitant spreads, selling you coins at markups wildly above the actual spot price of the metal. Furthermore, IRS regulations require you to store the physical metals in an approved depository, subjecting you to ongoing storage fees, insurance costs, and administrative custodial charges that do not exist with standard stock and bond portfolios. Financial professionals seeking gold exposure simply purchase a low-cost gold exchange-traded fund, entirely bypassing the predatory dealer markups and recurring storage fees.

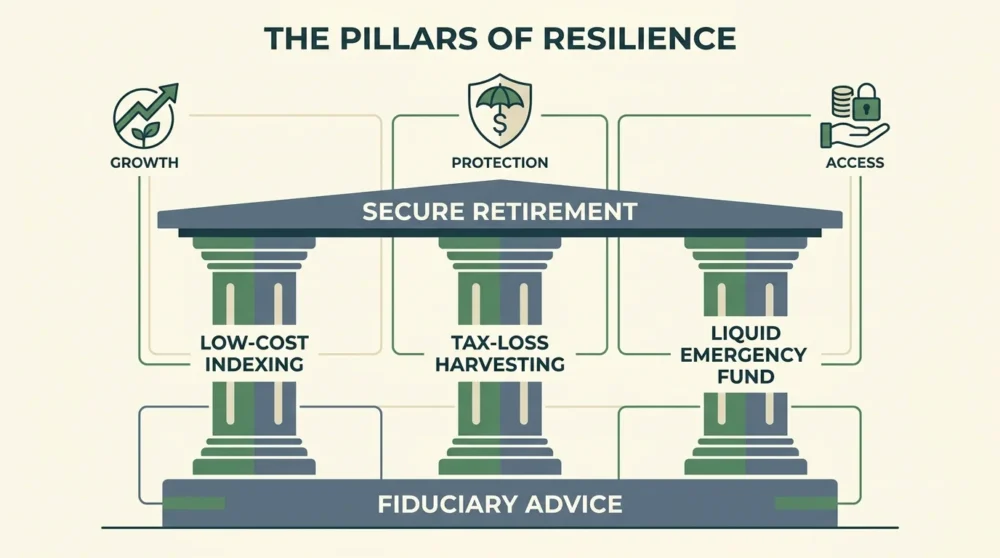

Strategy Pillars for a Resilient Retirement Portfolio

Understanding what to avoid represents only half the battle. To build a robust financial foundation, you must implement proactive strategies that align with your long-term goals. Financial experts rely on three specific pillars to generate wealth, manage risk, and maintain optimal cash flow throughout retirement.

Optimizing Cash Flow and Credit

Your ability to invest heavily depends entirely on managing the gap between your income and your expenses. Prioritize the aggressive elimination of high-interest consumer debt, such as revolving credit card balances and expensive auto loans. Paying off a credit card that charges twenty percent interest delivers an immediate, guaranteed twenty percent return on your money—a feat no legitimate investment product can match. Once you eliminate high-interest debt, redirect those monthly payments directly into your retirement accounts, effectively turning your past debt obligations into future wealth.

Building Efficient Investment Strategies

A successful retirement portfolio relies on simplicity, broad diversification, and relentless cost control. Experts construct their personal portfolios using low-cost, broad-market index funds and exchange-traded funds. By capturing the return of the entire global stock market and balancing it with high-quality government and corporate bonds, you eliminate the single-company risk that comes from picking individual stocks. Keeping your overall portfolio expense ratio below point-one-five percent ensures that the vast majority of your compound growth remains in your account rather than bleeding out to fund managers.

Ensuring Appropriate Financial Protections

Risk management remains critical, but you must decouple your insurance needs from your investment accounts. Maintain a liquid emergency fund holding three to six months of living expenses in a high-yield savings account or a money market fund. This cash buffer prevents you from selling your investments at a loss during a market downturn just to cover a sudden medical bill or home repair. For life insurance needs, secure a highly affordable term life policy to replace your income and protect your dependents until you reach financial independence.

Navigating Risk, Scams, and Compliance

The financial services industry operates under a complex web of regulations that dictate how advisors can sell products. Many salespeople adhere only to a “suitability” standard, meaning they can legally sell you an expensive, mediocre product as long as it generally fits your profile. Conversely, professionals acting as fiduciaries are legally bound to place your financial interests above their own compensation.

Always demand a fiduciary relationship when seeking retirement advice. Scams and predatory products thrive in environments where fee structures remain opaque. The Consumer Financial Protection Bureau resources on retirement planning provide excellent frameworks for evaluating financial advice and spotting the red flags of predatory sales tactics. Before signing any contract or rolling over your hard-earned assets, verify the disciplinary history and exact credentials of your broker using the free FINRA BrokerCheck database. If a professional refuses to disclose their exact commission structure in writing, you must walk away immediately.

Frequently Asked Questions About Retirement Products

How do I know if I already own one of these toxic financial products?

You can identify these products by thoroughly reviewing your account statements, trade confirmations, and product prospectuses. Look specifically for line items labeled “surrender charges,” “12b-1 fees,” “mortality and expense risk charges,” or “maintenance fees.” If your investment paperwork runs for hundreds of pages and requires a law degree to decipher the payout structure, you likely own a complex product designed to hide its true costs. Ask your advisor for a simple, single-page breakdown of every fee you pay annually in dollar amounts.

Can I get out of an expensive variable annuity without paying massive penalties?

Escaping a bad annuity requires careful timing and tax planning. Most variable annuities carry a surrender period lasting between five and ten years, during which you face steep penalties for early withdrawal. Review your contract to see if your surrender period has expired. If you still need an annuity structure but want lower fees, you can utilize Internal Revenue Service rules regarding section 1035 exchanges. This tax-free transfer allows you to move your funds directly from your high-fee variable annuity into a low-cost, direct-sold annuity offered by a discount brokerage, immediately stopping the bleeding from excessive fees.

Are all target-date mutual funds bad for my retirement?

Absolutely not. Target-date funds remain one of the best behavioral finance tools available to everyday investors, provided you choose the correct variety. The industry divides target-date funds into two distinct categories: actively managed and passively indexed. You must completely avoid the actively managed versions that charge high fees to try and beat the market. Instead, route your contributions into index-based target-date funds, which offer the exact same automated glide path into retirement but utilize ultra-low-cost index funds under the hood, maximizing your long-term wealth retention.

What is the safest way to invest for a retirement that is still decades away?

Safety over a multi-decade timeline requires protecting your purchasing power from inflation, which means you must accept short-term market volatility. The most prudent approach involves consistently buying a globally diversified portfolio of stock market index funds. While the stock market drops periodically, broad market indexes have historically recovered and driven immense wealth creation. Pairing these equity index funds with a growing allocation of bonds as you approach your target retirement date provides the perfect balance of growth to combat inflation and stability to weather inevitable economic storms.

Your Next Steps to Clean Up Your Portfolio

Transforming your retirement strategy begins with conducting a ruthless audit of your current holdings. First, log into your primary brokerage and workplace retirement accounts to locate the expense ratio for every single mutual fund or ETF you own. Highlight any fund charging more than point-five percent annually, as these represent prime candidates for replacement with cheaper index alternatives. Next, locate your life insurance and annuity contracts; request an in-force illustration from the carrier to explicitly identify the internal costs dragging down your returns. Finally, commit to adopting a fiduciary-only standard for any future financial advice you receive. By stripping away high-commission products and focusing on low-cost, highly liquid investments, you instantly reclaim control over your financial destiny and ensure your money works exclusively for your future, not your broker’s.