It is a typical Tuesday evening; you are cooking dinner while mentally calculating how to cover an unexpected root canal, the rising cost of after-school care, and your teenager’s upcoming orthodontic braces. The pot boils over on the stove as your mind races through bank balances and upcoming payment due dates. This mental tug-of-war drains your energy—leaving you feeling perpetually one step behind your own budget. Caring for a family requires immense emotional and physical bandwidth, and financial stress rapidly depletes your capacity to be present with your loved ones.

Building a comprehensive household money system requires much more than simply tracking pennies or restricting your spending. It demands a dedicated financial safety net that actively protects your housing stability, your immediate childcare needs, and your long-term ambitions from sudden economic shocks. When you lack a financial buffer, every minor inconvenience feels like a catastrophic event that threatens your household stability.

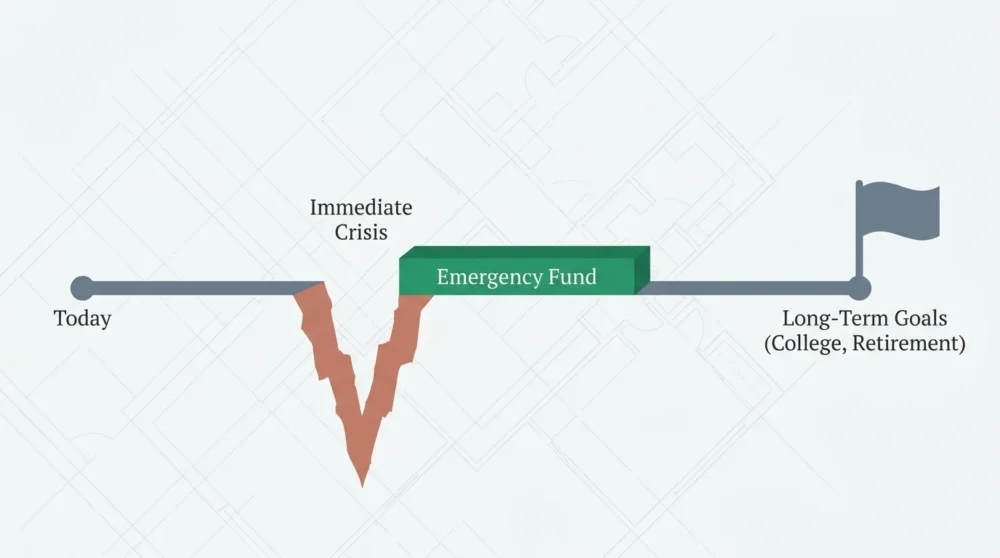

An emergency fund transforms these potential catastrophes into manageable inconveniences. By holding dedicated cash reserves in an accessible account, you reclaim control over your time, your choices, and your family’s future trajectory. A robust savings strategy acts as the cornerstone of generational wealth and daily peace of mind. Here are seven critical reasons you must prioritize building this essential cash buffer today.

Reason 1: An Emergency Fund Stabilizes Your Cash-Flow Framework

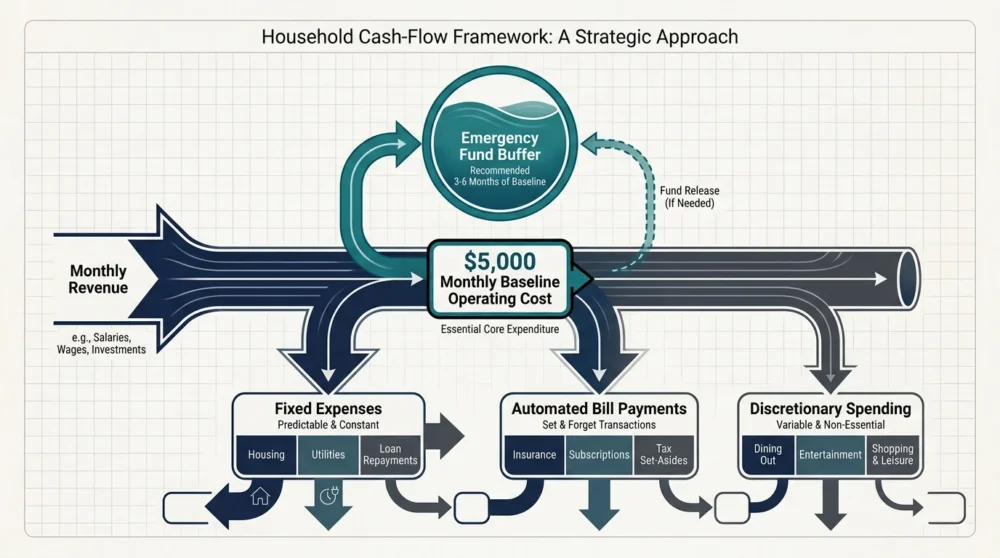

A functional household budget relies on a predictable cash-flow framework. You map your incoming revenue against your fixed expenses, automate your essential bill payments, and allocate the remainder toward groceries, fuel, and discretionary spending. This delicate ecosystem works beautifully when life goes exactly according to plan. However, a single unexpected mechanic bill can derail this entire system—forcing you to rely on high-interest credit cards just to buy groceries.

