Preserving your life savings while generating a reliable income stream requires you to navigate a complex web of tax laws and market forces. You spend decades accumulating wealth, but withdrawing that money incorrectly can drain your portfolio years earlier than anticipated. Today’s retirees face an unprecedented combination of prolonged inflation, shifting tax brackets, and unpredictable market returns. Financial experts consistently warn that seemingly minor missteps—such as pulling from the wrong account first or triggering hidden Medicare surcharges—can cost you thousands of dollars annually. By understanding these nine common retirement withdrawal mistakes, you can proactively protect your assets, minimize your tax burden, and ensure your money lasts for your entire lifetime.

The Economic Snapshot Reshaping Retirement

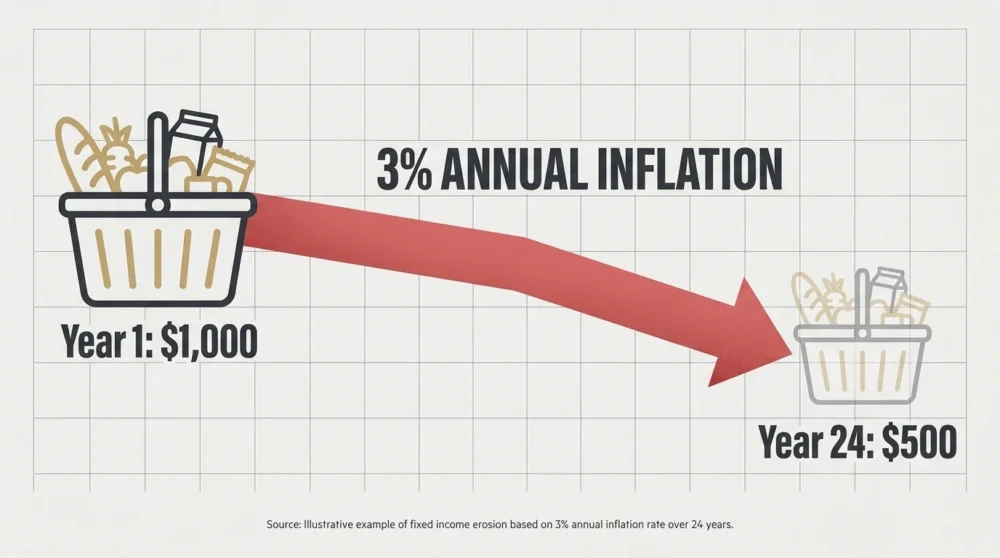

The financial landscape awaiting today’s retirees looks vastly different than the one previous generations experienced. For years, low inflation and steadily rising equity markets provided a forgiving environment for retirement withdrawals; however, recent economic shifts have severely complicated the income equation. The Federal Reserve’s battle against consumer price hikes pushed interest rates to levels unseen in decades, altering the dynamics of both bond yields and borrowing costs. Meanwhile, persistent inflation directly assaults your purchasing power. If inflation averages just three percent annually, the real value of your fixed income will be cut in half over a typical twenty-four-year retirement period. You can no longer rely on a static withdrawal plan when everyday expenses fluctuate aggressively. The Bureau of Labor Statistics regularly reports on the Consumer Price Index, highlighting how deeply these elevated costs cut into household budgets. Because you live on a fixed income, even a slight miscalculation in how much you withdraw to cover these rising costs can drastically shorten the lifespan of your investment portfolio. Understanding the current economic reality represents the first critical step in engineering a resilient, inflation-adjusted withdrawal strategy.

The 9 Costliest Retirement Withdrawal Mistakes

Securing your financial independence involves more than just selecting the right mutual funds; it requires executing a flawless distribution strategy. Financial advisors frequently identify the following nine errors as the most destructive forces facing modern retirees.

