Navigating your retirement money in 2026 requires aggressive tax planning to protect your wealth from a significantly harsher legislative landscape. Financial planners are sounding alarms because the sweeping tax cuts from the Tax Cuts and Jobs Act officially expired at the end of last year, pushing many retirees into higher marginal brackets and slashing the standard deduction. Securing your financial independence means looking beyond simple budgeting and embracing proactive strategies that shield your income from the Internal Revenue Service. You must optimize your portfolio right now to minimize your lifetime tax burden in this new economic environment. Implementing these eight expert-backed moves will secure your cash flow and keep your savings working directly for your family.

The 2026 Economic Snapshot Driving Retirement Taxes

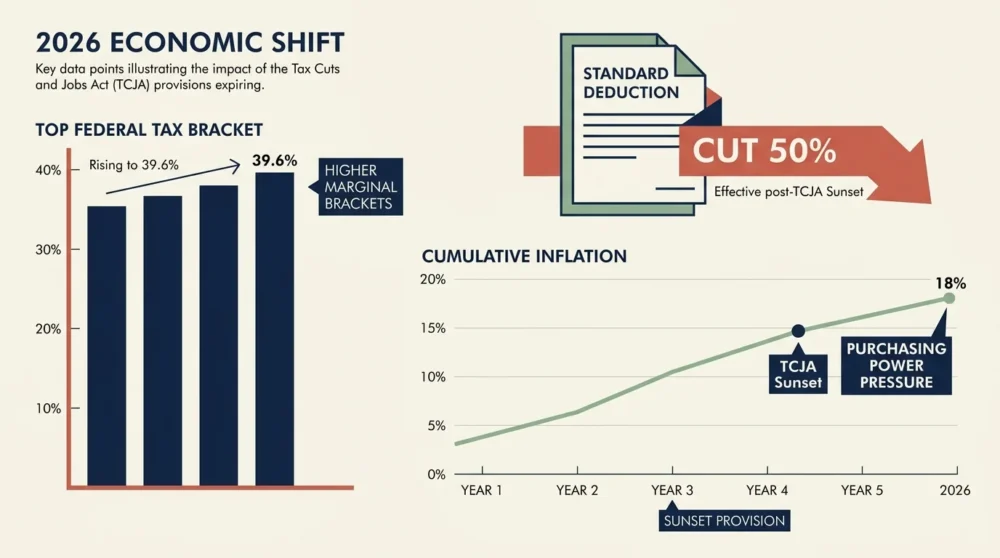

The financial realities facing older adults have shifted dramatically since the beginning of the decade. Following years of aggressive monetary tightening, interest rates have stabilized, but the broader macroeconomic environment leaves little room for complacency. The most significant shock to household finances this year stems directly from the expiration of the Tax Cuts and Jobs Act. Because Congress allowed these individual tax provisions to sunset, marginal tax brackets have reverted to higher pre-2018 levels. The top federal income tax bracket has climbed back to 39.6 percent, and the middle-income brackets have expanded, meaning every additional dollar you withdraw from your traditional retirement accounts faces steeper federal taxation. You can no longer rely on the generous standard deduction of previous years; it has been cut roughly in half, drastically altering how American families must approach deductions and charitable giving.

Furthermore, persistent cumulative inflation over the past five years has permanently raised the floor on everyday living expenses. When you review Federal Reserve data on household wealth, the numbers indicate that while nominal portfolio values remain robust, the actual purchasing power of those portfolios is under severe pressure from both inflation and the new tax regime. Retirees who rely on fixed-income investments or mandatory withdrawals from pre-tax accounts face a dangerous squeeze. If you do not proactively adjust your withdrawal strategies to accommodate these higher tax rates, you risk depleting your principal much faster than your original financial plan projected. Protecting your nest egg requires an active, defensive posture against these compounding legislative and economic headwinds.

