Picture sitting at your kitchen table on a Sunday evening. On your left sits your aging mother’s annual benefit statement; on your right sits your toddler’s monthly daycare invoice. You stare at the numbers, and the tension in your shoulders tightens. Your parent relies entirely on fixed government benefits, while you juggle modern parenting costs and your own distant retirement dreams. You wonder how families manage this intergenerational financial squeeze without breaking apart. You are not alone; millions of caregivers currently navigate the complex reality of household budgeting for multiple generations under a single roof.

The short answer to whether an individual can live comfortably on Social Security alone delivers a stark reality check. Federal census data indicates the average monthly retirement benefit hovers around $1,900. For most seniors, that modest amount barely covers housing, property taxes, and basic utilities. Furthermore, standard Medicare premiums are deducted directly from that check before it ever reaches a bank account, shrinking actual cash flow. The widening gap between fixed incomes and living expenses forces families into the sandwich generation. Living comfortably requires far more than hoping a single government check stretches to the end of the month; it requires a unified family financial strategy.

Implementing a Cash-Flow Framework for the Whole Family

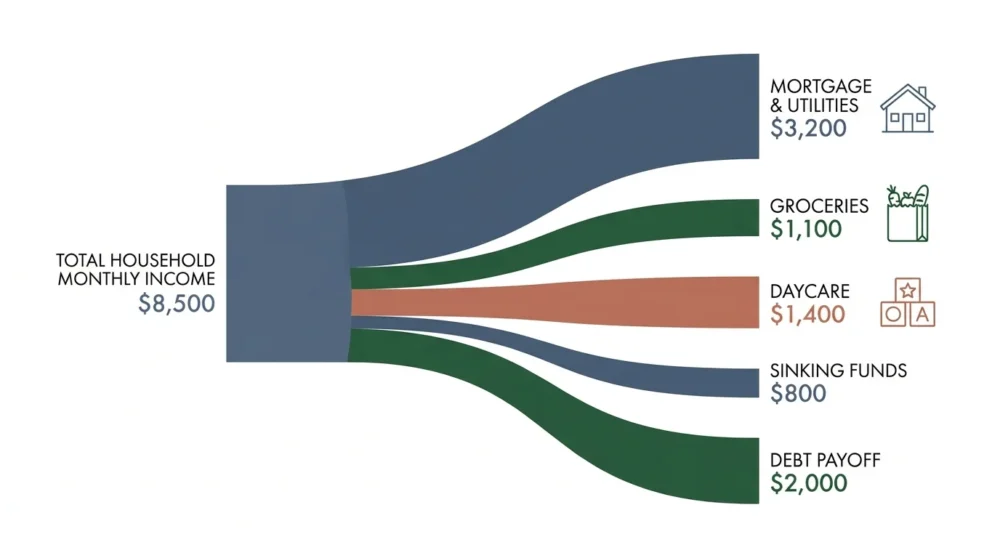

Addressing these multi-generational challenges requires you to build a robust household money system. You need a cash-flow framework based on hard numbers, not vague assumptions. Start by mapping your entire household budget to understand exactly where every dollar goes. When you merge an aging parent’s fixed income with your own household earnings, you create a clearer picture of your collective purchasing power. If your combined household brings in $8,500 monthly, you must track exactly how much vanishes into structural overhead like mortgages, groceries, and utilities before allocating funds to debt payoff or savings goals.

Next, implement sinking funds to handle irregular but inevitable expenses. A sinking fund allows you to set aside small amounts each month for predictable future bills. If you know your parent’s annual out-of-pocket medical deductibles average $1,200, automate a transfer of $100 every month into a dedicated savings account. Apply the exact same strategy to your own life by setting aside $150 monthly for inevitable car repairs. This proactive division ensures that when the brake pads wear out or the pharmacy bill spikes, the cash is already waiting in the bank.

