Picture yourself sitting at the kitchen table late on a Sunday evening, staring down a stack of incoming mail. On the left sits a hefty medical bill for a recent hospital stay; on the right, a permission slip for your child’s expensive field trip and a rising property tax statement. You might already be squeezing your budget to cover standard housing costs, fund your toddler’s daycare, and perhaps even send a small monthly stipend to your aging parents. Suddenly facing a chronic illness or severe injury diagnosis for your spouse shatters your financial equilibrium. The tension between preserving a normal family life and funding an essential senior care budget creates an overwhelming emotional and financial burden. You love your partner and want to provide the highest quality care, but you also have a household to run, children to raise, and an eventual retirement to fund.

Navigating long term care spouse finances requires moving past panic and building an ironclad household money system. You must transform your abstract worries into a concrete plan. When you take proactive control of your cash flow, legal protections, and family communication, you reclaim your peace of mind. By implementing strategic money systems, you can protect your spouse’s dignity, keep your household running smoothly, and secure your family’s financial future.

Building a Resilient Cash-Flow Framework

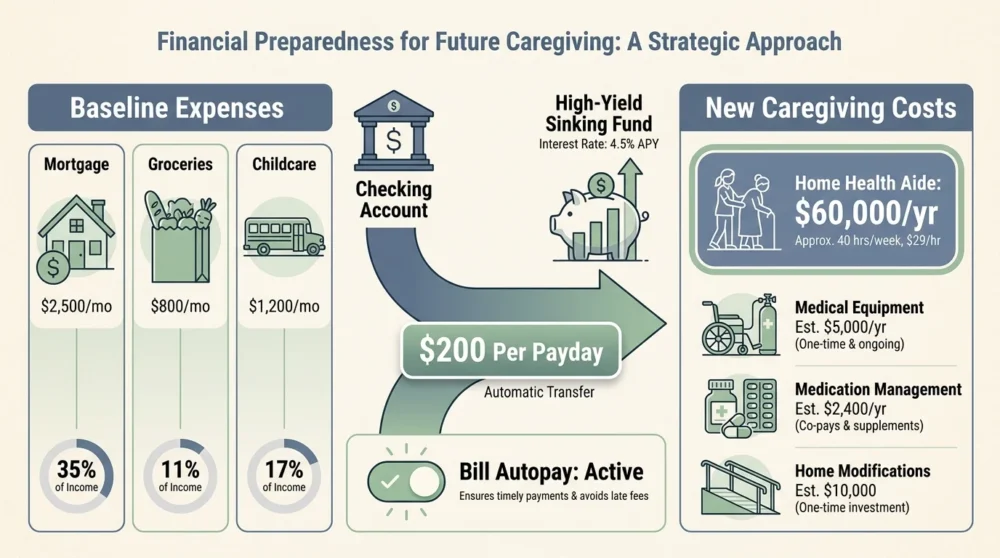

Your first step in a spouse illness financial plan involves ruthless and precise budget mapping. When long-term care enters the picture, vague mental math no longer suffices. You need to account for every dollar entering and exiting your household. Start by separating your baseline living expenses—such as your mortgage, utilities, groceries, and childcare—from your new caregiving costs. Concrete data makes a massive difference here. The USDA cost studies historically estimate that raising a child costs over a quarter of a million dollars from birth to age eighteen. When you combine those heavy child-rearing expenses with a home health aide that can cost upwards of sixty thousand dollars a year, your monthly cash flow faces unprecedented strain. You must reallocate funds from discretionary categories like dining out or luxury travel into your essential care and housing buckets.

Once you map your budget, you should implement targeted sinking funds to absorb financial shocks. A sinking fund is a dedicated savings account designed for a specific future expense. Open a high-yield savings account exclusively for your medical deductibles and out-of-pocket care costs. Set up an automatic transfer to move a set amount—say, two hundred dollars—from your primary checking account into this sinking fund every payday. When a massive pharmacy bill or a copay for a specialist visits arrives, you pull the money directly from the sinking fund rather than scrambling to cover it from your grocery budget. You can use the same sinking fund strategy to save for upcoming home modifications, such as installing a wheelchair ramp or retrofitting a ground-floor bathroom.

Bill automation serves as another critical tool for the healthy spouse. Caregiving consumes an enormous amount of mental energy and time. You cannot afford to pay late fees simply because you spent hours on the phone with insurance companies and forgot to pay the electric bill. Set all your fixed household expenses and recurring medical premiums to autopay. This system ensures your lights stay on and your insurance policies remain active without requiring your constant manual intervention.