Strategic Cash Flow and Investing Moves for Seniors

1. Reassess Roth Conversions in the New Tax Reality

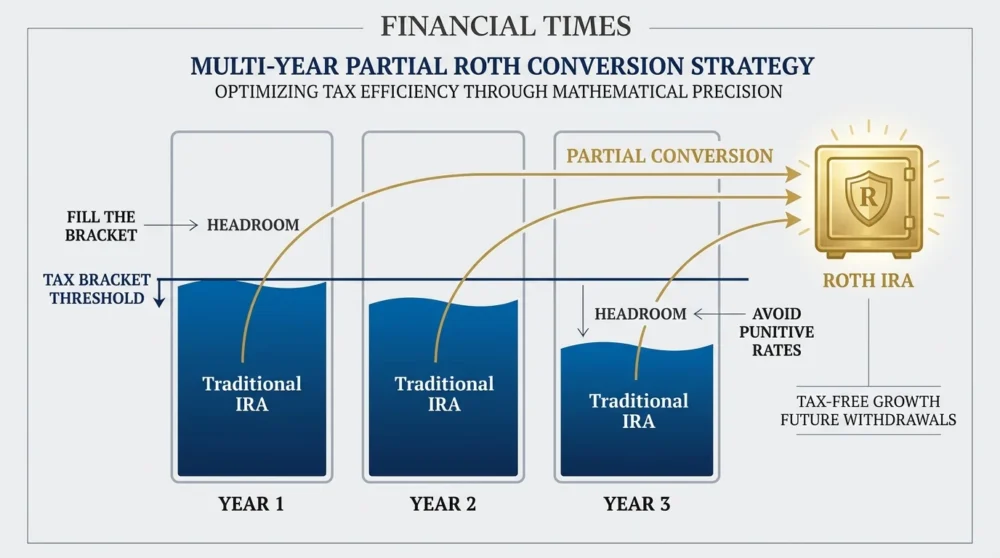

Converting traditional, pre-tax retirement funds into tax-free Roth accounts remains a cornerstone strategy, but the math requires precision in 2026. Because marginal tax rates have increased, executing a massive conversion in a single calendar year could penalize you severely by pushing your income into the highest brackets. Instead, financial advisors recommend utilizing a multi-year partial conversion strategy. You must evaluate your current projected income and identify exactly how much headroom remains in your current tax bracket before crossing into the next marginal rate. By intentionally converting just enough pre-tax money to fill up your current bracket—and stopping right at the threshold—you move funds into a tax-free vehicle without triggering punitive rates. You pay the tax today, but you secure tax-free growth and tax-free withdrawals for the rest of your life, effectively insulating those dollars from any future congressional tax hikes.

2. Leverage Qualified Charitable Distributions to Satisfy RMDs

Required Minimum Distributions act as a massive tax trap for retirees who hold substantial wealth in traditional Individual Retirement Accounts. The government mandates that you begin withdrawing these funds once you reach your applicable starting age, forcing fully taxable income onto your tax return whether you need the cash to pay your bills or not. If you are charitably inclined, the Qualified Charitable Distribution offers a brilliant mechanism to neutralize this tax threat. A Qualified Charitable Distribution allows you to transfer funds directly from your IRA to an eligible nonprofit organization without the money ever appearing as taxable income on your federal return. This move automatically satisfies your mandatory withdrawal requirement while simultaneously keeping your adjusted gross income lower. By keeping that income off your return, you systematically lower your overall tax burden and protect yourself from additional cascading taxes on your Social Security benefits.

