Picture your family gathered around the dinner table, sharing stories and passing dishes. Suddenly, a casual remark about a neighbor’s sudden illness or a friend’s messy estate battle sparks a heavy, uncomfortable silence. You catch your adult children exchanging worried glances, silently wondering how they would handle a similar crisis if it happened to you. This unspoken tension around aging, caregiving, and inheritance is a heavy burden for both generations to carry. You can dissolve that anxiety by pulling back the curtain on your financial reality long before an emergency strikes. Opening up about your money does more than just transfer logistical knowledge; it builds a bridge of profound trust and equips your children to manage future transitions without the panic of the unknown. Delaying these conversations often leaves families scrambling during medical crises, forcing them to navigate deep emotional grief and exhausting financial detective work simultaneously. Taking charge of this narrative empowers your adult children and fiercely protects the legacy you spent decades building. It allows you to define the terms of your future care and ensures your assets are handled exactly as you intend.

Mapping Your Cash Flow and Sharing the Blueprint

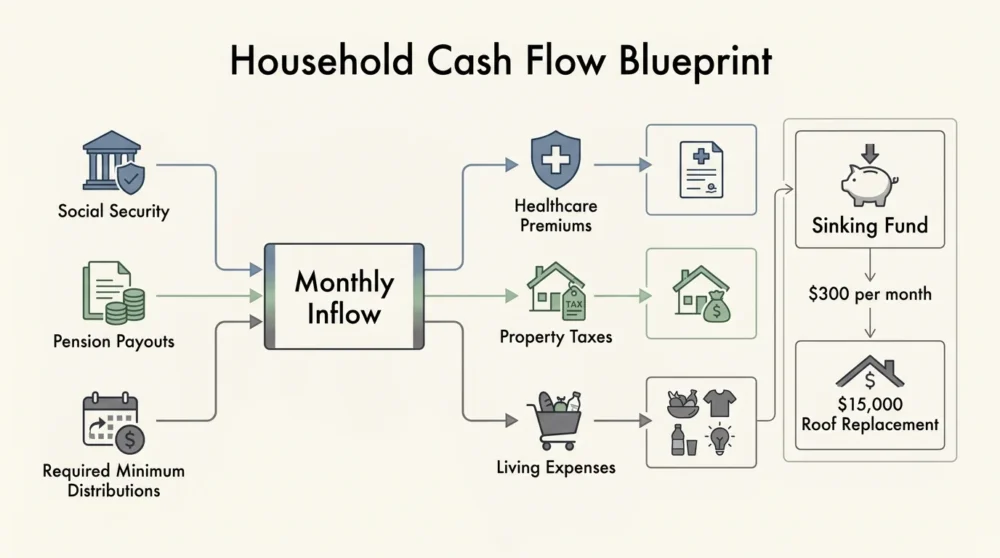

To start this vital dialogue, you need to show your adult children how your household money systems operate on a daily and monthly basis. They might assume you have infinite resources stashed away, or conversely, they might worry you are quietly struggling to pay for groceries on a fixed income. By mapping your cash flow together, you replace their assumptions with concrete, manageable data. Sit down and explain the mechanics of your budget, detailing your fixed income sources like Social Security benefits, pension payouts, or required minimum distributions from your retirement accounts. Show them exactly how those funds cover your basic living expenses, healthcare premiums, and property taxes. You do not need to share every grocery receipt, but providing a high-level overview of your monthly inflows and outflows establishes a crucial baseline of reality. This transparency helps them understand your daily financial rhythms and sets realistic expectations about your spending capacity.