Mistake 1: Ignoring the Tax Sequence of Withdrawals

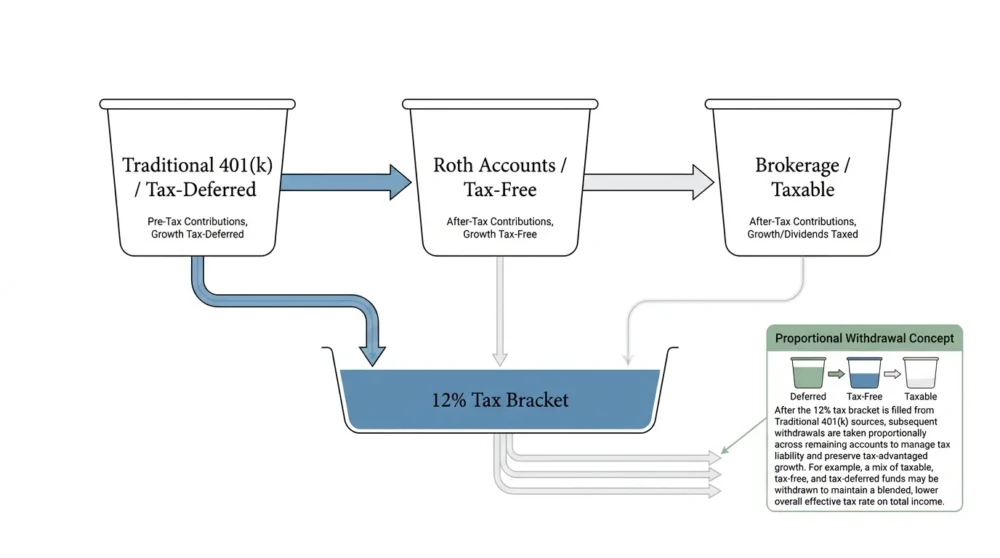

When you retire, you transition from accumulating assets to drawing them down, which fundamentally changes your relationship with federal tax laws. Most retirees hold a mixture of traditional tax-deferred accounts, tax-free Roth accounts, and taxable brokerage accounts. A devastating mistake involves withdrawing funds haphazardly or pulling strictly from your largest tax-deferred account first. If you withdraw massive sums from a traditional 401(k), you add ordinary income to your tax return; this rapidly pushes you into a significantly higher marginal tax bracket. Financial experts recommend implementing a proportional withdrawal sequence. You minimize your lifetime tax liability by filling up lower tax brackets with traditional account withdrawals, then using Roth distributions to cover any additional spending needs, keeping more capital safely invested.