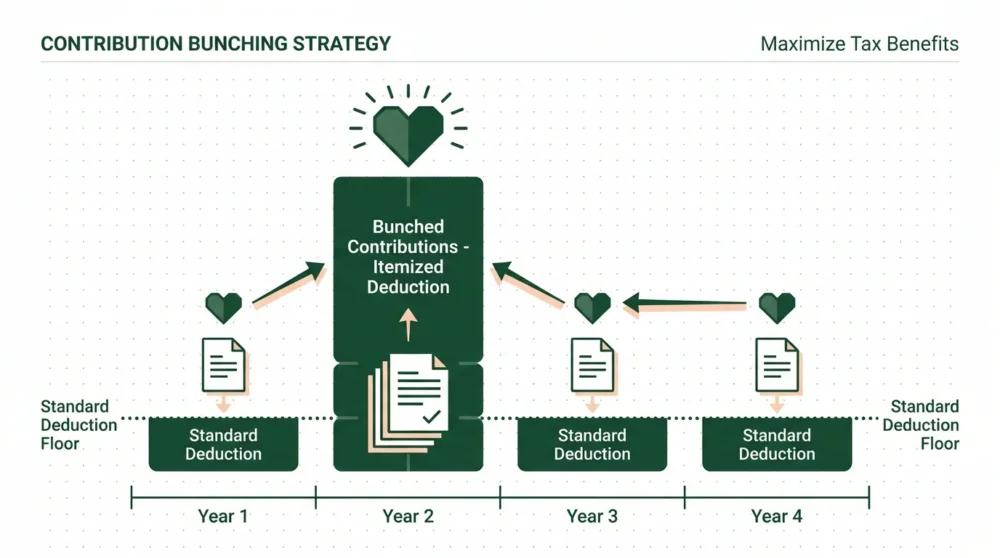

3. Deploy Charitable Contribution Bunching

The expiration of the expanded standard deduction has completely revitalized the strategy of itemizing your tax deductions. For the past eight years, the standard deduction was so high that very few households gained any tax benefit from writing off their charitable contributions. Now that the standard deduction has dropped significantly, financial planners strongly recommend a strategy known as bunching. Rather than giving a steady amount to charity every single year, you consolidate multiple years of planned donations into a single tax year. For example, if you typically donate five thousand dollars annually, you might instead donate fifteen thousand dollars in 2026 and then refrain from giving for the next two years. By utilizing a Donor-Advised Fund, you can take the massive itemized tax deduction in the year you make the large contribution, and then the fund will disburse the money to your chosen charities slowly over time according to your wishes. This approach guarantees your generosity actually lowers your tax bill.

4. Harvest Capital Gains and Losses Strategically

Managing the taxable events in your brokerage accounts requires constant vigilance. Tax-loss harvesting involves intentionally selling investments that have lost value to offset the taxes you owe on investments that have generated a profit. If your losses exceed your gains, you can use up to three thousand dollars of those excess losses to offset your ordinary income, carrying the remainder forward into future tax years. Conversely, if you find yourself in a lower income year—perhaps you have retired but have not yet claimed Social Security or begun taking mandatory withdrawals—you should explore tax-gain harvesting. By intentionally selling highly appreciated stock while your income falls into the zero percent long-term capital gains bracket, you effectively reset the cost basis of those shares completely tax-free. You simply repurchase the shares immediately, as the restrictive wash-sale rules apply only to harvesting losses, not to securing tax-free gains.