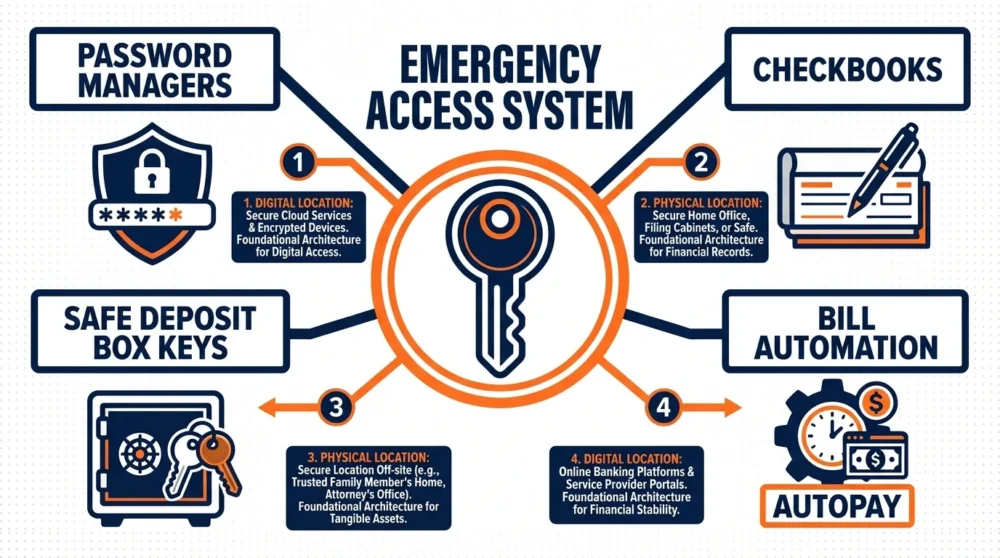

Explain the concept of sinking funds if you use them to manage large, infrequent expenses. For example, if you deliberately set aside three hundred dollars every month into a dedicated savings account for a future fifteen-thousand-dollar roof replacement or an upcoming vehicle purchase, tell them. Sharing this strategy teaches them advanced budgeting techniques for their own households while reassuring them that you are actively anticipating future liabilities. It is also critical to walk them through your bill automation systems. If a sudden illness incapacitates you, your adult children need to know exactly which bills are set to autopay and which bank accounts fund those automated payments. Share the physical or digital location of your password managers, checkbooks, and safe deposit box keys. When your children understand the foundational architecture of your daily finances, they can step in seamlessly if a medical emergency temporarily takes you out of the driver’s seat—preventing late fees, utility shut-offs, and unnecessary stress.

Building and Explaining Your Safety Nets

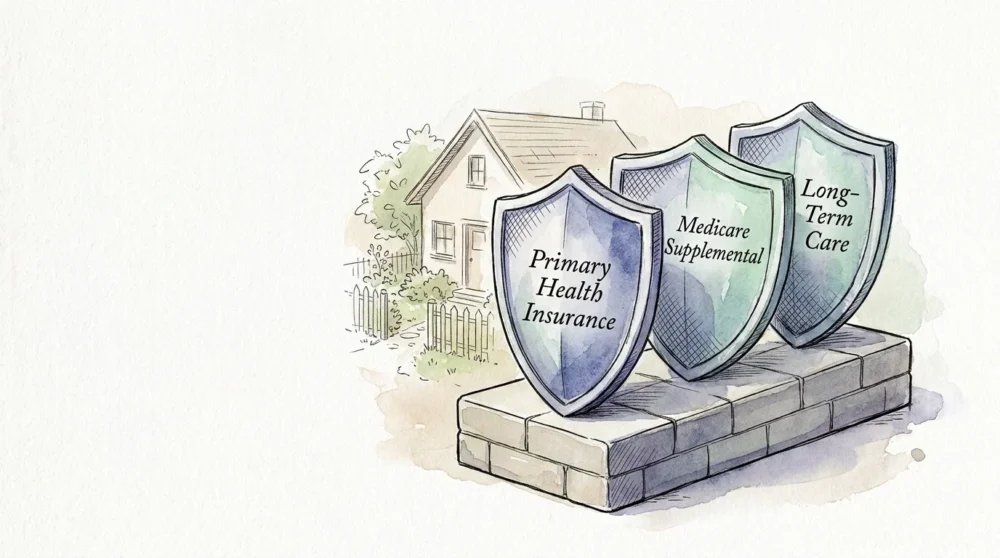

Once the daily cash flow is clear, pivot the conversation to the structural integrity of your safety nets. This is often the most reassuring part of the discussion for your adult children, as it directly addresses their quietest fears about your vulnerability. Start by reviewing your comprehensive insurance coverage. Detail your primary health insurance, Medicare supplemental plans, and any long-term care policies you currently hold. Explain exactly what these policies cover, such as in-home nursing care or assisted living facilities, and what they do not cover. This level of transparency prevents your family from being blindsided by staggering out-of-pocket medical bills later. Next, discuss your liquid emergency fund. Reveal the amount you keep in accessible savings accounts specifically earmarked for unexpected medical deductibles, sudden home repairs, or temporary income disruptions. When they know you have a fully funded six-month cash reserve, their underlying anxiety about needing to financially support you diminishes significantly.