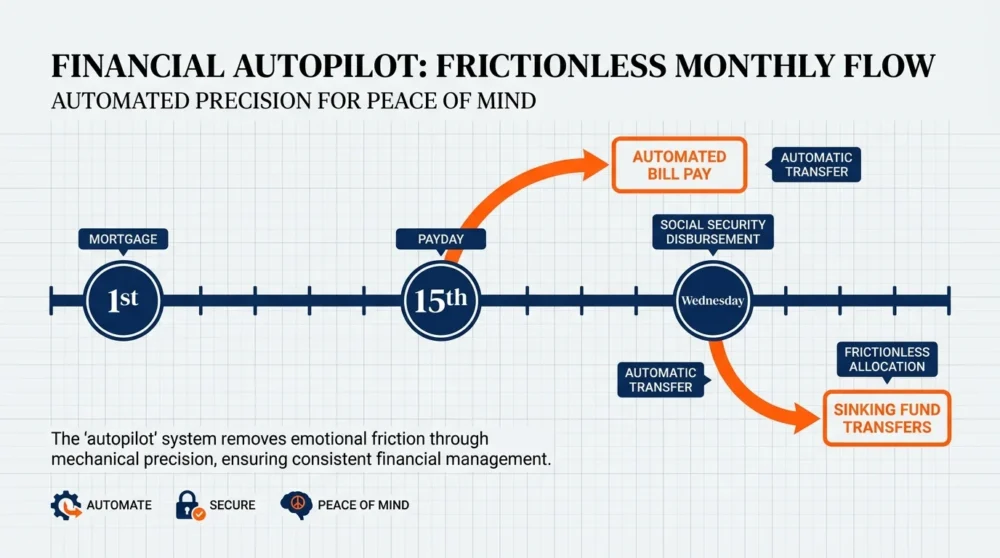

Automating your bills removes the emotional friction from daily money management. Set up direct debits for fixed expenses like mortgages, utilities, and insurance premiums. Schedule these automatic transfers to align perfectly with payday and Social Security disbursement dates, which typically fall on specific Wednesdays of the month. You free up immense mental bandwidth to focus on complex family decisions when you put routine payments on autopilot.

Building Safety Nets for Every Generation

Building safety nets requires a proactive approach to risk management. You must optimize benefits and secure the right insurance policies to prevent a single medical emergency from derailing your family’s stability. For aging parents, Medicare optimization represents a crucial annual task. Sit down with them every fall during open enrollment to review their coverage. You must ensure their current prescription drug plan covers their specific medications cost-effectively for the upcoming year.

For your immediate family, term life insurance and long-term disability coverage form the bedrock of your protection strategy. If you provide the primary income supporting growing children and dependent parents, your sudden loss of income would devastate the household. Secure a robust term policy that covers your remaining mortgage balance, projected childcare costs, and your parent’s ongoing care needs. Skip the expensive permanent life insurance products and buy pure term coverage to secure the maximum death benefit for the lowest premium.

Emergency funds remain your critical first line of defense against the unexpected. Keep three to six months of essential collective living expenses in a completely liquid, high-yield savings account. You might feel tempted to invest this money to chase higher returns, but liquidity is paramount when the roof springs a leak or a parent requires sudden medical transport. Estate planning basics also fall squarely under the safety net umbrella. Every adult in your household needs a finalized living will, an advance healthcare directive, and a durable power of attorney. You can find practical guides on structuring these legal documents through the Consumer Financial Protection Bureau.

Balancing Long-Range Goals and Intergenerational Support

Balancing long-range goals with immediate family support requires strict prioritization. You face a constant tug-of-war between saving for your children’s future college education, funding your own retirement, and supplementing your parent’s fixed income. Prioritize your own retirement savings above all else. You can borrow money for college tuition, but no lending institution will offer you a personal loan to fund your retirement years.

If you neglect your own nest egg to pay for everything else today, you simply pass the heavy burden of your care onto your children in the future. Contribute enough to your employer’s workplace plan to capture the full matching contribution before directing funds elsewhere. Take time to use the Social Security Administration calculators to forecast your own future payouts, ensuring you understand the gap you need to fill with personal investments.

Intergenerational support does not always mean writing a massive check every month. Offset household costs through strategic, non-financial family contributions. An aging parent might not contribute significantly to the monthly mortgage payment, but they can provide reliable after-school childcare, saving you thousands of dollars annually. When you quantify these non-financial contributions, you alleviate interpersonal tension. Federal surveys and USDA food plan reports reveal that groceries consume a massive portion of a family budget. A parent who takes over weekly meal planning and bulk cooking dramatically reduces your monthly food expenses.

