Picture your family gathered around the dinner table on a bustling Sunday afternoon. You watch your grandchildren playing in the living room and feel a deep, instinctual urge to give them a significant financial head start in life. Yet, as you survey the room, you also see your adult children quietly stressing over exorbitant childcare bills, and you know your own aging parents require increasing levels of medical support. This delicate balancing act defines the modern sandwich generation; you are caught between securing your own retirement, supporting your immediate family today, and funding a legacy for tomorrow. You want to leave money to your grandchildren, but you cannot afford to jeopardize your current financial stability to do so.

Building a household money system resolves this tension by transforming vague wishes into mathematical realities. The desire to provide a financial gift to grandkids often leads well-meaning caregivers to make emotional decisions—like draining retirement accounts to pay for a grandchild’s private preschool—which ultimately harms the entire family structure. A smarter approach relies on structured cash-flow management, ironclad safety nets, and transparent communication. By organizing your present household finances with precision, you can systematically fund a legacy money plan that outlasts you and genuinely enriches the next generation.

Building a Multigenerational Cash-Flow Framework

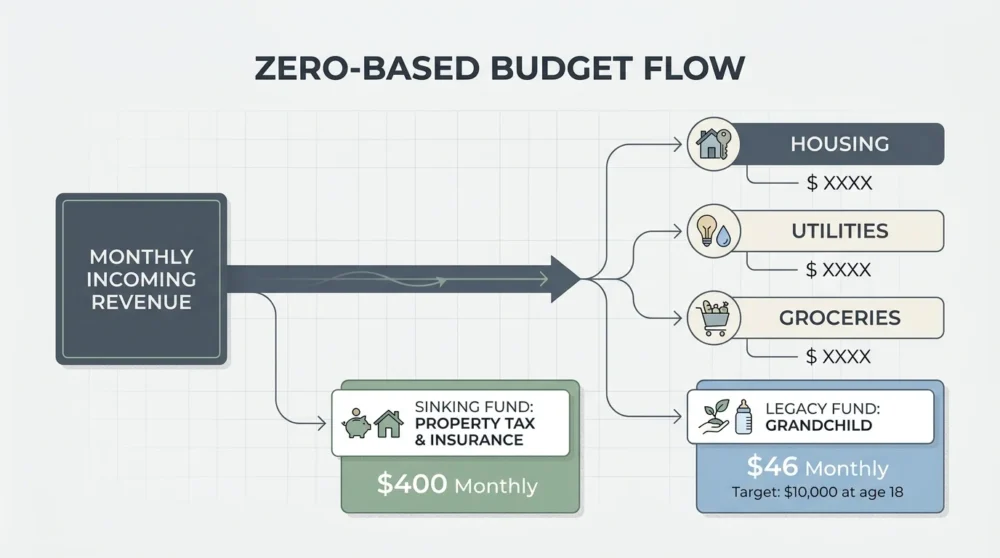

Your ability to leave a lasting inheritance begins with how you manage your monthly household cash flow today. Without a crystal-clear understanding of your incoming revenue and outgoing expenses, any attempt to save for future generations becomes a guessing game. Implement a zero-based budget where every dollar receives a specific job before the month begins. This method ensures your primary obligations—housing, utilities, groceries, and debt service—are fully funded before you allocate surplus cash to legacy goals. When you track your spending rigorously, you often uncover hidden margins in your budget that you can immediately redirect toward your grandchildren’s future.

To insulate your monthly budget from unexpected shocks, you must utilize sinking funds for predictable but irregular expenses. A sinking fund breaks large annual or semi-annual bills into manageable monthly savings targets. For example, if your property taxes and homeowners insurance total $4,800 annually, you automatically transfer $400 each month into a dedicated savings account. You apply this exact same mathematical logic to family planning. If you want to gift your grandchild $10,000 when they turn eighteen, you create a sinking fund for that goal; saving just $46 a month over eighteen years will reach that target even without factoring in compound interest. Relying on automation removes the friction from these decisions, ensuring that you consistently fund both your household maintenance and your legacy aspirations.