The absolute cornerstone of your safety net is your estate plan, and this topic requires blunt, honest communication. Outline the foundational legal documents you have established, including your last will and testament, your durable financial power of attorney, and your healthcare proxy or advance directive. Do not just tell them these documents exist in a filing cabinet; explain your reasoning behind the specific people you chose for these critical roles. If you named your oldest daughter as your healthcare proxy because she has a background in nursing and remains calm under pressure, state that clearly to prevent quiet resentment among her siblings. You can direct them to excellent educational resources provided by the Consumer Financial Protection Bureau to help them fully understand the legal and ethical responsibilities associated with managing someone else’s money. Furthermore, discuss how you are optimizing your government and retirement benefits. If you intentionally delayed drawing Social Security until age seventy to maximize your guaranteed monthly payout, explain the math behind that strategic trade-off. Your adult children will learn invaluable lessons from your long-term planning while gaining immense confidence in your financial security.

Aligning Long-Range Goals and Intergenerational Support

Family finances rarely exist in a sterile vacuum, and your money choices frequently intersect with the major life milestones of your adult children. You might currently be navigating the delicate, emotionally charged balance of preserving your retirement nest egg while desperately wanting to help them fund housing down payments, exorbitant childcare, or their own children’s education. You must be explicitly clear about your financial boundaries and actual capabilities. If you intend to contribute to your grandchildren’s future, discuss the exact mechanics of how you plan to do so. Setting up a 529 college savings plan is a brilliant, tax-advantaged way to offer intergenerational support without simply handing over uncontrolled cash. You can explain how the invested funds grow tax-free over the years and clarify exactly how much you plan to contribute annually, setting firm expectations.

However, you must also communicate your necessary retirement trade-offs with firm compassion. You might have to gently but resolutely explain that you cannot co-sign a massive mortgage or provide a substantial down payment loan because doing so would severely jeopardize your own financial independence. Framing this refusal as a protective measure for their own future is highly effective. You are ensuring that you will never become a financial burden to them in your later decades, which is truly the greatest financial gift you can ever offer a child. If you are actively stepping in to help with your grandchildren, quantify that contribution. According to ongoing economic data tracked by the United States Department of Agriculture, the baseline cost of raising a child is astronomically high, and your unpaid labor as a part-time caregiver provides immense financial relief to your adult children’s household budget. Discuss this dynamic openly so both parties fully understand the economic value of your time and the strict boundaries required to prevent you from experiencing caregiving burnout.

Establishing Family Communication and Money Systems

Talking about money should never be a one-time, high-stress event initiated only by a crisis; it needs to become a routine, normalized part of your family culture. To achieve this healthy dynamic, you should establish a structured family communication system. Propose a recurring annual family money meeting. Set a clear, written agenda for this gathering, starting with general updates on your health and future housing plans, moving to any structural changes in your estate documents or account locations, and finishing with an open, non-judgmental floor for their questions. Hosting this meeting in a neutral, comfortable environment—perhaps a quiet weekend afternoon with coffee and pastries—strikes the perfect balance between handling serious business and fostering family bonding.

You can also use these conversations to help your adult children build better financial systems within their own growing households. Share the hard-won generational wisdom you have accumulated over decades of earning and saving. For instance, talk to them about how you successfully taught them the value of a dollar, and how they might actively implement chore-based allowances for their own kids. Explaining how linking specific household tasks to earning money fosters a strong, resilient work ethic in the youngest generation reinforces your respected role as the family’s financial educator. Establish strict, unwavering decision rules for any ongoing financial assistance you currently provide to your adult children. If you are helping a child aggressively pay off lingering student loans, agree on a formalized matching system where you contribute one dollar for every dollar they independently pay above the required minimum. These formalized systems remove the emotional friction and guilt from family money, turning potential conflicts into collaborative, highly structured teamwork.