Advanced Protections and Healthcare Tax Planning

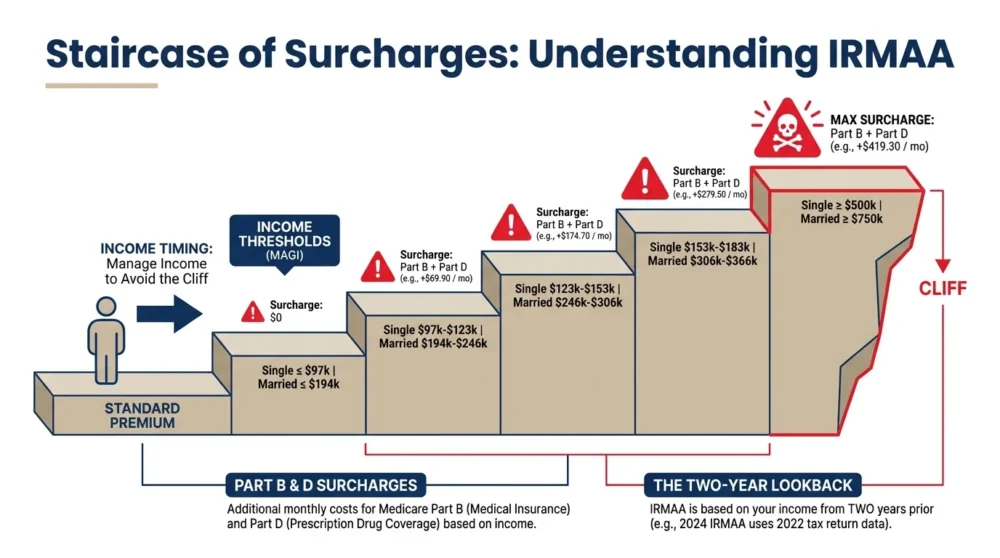

5. Navigate Medicare IRMAA Surcharges with Income Timing

Healthcare costs represent one of the most significant line items in any retirement budget, and the Income-Related Monthly Adjustment Amount operates as a stealth tax on your success. The government bases your Medicare Part B and Part D premiums on your modified adjusted gross income from two years prior. This means an unusual spike in your 2026 income will trigger dramatically higher healthcare premiums in 2028. Because the surcharge brackets act as hard cliffs, earning just one single dollar over the limit forces you to pay the exact same penalty as someone who earned thousands of dollars more. You must rigorously control your recognized income. If a life-changing event such as retirement or the death of a spouse caused your income to drop after a high-earning year, you should immediately file an appeal using form SSA-44 with the Social Security Administration to request an adjustment based on your new, lower-income reality. Review the official Medicare pricing framework to understand precisely where these dangerous income cliffs reside.

6. Maximize Health Savings Accounts as Stealth Retirement Vehicles

If you have not yet enrolled in Medicare and still utilize a high-deductible health plan, a Health Savings Account stands as the single most powerful tax shelter available in the American financial system. These accounts provide a unique triple-tax advantage; your contributions lower your taxable income, the investments grow entirely tax-free, and your withdrawals escape taxation completely when used for qualified medical expenses. Financial advisors recommend treating this account as a supplementary retirement fund rather than a checking account for current medical bills. If your cash flow permits, pay for your current copays and prescriptions out of pocket, allowing the funds inside the account to compound aggressively in the stock market over decades. Once you turn sixty-five, the penalties for non-medical withdrawals vanish, allowing you to pull the money out for any reason whatsoever simply by paying ordinary income tax, perfectly mirroring a traditional IRA while retaining the ability to withdraw funds tax-free for healthcare.

7. Relocate to Tax-Friendly Jurisdictions Carefully

With federal tax rates increasing, the state you choose to call home plays an outsized role in your financial survival. Relocating from a state with punitive income and estate taxes to a jurisdiction that does not tax income or retirement distributions can save you tens of thousands of dollars annually. However, state revenue departments have grown incredibly aggressive in auditing wealthy seniors who claim to have moved. Simply buying a condo in a tax-free state will not satisfy auditors. You must definitively sever your legal and social ties to your former, high-tax domicile. This requires passing the 183-day physical presence test, transferring your driver’s license, registering your vehicles, moving your voter registration, shifting your primary medical providers, and relocating your most valuable family heirlooms. Keep meticulous logs of your travel and spending to prove your primary residence has permanently changed, as auditors will rigorously examine your credit card transactions and flight records.

8. Shield Your Estate After the Lifetime Exemption Drop

The 2026 tax landscape introduces a massive threat to generational wealth transfer. The historically high lifetime estate and gift tax exemption—which hovered around fourteen million dollars per individual—plummeted by roughly fifty percent when the tax cuts expired. Millions of families who previously considered themselves immune to estate taxes suddenly face the prospect of the federal government confiscating a massive percentage of their legacy upon death. You must immediately evaluate aggressive gifting strategies to reduce the size of your taxable estate. Utilize your annual gift tax exclusion to move maximum allowable cash to your heirs without dipping into your lifetime exemption. Furthermore, explore complex legal structures such as Spousal Lifetime Access Trusts or Irrevocable Life Insurance Trusts with your attorney to lock away highly appreciating assets outside of your taxable estate. Acting decisively now prevents the government from becoming the largest beneficiary of your life’s work.