Cash reserves protect this daily operating structure. When you face a sudden disruption, you draw from your emergency account rather than pausing your automated bill payments or skipping a mortgage contribution. Real numbers illustrate this perfectly: if your monthly baseline operating cost is five thousand dollars, holding even one month of expenses in a liquid account guarantees your lights stay on during a sudden transition.

Furthermore, an emergency fund allows you to clearly separate unexpected crises from expected periodic expenses. You establish sinking funds for anticipated costs like annual property taxes or holiday gifts, while your emergency fund remains untouched unless a true crisis occurs. To help structure this foundational budget mapping, you can utilize the free financial worksheets provided by the Consumer Financial Protection Bureau to evaluate your baseline household expenses.

Reason 2: It Shields You From Unplanned Childcare and Housing Spikes

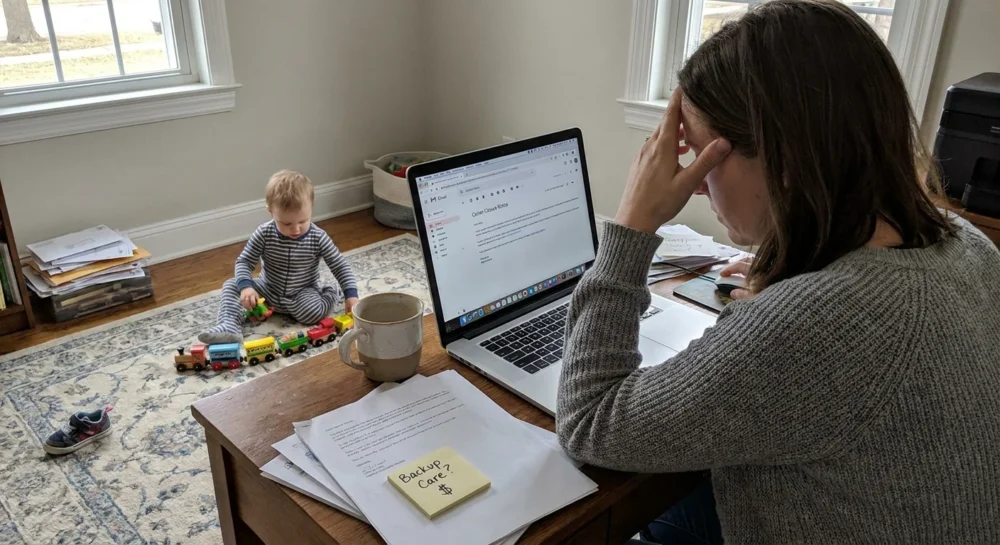

Caregivers intimately understand that childcare costs consume a massive percentage of the modern family budget. Historical benchmarks from the United States Department of Agriculture highlight the immense baseline cost of raising a child, yet inflation and modern daycare shortages push these figures even higher. You might budget meticulously for standard tuition, but unexpected gaps in care completely upend your monthly planning.

If your regular daycare center unexpectedly closes for a week, or your reliable nanny suddenly resigns, you must secure emergency backup care immediately. Backup care providers often charge premium daily rates that easily exceed your standard childcare allocations. An emergency fund allows you to write that premium check without hesitation—ensuring you can still attend work and maintain your primary income source.

Similarly, homeownership introduces severe, sudden financial liabilities. A failing HVAC system in the middle of a freezing winter or a burst pipe in your primary bathroom requires immediate remediation. Your cash reserves allow you to hire reputable contractors immediately, preventing minor water damage from evolving into a devastating structural crisis that displaces your family.