Furthermore, grounding your budget in realistic data helps you set boundaries with your adult children regarding current financial support. Recent federal cost studies highlight the staggering expense of raising a family in the modern economy, which explains why so many adult children lean on their aging parents for help. By mapping out your exact cash flow, you can determine precisely how much you can afford to help them with immediate needs—like day-to-day childcare or groceries—without cannibalizing the inheritance you intend to leave behind. A strong cash-flow system grants you the permission to say yes to legacy planning and the confidence to say no to unsustainable current spending.

Constructing Safety Nets for Intergenerational Wealth

A comprehensive legacy plan requires robust safety nets because a single severe medical emergency or extended period of unemployment can entirely wipe out an intended inheritance. Your first line of defense is a fully funded emergency reserve containing three to six months of essential living expenses. This liquid cash sits in a high-yield savings account, acting as a buffer between your family and financial disaster. When the roof leaks or a transmission fails, you pay for the repair directly from the emergency fund rather than liquidating the investments you earmarked for your grandchildren.

Insurance forms the second crucial layer of your family protection system. Life insurance, in particular, offers a highly efficient mechanism for transferring wealth across generations. While term life insurance provides essential income replacement during your peak earning and child-rearing years, permanent life insurance policies can serve as an integral component of a legacy money plan for seniors. The death benefit passes to your beneficiaries tax-free, creating instant liquidity that can fund a grandchild’s education, help them purchase a first home, or cover the costs of your final expenses so your family does not carry the burden. Additionally, securing comprehensive health and long-term care insurance ensures that end-of-life medical costs do not consume the estate you spent decades building.

Beyond insurance and savings, effective estate planning for the family cements your legacy. Relying on a simple will is often insufficient when minor grandchildren are involved. If you leave a lump sum directly to a minor, the courts will step in to control the money until the child reaches adulthood, a process that incurs heavy legal fees and causes unnecessary delays. Instead, utilize legal tools designed for generational wealth transfer. Establishing a revocable living trust allows you to dictate exactly how, when, and under what conditions your grandchildren receive their inheritance; you might stipulate that funds are released in tranches at ages twenty-five, thirty, and thirty-five. For more accessible education planning, 529 college savings plans allow your contributions to grow tax-free when used for qualified educational expenses. You can explore a variety of financial empowerment tools to better understand how beneficiary designations on your retirement accounts interact with these legal structures to bypass the lengthy probate process entirely.

Balancing Long-Range Goals and Legacy Planning

A common pitfall among generous caregivers is prioritizing a grandchild’s financial future over their own retirement security. You must remember a fundamental rule of family finance: your grandchildren can borrow money for their college education, but you cannot secure a loan to fund your retirement. Funding your own golden years is actually the greatest financial gift you can give your family. When you ensure you have enough money to cover your housing, healthcare, and daily living needs through your nineties, you remove the terrifying burden of eldercare from your adult children’s shoulders. Consequently, your children can focus their income on raising your grandchildren, creating a positive ripple effect throughout the family tree.

Once your retirement baseline is thoroughly secured, you can optimize your long-range legacy contributions. Consider the profound impact of front-loading a 529 plan while your grandchildren are still in diapers. The mathematics of compound interest dictate that time is your greatest asset; a single $10,000 investment growing at an average of seven percent annually will become roughly $33,000 by the time a newborn turns eighteen. If you choose to utilize an irrevocable trust or a Uniform Transfers to Minors Act account, you must carefully weigh the tax implications and the impact these assets might have on the child’s future financial aid eligibility.

Demographic shifts require a fresh perspective on how we distribute family wealth. According to national demographic data, multigenerational living arrangements are steadily increasing as families pool resources to combat housing affordability and childcare shortages. In these dynamic environments, leaving money to grandchildren might not mean writing a check upon your passing; it might mean funding an addition to your home so your adult children and grandchildren can live with you rent-free, enabling them to save for their own eventual down payment. True legacy planning adapts to the lived reality of your specific family structure rather than adhering to outdated, rigid financial traditions.

Communication and Household Money Systems

The most sophisticated financial strategies will fail if you do not actively communicate your intentions to your family. Money remains a taboo subject in many households, breeding resentment, entitlement, and confusion. Break this cycle by implementing regular family money meetings. When discussing inheritance tips for seniors with your adult children, clearly outline your estate plan without necessarily revealing exact dollar amounts. Explain the structures you have put in place—such as trusts or 529 plans—so your children can factor your contributions into their own financial projections. Transparency prevents your adult children from over-saving for a college expense you have already covered, freeing up their current cash flow for other pressing household needs.