Establishing Unbreakable Safety Nets

A well-structured budget falls apart without the right protective barriers in place. Traditional financial advice suggests keeping three to six months of living expenses in an emergency fund. However, when managing a spouse’s long-term care, you should aggressively aim to expand that safety net to nine or twelve months of expenses. Illness brings unpredictable complications; a sudden hospitalization could force the healthy spouse to take unpaid leave from work. A robust emergency fund provides the ultimate breathing room during a crisis.

Beyond cash savings, you must solidify your legal and insurance safety nets. Estate planning basics are non-negotiable. Both you and your spouse need updated wills, durable powers of attorney, and advance healthcare directives. A durable power of attorney allows you to make financial decisions, access bank accounts, and manage investments if your spouse loses cognitive or physical capacity. Without this document, you might have to endure a lengthy and expensive legal battle to gain conservatorship over your own household assets. You can utilize resources from the Consumer Financial Protection Bureau tools to understand your specific responsibilities and rights as a financial caregiver.

You also need to optimize every available benefit. Review your employer-sponsored benefits for hidden gems like backup care assistance, flexible spending accounts for dependent care, or critical illness insurance payouts. Understand the stark difference between Medicare and Medicaid. While many families assume Medicare will cover a nursing facility indefinitely, Medicare’s official guidelines clarify that it only pays for short-term rehabilitation following a hospital stay. Medicaid, on the other hand, covers long-term facility care but requires you to meet strict, state-specific income and asset depletion thresholds. Navigating Medicaid spend-down rules while protecting the healthy spouse’s living standards—often called the Community Spouse Resource Allowance—usually requires guidance from a certified elder law attorney.

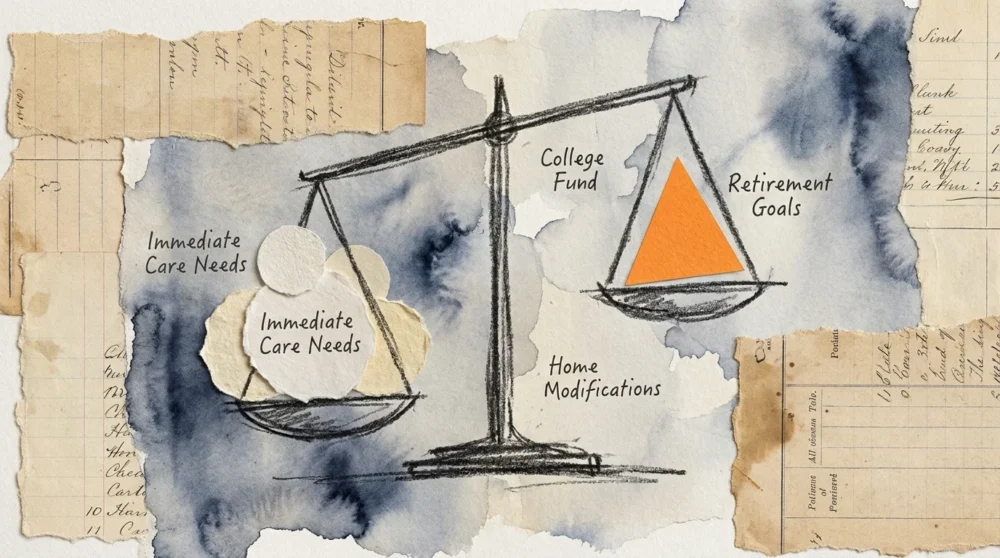

Balancing Long-Range Goals with Immediate Needs

Caregivers frequently sacrifice their own future security to fund immediate medical needs. You might feel tempted to pause your retirement contributions or drain a 529 college savings plan to pay for your spouse’s care. You must resist this urge. Census Bureau data highlights the severe financial pressure placed on caregivers, showing that millions of Americans risk poverty in their later years because they completely halted their wealth-building efforts to support a sick relative. You cannot borrow money to fund your retirement, but your children can access scholarships, grants, and federal student loans to fund their education.

Adopt a firm rule of thumb: secure your own retirement and your emergency housing needs before overfunding a child’s college account or bailing out adult children financially. This intergenerational support boundary is incredibly difficult to enforce emotionally, but it remains financially imperative. If you bankrupt your retirement to pay for your spouse’s immediate care, you will simply become a financial burden to your children in twenty years. Prioritize maximizing any employer matches in your 401(k) or 403(b) accounts. If cash flow becomes overwhelmingly tight, reduce your contributions to the minimum required to get the match, but do not stop investing entirely. Time in the market remains your strongest asset for long-term survival.