Risk, Compliance, and Avoiding Costly Penalties

Executing advanced tax maneuvers requires strict adherence to regulatory deadlines, as the Internal Revenue Service penalizes mistakes relentlessly. Failing to take your full mandatory withdrawal from your retirement accounts triggers an automatic excise tax on the amount you failed to withdraw. While recent legislative updates reduced this penalty from fifty percent to twenty-five percent—and potentially down to ten percent if corrected quickly—it remains a devastating loss of capital that you must avoid by double-checking your required minimum distribution calculations every autumn.

Beyond regulatory penalties, retirees must remain vigilant against external threats targeting their wealth. The chaotic transition into the new 2026 tax code has spawned a massive wave of criminal enterprises seeking to exploit consumer confusion. Phantom tax preparers and fraudulent settlement firms frequently target older Americans with false promises of eliminating tax debt or bypassing the new, higher tax brackets entirely. These scammers disappear with your upfront fees and often steal your sensitive personal data in the process, leaving you vulnerable to identity theft and completely liable for the fraudulent returns filed in your name. You must only engage with credentialed fiduciaries, certified public accountants, or enrolled agents. You can monitor emerging threats by reviewing Consumer Financial Protection Bureau reports on elder financial exploitation to ensure you recognize the warning signs of financial predators.

Frequently Asked Questions About Retirement Taxes

At what age do I stop paying taxes on Social Security?

You never automatically age out of paying taxes on your Social Security benefits. The taxation of your benefits depends entirely on your combined income, which the government calculates by adding your adjusted gross income, your nontaxable interest, and half of your Social Security benefits for the year. If this combined total exceeds specific thresholds set by Congress, up to eighty-five percent of your benefits become subject to federal income tax, regardless of whether you are seventy years old or one hundred years old. Proactive income planning remains the only legal method to reduce the taxation of your benefits.

Does the 2026 tax code change affect my existing Roth IRA?

The expiration of the tax cuts does not negatively impact the foundational rules governing existing Roth accounts. The money you have already successfully contributed or converted into a Roth vehicle remains completely insulated from the new, higher income tax brackets. Provided you follow the five-year aging rules and have reached the qualifying age of fifty-nine and a half, your withdrawals—including all the investment growth—remain entirely tax-free. This characteristic makes the Roth IRA an incredibly valuable defensive asset during periods of rising federal tax rates.

How do I know if I am subject to the Medicare IRMAA surcharge?

You determine your exposure to the Medicare surcharge by examining your federal tax return from exactly two years ago. The Social Security Administration automatically reviews your modified adjusted gross income from that prior year; for example, your 2026 premiums depend entirely on the income you reported on your 2024 tax return. If your income surpassed the published threshold for your filing status, you will receive an official determination notice in the mail outlining the exact extra premium amount you must pay for both your medical and prescription drug coverage for the upcoming calendar year.

Can I still deduct my medical expenses under the new tax laws?

You can definitely still deduct your medical expenses, and it may actually be easier to do so in 2026. Because the standard deduction has decreased, more households will find it advantageous to itemize their deductions. You are legally permitted to deduct qualified out-of-pocket medical and dental expenses that exceed seven and a half percent of your adjusted gross income. By carefully tracking expenses such as long-term care premiums, accessibility home modifications, and major dental work, and utilizing the Bureau of Labor Statistics consumer price metrics to project rising healthcare costs, you can strategically group these expenses into a single calendar year to maximize your valuable tax deduction.

Take Action Today

You cannot afford to passively ride out the turbulence of the 2026 tax landscape. Begin your defensive planning immediately by pulling your most recent tax return and scheduling a comprehensive review session with a certified public accountant or credentialed financial advisor. Project your current income against the newly elevated tax brackets and calculate exactly how the reduced standard deduction alters your baseline financial plan. Identify which of these eight strategies—from executing precision Roth conversions to bunching your charitable contributions—best fits your specific cash flow needs. Gather your investment statements, map out your anticipated healthcare expenses, and initiate these structural changes before the fourth quarter arrives. Taking decisive action today ensures you maintain total control over your wealth and secures the comfortable, independent retirement you worked decades to achieve.