Reason 3: A Cash Buffer Fortifies Your Broader Safety Nets

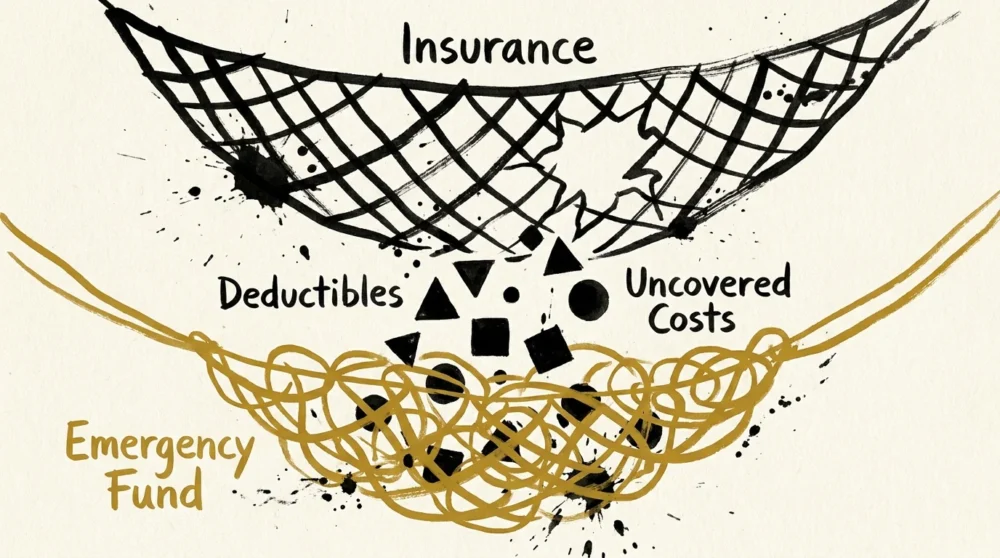

Insurance policies serve as essential protective barriers for your family, yet they contain a significant vulnerability: the deductible. You purchase health, auto, and homeowner policies to prevent financial ruin, but you cannot access these benefits until you pay your required out-of-pocket minimums. If you select an insurance policy with a higher deductible to keep your monthly premiums affordable, you must have that exact amount readily available in cash.

Emergency savings act as the anchor for these broader safety nets. Having three thousand dollars in the bank empowers you to file a necessary insurance claim immediately after a vehicle collision, rather than delaying critical repairs while you scrape the funds together. This proactive stance keeps your family moving forward and minimizes the disruption to your daily routines.

Additionally, protecting your family involves foundational estate planning, which requires upfront capital. Setting up basic wills, advance directives, and term life insurance policies protects your dependents, but hiring an attorney to draft these documents costs money. You can utilize your financial cushion to pay for these essential legal protections. If you struggle to navigate these overwhelming systems, you can consult vetted financial educators through the National Foundation for Credit Counseling for personalized, nonprofit guidance.

Reason 4: It Protects Your Long-Range Goals from Immediate Crises

Parents frequently sacrifice their own retirement security to handle immediate household crises. When a major appliance fails, you might feel tempted to withdraw funds from your retirement accounts or pause your long-term investing contributions. This reactive strategy severely damages your future financial independence; raiding a retirement account often triggers harsh tax penalties and disrupts the powerful engine of compound interest.

An emergency fund stands as a strict firewall between your current crisis and your future wealth. You preserve your retirement investments by paying for the broken refrigerator with cash from your emergency account. You continue making uninterrupted contributions to your long-term portfolios, ensuring your future self remains secure even when your present self faces adversity.

This firewall also protects your children’s educational investments. You work diligently to fund college savings accounts or 529 plans, aiming to reduce their future student loan burdens. A dedicated emergency fund ensures you never have to liquidate those educational assets prematurely. You can find robust resources on balancing immediate savings needs against college funding goals through tools provided by Federal Student Aid.

Reason 5: Emergency Savings Support Intergenerational Caregiving

Modern families increasingly find themselves in the sandwich generation—simultaneously supporting growing children and providing care for aging parents. The financial demands of eldercare often arrive without warning and carry immense emotional weight. You might receive a sudden phone call requiring you to fly across the country to assist a parent navigating a complex medical diagnosis.

Intergenerational support requires deep flexibility and rapid access to capital. You may need to pay for urgent medical transport, install accessibility ramps at a parent’s home, or cover the gap before their Medicare benefits activate. An emergency fund provides the liquidity necessary to solve these problems decisively, allowing you to focus on your parent’s health rather than panicking over the cost of a last-minute flight.

Furthermore, maintaining your own financial independence is the greatest gift you can offer your children. By building a robust emergency fund today, you ensure that you will not become a financial burden to your own kids in the future. You break the cycle of financial anxiety and establish a legacy of stability and proactive planning.