Frequently Asked Questions About Family Finance Dynamics

How do we navigate transparency in a blended family?

Blended families inherently introduce highly complex layers of financial history, competing inheritance expectations, and deep emotional attachments. When dealing with stepchildren, multiple marriages, and varying state laws, absolute clarity is your best defense against future litigation and family heartache. You must be completely transparent about which specific assets are legally shared with your current spouse and which are strictly ring-fenced for your biological children. Explain your exact beneficiary designations on all retirement accounts and life insurance policies in detail. If you have established a specific legal trust to ensure your current spouse can remain comfortably in the family home while the eventual equity passes directly to your children, outline this mechanism clearly to all parties. Open, mediated communication now prevents devastating surprises during the stressful probate process and preserves fragile family harmony when you are no longer there to keep the peace.

What if my adult children rely on a single-income household?

Single-income households face significantly heightened vulnerabilities, especially during sudden economic downturns or unexpected health crises. If your adult child operates a single-income home, your financial conversations should heavily emphasize the critical importance of robust term life and long-term disability insurance for the primary earner. You can share your own historical experiences with managing income protection and risk. Furthermore, discuss how your estate plan might conditionally provide a safety net for their family if the primary earner tragically loses their job or passes away. While you should never promise to be an endless ATM, you can gently reassure them that your emergency reserves could offer temporary stabilization in a worst-case scenario. You might also point them to demographic realities and income studies highlighted by the United States Census Bureau to show them they are definitely not alone in managing the tight margins of a single-earner household, encouraging them to aggressively prioritize their own emergency savings rate.

How can I help an adult child who needs a credit rebuild?

It is profoundly painful to watch an adult child struggle with suffocating consumer debt or a poor credit history, but bailing them out with a sudden lump sum often enables the exact behavior that caused the systemic problem. Instead of simply writing a check, generously offer to fund comprehensive educational sessions with a certified financial counselor from a reputable organization like the National Foundation for Credit Counseling. If you do ultimately choose to provide direct financial assistance, strictly structure it as a formal loan with a written promissory note, a clear repayment schedule, and an agreed-upon, fair interest rate. You can also offer to add them as an authorized user on your oldest, spotless credit card account to help artificially boost their credit score, provided you keep the physical card securely in your own possession to prevent any further debt accumulation. This structured approach offers practical, highly effective scaffolding without ever compromising your own hard-earned financial stability.

Should we factor their childcare costs into our estate planning?

Childcare is very often the most crushing, relentless expense a young family faces, frequently rivaling or even significantly exceeding their monthly mortgage payments. While your estate plan is primarily designed for post-life asset distribution, you can absolutely utilize a portion of your wealth right now to significantly ease their current, heavy burden. Living inheritances are becoming increasingly popular for this exact reason. If your own retirement is fully funded and completely secure, you might choose to pay their preferred daycare center directly or help fund a dependent care flexible spending account. This brilliant strategy allows you to joyfully witness the profound impact of your wealth during your lifetime. Alternatively, if you cannot or prefer not to provide liquid cash, generously offering to provide dedicated childcare one or two days a week is a massive, tangible economic contribution that should be explicitly recognized and highly valued within your family’s overall long-term financial planning.

Do not let the quiet fear of awkwardness delay these utterly critical conversations. The absolute worst time to figure out a family’s complicated financial puzzle is in the sterile, terrifying waiting room of a hospital or the stiff, grief-filled chairs of a funeral home; you have the power to replace uncertainty with clarity right now. Pick up the phone this week and invite your adult children over for a relaxed, open conversation about the future. By courageously sharing your cash flow, meticulously explaining your safety nets, and aligning your long-term goals, you are actively giving them a priceless inheritance of profound preparedness and lasting peace of mind. Start talking today, and firmly secure your family’s financial resilience for generations to come.