Establishing Family Communication and Money Systems

No financial strategy survives the chaos of daily life without open communication and clearly defined systems. Hold regular family money meetings to keep everyone aligned and accountable. Schedule a dedicated hour once a month to review the household budget, track progress toward sinking funds, and discuss any upcoming major expenses. Create a simple, recurring agenda covering cash flow status, safety net reviews, and long-range planning. Treat this kitchen-table meeting with the exact same respect you give a professional workplace obligation.

Include your children in these money conversations using age-appropriate concepts. Introduce chore-based allowances to teach them the vital connection between effort and income. Instead of handing out a flat weekly sum unconditionally, tie their compensation to specific household responsibilities like folding laundry or loading the dishwasher. This hands-on approach builds concrete financial literacy early, ensuring your kids develop the robust skills needed to fund their own lives so they never find themselves completely dependent on fixed government benefits.

Establish clear decision rules for discretionary spending across the household. Institute a rule that any non-essential purchase over $100 requires a mandatory 24-hour cooling-off period and a brief discussion between partners. When you integrate aging parents into these household financial discussions, you respect their autonomy and dignity while maintaining necessary boundaries around the unified family budget.

Frequently Asked Questions About Household Finances

How can blended families navigate conflicting money philosophies?

Blended families often bring competing financial habits, different spending triggers, and separate legal obligations into a new household. Prioritize absolute financial transparency from day one. Sit down with your partner and lay out every asset, debt, and fixed expense on the table. Create a joint checking account specifically for shared household bills, while maintaining individual accounts for personal discretionary spending. This hybrid approach fosters deep teamwork while preserving individual autonomy, significantly reducing daily friction over minor purchases.

What are the most effective budgeting strategies for single-income households?

Single-income homes require a dedication to zero-based budgeting, a system where every single dollar receives a specific job title before the month even begins. Build a significantly larger emergency fund—ideally holding six to nine months of living expenses—because you lack a secondary household income to fall back on if an unexpected job loss occurs. Focus heavily on cutting structural overhead. Call your providers to negotiate your insurance rates, eliminate unused monthly subscriptions, and meticulously plan family meals around weekly grocery sales to maximize your single stream of revenue.

How do you rebuild a damaged credit score while juggling massive family expenses?

Rebuilding credit requires slow, steady consistency rather than overnight cash infusions. Start by pulling your annual credit reports and formally disputing any outdated inaccuracies dragging down your score. Keep your credit utilization ratio below thirty percent by paying down active balances strategically. Automate minimum payments on all open accounts to ensure you never miss a due date, as payment history makes up the largest portion of your score. If outstanding consumer debt feels completely overwhelming, consult a vetted nonprofit credit counseling agency to explore a formal debt management plan, which can consolidate your payments and lower interest rates without forcing you to take out a new loan.

How can families effectively offset the crushing cost of modern childcare?

Childcare costs routinely rival a monthly mortgage payment, forcing families to seek creative alternatives to traditional daycare centers. First, thoroughly investigate whether your employer offers a Dependent Care Flexible Spending Account. This powerful tool allows you to pay for qualifying daycare expenses with pre-tax dollars, saving you up to thirty percent on your actual out-of-pocket costs. Next, actively explore cooperative childcare arrangements with trusted neighbors or other parents in your local community, trading supervision days to lower costs. Finally, heavily leverage the time and energy of aging parents who live with you or nearby. Securing even two days a week of reliable grandparent care dramatically reduces your annualized daycare expenses, keeping thousands of dollars inside the family ecosystem.

Take Control of Your Family’s Financial Future

Navigating the complex intersection of aging parents on fixed incomes, rapidly growing children, and your own pursuit of financial independence requires immense patience and discipline. The daily math might seem completely intimidating when you first look at a static Social Security income alongside rising household costs. However, when you actively implement solid cash-flow systems, automate your savings, and communicate openly with every generation under your roof, you strip away the anxiety and replace it with practical, actionable steps.

Do not let another stressful month slip by in a haze of financial uncertainty. Schedule a comprehensive family money check-in this week. Gather your budget documents, sit down with your partner or parents, and map out your financial trajectory for the next thirty days. You possess the power to rewrite your family’s money habits, build lasting safety nets, and confidently ensure that every single generation under your roof thrives together.