Creating Household Communication and Money Systems

Financial plans fail in a vacuum; they require active, ongoing communication across your entire household. Establishing a weekly family meeting creates a structured environment to discuss the week ahead. Keep the agenda brief and practical. Start by sharing one positive family win to maintain morale. Next, review upcoming medical appointments so everyone understands the logistical schedule. Discuss the week’s grocery and household budget, ensuring all family members understand any current spending freezes. Finally, distribute household chores.

Involving children in household management provides massive relief to the caregiving spouse while teaching valuable financial literacy. Implement a chore-based allowance system for age-appropriate tasks. If your teenager takes over mowing the lawn, doing the family laundry, or cooking dinner twice a week, pay them a weekly stipend for their labor. This arrangement serves two purposes. First, it frees up your limited time so you can manage insurance claims, work your day job, and provide direct care to your partner. Second, it shifts discretionary spending away from you; when your teenager wants to buy a new video game or go to the movies, they use their earned allowance. This creates clear decision rules within the family and stops the constant nickel-and-diming that slowly drains a household budget.

Frequently Asked Questions from Caregiving Families

How should blended families approach long-term care funding?

Blended families face complex dynamics when balancing the financial needs of stepchildren alongside a spouse’s long-term care. Transparency and clear boundaries serve as your best tools. You should keep pre-existing separate assets distinctly categorized, particularly if you established specific trusts or college funds for children from a previous marriage. Have an open conversation with adult stepchildren about the reality of their parent’s caregiving cost. Set clear expectations regarding who holds the power of attorney and how the family will fund facility care or home aides. Consulting an estate planner who specializes in blended family dynamics ensures that the healthy spouse retains their home and livelihood while honoring the sick partner’s wishes for their biological children.

How do we survive a transition to a single-income home?

When a spouse’s illness forces them to leave the workforce, the sudden loss of income requires an immediate and radical lifestyle adjustment. Do not wait for the severance pay or short-term disability to run out before making changes. Downsize your expenses proactively. You might need to trade in a financed vehicle for a reliable used car to eliminate a monthly payment. Cancel all non-essential subscriptions. Investigate whether the ill spouse qualifies for Social Security Disability Insurance, which can replace a portion of their lost income. Depending on your state and the exact nature of the care required, the healthy spouse or an adult child might even qualify to receive payment as a family caregiver through Medicaid waiver programs.

What is the best way to rebuild credit after medical debt?

A staggering medical diagnosis often brings equally staggering debt, which can quickly ruin a carefully built credit score. If you missed credit card or mortgage payments while dealing with an acute medical crisis, start your recovery by prioritizing your secured debts—your home and your car. Communicate directly with hospital billing departments; non-profit hospitals are legally required to offer financial assistance programs that can forgive a massive portion of your medical debt based on your current income. Do not convert interest-free medical debt into high-interest credit card debt. If you feel completely underwater, seek guidance from a vetted, non-profit credit counseling agency like the National Foundation for Credit Counseling to help you consolidate payments and rebuild your credit responsibly over time.

How do we manage skyrocketing childcare costs alongside caregiving expenses?

The dual pressure of paying for daycare and funding a senior care budget represents the ultimate sandwich generation squeeze. You must aggressively hunt for structural relief. Check if your employer offers a Dependent Care Flexible Spending Account, which allows you to use pre-tax dollars for childcare, saving you thousands of dollars a year in taxes. Look into community-based programs; many local YMCAs, faith-based organizations, and public school districts offer sliding-scale after-school care based on your household income. If you have reliable family members nearby, consider asking them to cover one or two days of childcare a week in exchange for you covering a different need for them down the road. Every dollar you shave off childcare is a dollar you can redirect toward your spouse’s physical care and comfort.

Managing the financial fallout of a spouse’s long-term care demands incredible resilience, but you possess the strength to build a functioning system. You do not have to tackle the entire decades-long financial plan today. Pick just one actionable step to execute right now. Schedule a thirty-minute family money check-in for this coming Sunday. Open that high-yield savings account and set up your first automatic transfer for medical deductibles. Secure your power of attorney documents. By taking small, deliberate actions, you will slowly replace your financial anxiety with operational confidence, ensuring your family thrives even in the face of profound adversity.