Mistake 2: Missing Required Minimum Distribution Deadlines

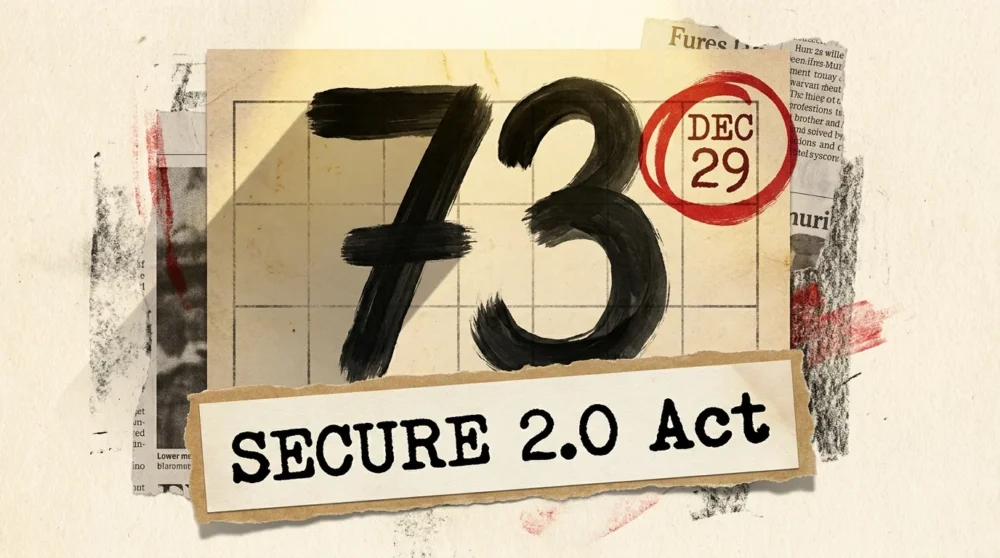

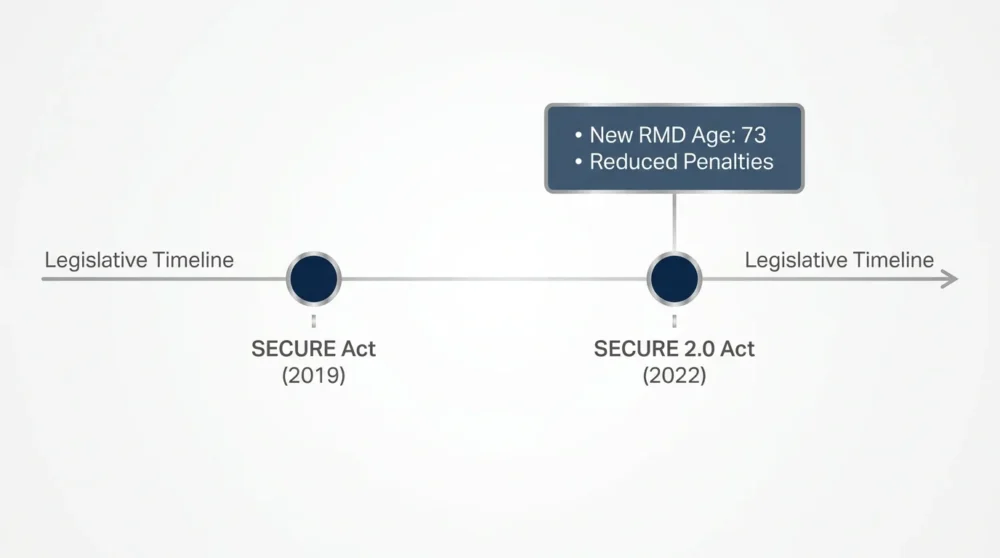

The federal government provides upfront tax benefits for retirement accounts with the expectation that you will eventually pay taxes on the distributions. Required minimum distributions represent the mandatory amount you must withdraw from traditional accounts each year. Following recent legislative adjustments under the SECURE 2.0 Act, the starting age for these distributions shifted to seventy-three. Missing your distribution deadline triggers an aggressive penalty. The Internal Revenue Service rules regarding required distributions previously imposed a draconian fifty percent excise tax on unwithdrawn amounts; today, lawmakers reduced this to twenty-five percent, yet it remains a catastrophic loss of wealth. You must calculate these mandatory distributions accurately based on your exact account balances and life expectancy factors. Automating these withdrawals late in the year ensures you never miss the strict December deadline.

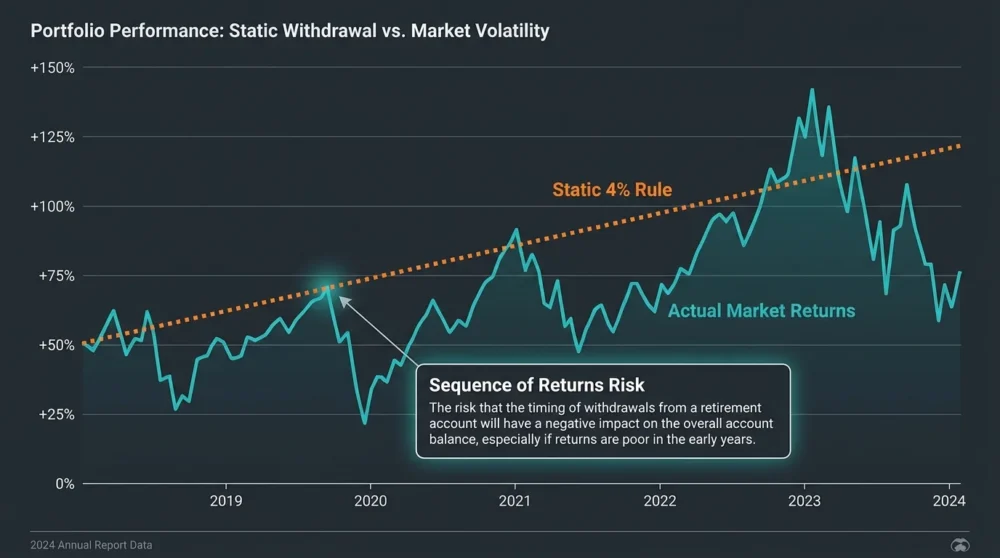

Mistake 3: Blindly Following the Four Percent Rule

Many investors anchor their entire financial plan to the four percent rule, a guideline suggesting you can safely withdraw four percent of your portfolio in year one and adjust for inflation thereafter. However, financial planners warn that treating this historical benchmark as an absolute law invites financial disaster. Market conditions fluctuate, meaning a static withdrawal strategy forces you to liquidate assets aggressively during severe market downturns. Instead of blindly following a rigid formula, you need a dynamic, adaptable spending plan. Experts advocate for utilizing guardrails—automatically reducing your withdrawal rate when markets plunge and granting yourself a slight raise during sustained bull markets. This flexible approach preserves your principal during turbulent economic periods and ensures your income sustains your longevity.