If you are a grandparent who provides daily care or lives with your grandchildren, you have a unique opportunity to build a household money system that teaches financial literacy in real time. Implement a chore-based allowance system for the grandchildren in your care. Tie specific, age-appropriate household tasks to a modest weekly payout, requiring them to divide their earnings into spending, saving, and giving categories. This practical application of money management reinforces the value of hard work and delayed gratification. By the time they eventually inherit the larger financial gift you have prepared, they will possess the emotional maturity and tactical skills required to manage it responsibly.

You must also establish clear decision rules regarding current financial interventions. When an adult child asks for a loan to cover an emergency, refer back to your predetermined cash-flow framework. Agreeing to formalize any family loans with written repayment schedules protects both your retirement timeline and the familial relationship. By operating your family finances like a well-run organization, you replace emotional reactions with predictable, systems-based responses.

Frequently Asked Questions About Family Finances

How do blended families manage inheritance and legacy planning?

Blended families face complex legacy challenges because standard estate planning defaults often do not align with modern family structures. If you remarry and simply leave all your assets to your new spouse, your biological grandchildren could be entirely disinherited when your second spouse passes away. To prevent this, you must use highly specific beneficiary designations and legal instruments. Establishing a qualified terminable interest property trust allows you to provide income for your surviving spouse for the remainder of their life while guaranteeing that the principal ultimately passes to your chosen grandchildren. You must meticulously update your life insurance and retirement account beneficiaries after any marriage, divorce, or birth to ensure your assets bypass probate and reach the correct heirs.

How can single-income households afford to save for a grandchild’s future?

Single-income homes operate with tighter margins, demanding aggressive prioritization and optimization of existing resources. The non-working spouse plays a critical role in legacy building by driving household efficiency, lowering grocery bills, and managing the administrative side of the budget. To maximize tax advantages, the earning spouse should fund a spousal individual retirement account, which effectively doubles the family’s tax-advantaged retirement space. Furthermore, acquiring adequate life insurance for the non-working caregiver is essential; the economic value of stay-at-home caregiving, managing the household, and coordinating eldercare is immense. Replacing that labor in the event of an untimely death would financially devastate the surviving spouse, completely derailing any long-term inheritance plans.

What steps should we take if debt is eating into our legacy plan?

High-interest consumer debt serves as an aggressive parasite on your family’s wealth, systematically destroying your ability to leave an inheritance. If credit card balances or personal loans are consuming your monthly cash flow, you must temporarily halt your legacy savings to focus entirely on credit rebuilding and debt elimination. Utilize the avalanche method to pay off the balance with the highest interest rate first, or the snowball method to build momentum through small, quick wins. If the debt feels insurmountable, seeking guidance from nonprofit credit counseling agencies can provide structured debt management plans that negotiate lower interest rates with your creditors. Rebuilding your credit score eventually lowers your insurance premiums and borrowing costs, freeing up vital cash to redirect back toward your grandchildren’s inheritance.

How do we handle the crushing cost of childcare while saving for the future?

Childcare currently operates as a second mortgage for many young families, severely restricting their ability to save. As a grandparent, providing free or heavily discounted childcare one or two days a week can dramatically alter your adult child’s financial trajectory, serving as a powerful, immediate financial gift that allows them to save for their own retirement. Additionally, families must rigorously utilize available tax advantages. Maximize dependent care flexible spending accounts through your employer, which allows you to pay for daycare with pre-tax dollars. Ensure you claim the child and dependent care tax credit during tax season. Every dollar saved on current childcare logistics is a dollar that can remain invested and compounding in your generational wealth system.

Take the Next Step for Your Family

Leaving a meaningful legacy is not an accidental outcome; it is the deliberate result of organized systems, consistent communication, and proactive planning. You hold the power to change your family’s financial trajectory for generations by taking control of your current cash flow, fortifying your safety nets, and formalizing your estate plan. Do not wait for the perfect moment to start organizing your household finances. Schedule a family money check-in this week to review your budget, update your beneficiaries, and take the first concrete step toward securing your grandchildren’s financial future.