Reason 6: Financial Cushions Reduce Relational Friction

Financial stress remains one of the leading causes of relational tension and marital discord. When money is tight, you naturally adopt a scarcity mindset. Every minor spending decision becomes a high-stakes negotiation that can trigger exhausting arguments between partners. The pressure cooker of a rigid budget leaves no room for grace, spontaneity, or honest mistakes.

A healthy emergency fund dramatically lowers the emotional temperature in your home. It shifts your family money meetings from stressful triage sessions to strategic, forward-looking planning. Instead of arguing about how to cover an unexpected vet bill, you confidently authorize the payment and spend your meeting discussing your upcoming vacation goals or chore-based allowances for your children.

This stability allows you to implement functional communication systems and decision rules. For example, you and your partner can establish a threshold rule: any discretionary purchase over one hundred dollars requires a quick text message discussion, while smaller purchases do not require micromanagement. These systems only succeed when backed by the confidence of a well-funded cash reserve.

Reason 7: It Provides Breathing Room for Major Life Transitions

The modern economy demands incredible flexibility, yet true flexibility always requires capital. Whether you are navigating a sudden corporate layoff, managing the complex shift to a single-income household after the birth of a child, or deliberately taking a lower-paying job to improve your work-life balance, cash reserves buy you essential breathing room.

Transitioning through a period of unemployment without an emergency fund forces you to accept the very first job offer you receive, regardless of the salary or toxic work environment. Conversely, a fully funded safety net covering three to six months of living expenses empowers you to negotiate fiercely, wait for the right opportunity, and protect your career trajectory.

This breathing room also proves vital during a credit rebuild. If you are actively working to eliminate high-interest debt, an unexpected expense can easily derail your momentum and push you right back into the credit card trap. Holding a small starter emergency fund ensures that when a tire blows out, you pay with cash and keep your debt payoff journey entirely on track.

Frequently Asked Questions About Household Money Systems

How do blended families handle joint emergency savings?

Blended families often navigate complex financial histories, varied income levels, and existing child support obligations. You establish trust by maintaining transparent communication about your financial starting points. Many successful blended households utilize a hybrid approach: you build a joint emergency fund to cover shared household crises—like a leaking roof or a broken family vehicle—while maintaining smaller, individual emergency accounts to preserve a sense of personal autonomy and security. This structure fosters teamwork while respecting individual financial boundaries.

What is the best way for a single-income home to build a buffer?

Single-income households inherently carry a higher risk profile because the loss of one job eliminates one hundred percent of the family’s revenue. You must aggressively prioritize savings by automating small, weekly transfers to a high-yield savings account the moment your paycheck clears. You map your baseline budget ruthlessly, stripping away unused subscriptions and negotiating fixed bills. You leverage micro-saving strategies—sweeping leftover grocery cash or cash-back rewards directly into your emergency fund. Consistency matters far more than the initial dollar amount; even transferring twenty dollars a week builds critical momentum.

How can we rebuild credit while still trying to save?

Balancing credit repair with active saving requires a strategic, phased approach. You begin by halting all aggressive debt payments temporarily until you accumulate a starter emergency fund of one thousand to two thousand dollars. This initial cash barrier guarantees you stop relying on credit cards for minor emergencies. Once this starter fund is secure, you shift your focus to eliminating your highest-interest balances—often utilizing the avalanche or snowball debt payoff methods. You continue utilizing secured credit cards for planned, budgeted expenses, paying the balance entirely each month to steadily rebuild your credit score without risking new debt.

What steps help manage overwhelming childcare costs?

Managing the immense burden of childcare requires utilizing every available tax advantage and community resource. You must optimize your workplace benefits by actively enrolling in a Dependent Care Flexible Spending Account; this allows you to pay for qualifying daycare expenses using pre-tax dollars, significantly lowering your taxable income. You coordinate with your tax professional to claim applicable child and dependent care tax credits. Additionally, you explore community-based solutions, such as parent co-ops or shared nanny arrangements, which disperse the financial load across multiple families while maintaining high-quality care standards.

Schedule Your Family Money Check-In

Reading about financial strategy only matters if you translate these concepts into tangible action. You hold the power to permanently alter your family’s financial trajectory by initiating clear, honest conversations about your household money systems. Do not wait for the next crisis to force the issue; proactive planning builds resilience and deepens trust among family members.

Take ten minutes this week to schedule a dedicated family money check-in. You can review your current cash reserves, identify upcoming seasonal expenses, and set up an automated transfer to your emergency savings account. Even a modest contribution marks a decisive step toward lasting stability. By prioritizing your financial safety net today, you guarantee a more secure, peaceful, and empowered tomorrow for your entire household.