Mistake 4: Claiming Social Security at the Wrong Time

Treating your investment portfolio and your guaranteed income streams as separate entities represents a profound planning failure. Claiming Social Security at age sixty-two locks in a permanently reduced monthly benefit, drastically increasing the pressure on your personal savings to bridge the income gap. Conversely, the Social Security Administration guidelines on claiming ages confirm that delaying your claim allows your benefits to grow by a guaranteed eight percent for every year you wait past your full retirement age until age seventy. You must strategically weigh your life expectancy, tax bracket, and portfolio size before filing. Sometimes, drawing down your individual retirement accounts early to facilitate a delayed Social Security claim creates a significantly larger, inflation-protected income floor for the final decades of your life.

Mistake 5: Failing to Adjust for Inflation and Market Volatility

Entering retirement exposes you to sequence of returns risk, the mathematical danger of experiencing severe market declines early in your withdrawal phase. If you pull funds from an equity portfolio while share prices plummet, you lock in permanent losses and destroy the shares needed to generate future growth. Failing to adjust your withdrawals for this volatility mathematically guarantees you will deplete your savings prematurely. To combat this risk, you must maintain a cash buffer or a dedicated bucket of short-term, low-risk investments. When a bear market strikes, you simply halt stock liquidations and draw from your cash reserves to cover living expenses. This strategic maneuvering gives your growth-oriented investments the crucial time necessary to recover their lost value.

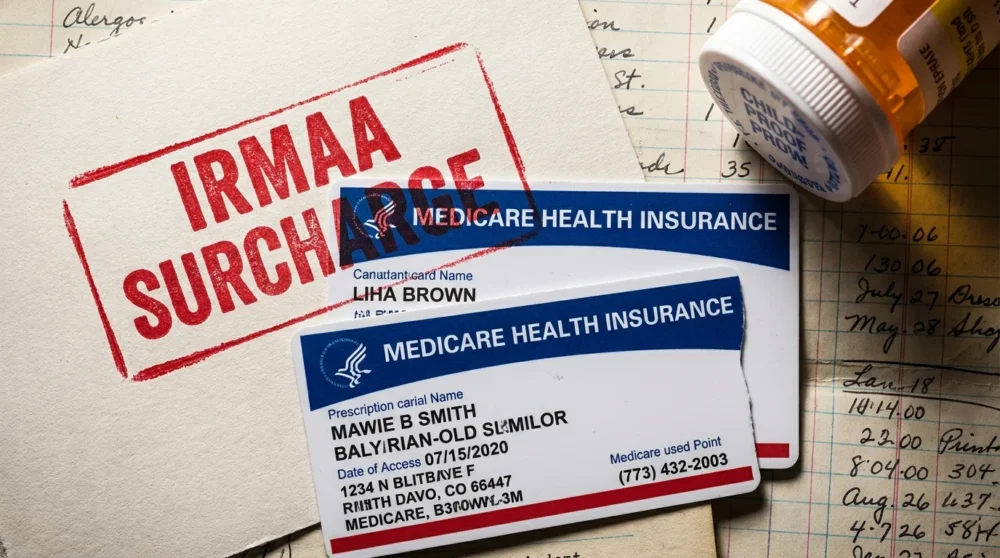

Mistake 6: Overlooking Medicare Premium Surcharges

Retirees often assume their healthcare premiums remain static, completely missing the hidden tax known as the Income-Related Monthly Adjustment Amount. The federal government determines your Medicare Part B and Part D premiums based on your modified adjusted gross income from two years prior. A large, unplanned withdrawal from a traditional retirement account or a massive Roth conversion can accidentally push your income past Medicare premium surcharge thresholds, triggering steep premium hikes that persist for an entire year. These sudden premium spikes drastically reduce your net monthly income. You must meticulously project your taxable distributions each year and cap your taxable withdrawals just below the surcharge thresholds to prevent your healthcare costs from devouring your budget.

Mistake 7: Holding Too Much Cash or Taking Too Little Risk

Fearing a stock market crash, conservative retirees frequently park the majority of their wealth in cash equivalents or low-yield bonds. While this strategy temporarily eliminates short-term volatility, it introduces a much more insidious threat: purchasing power erosion. Over a thirty-year retirement horizon, inflation systematically decimates the real value of stagnant money. If your portfolio fails to generate growth that outpaces the rising cost of goods and services, your standard of living will inevitably collapse. Financial advisors emphasize that you must maintain a carefully calibrated allocation to equities throughout your retirement. A balanced portfolio provides the essential engine for long-term capital appreciation, ensuring your income stream can expand alongside the ever-increasing costs of housing, energy, and daily necessities.

Mistake 8: Underestimating Healthcare and Long-Term Care Costs

Budgeting solely for housing, food, and leisure leaves you dangerously unprepared for the staggering reality of medical expenses. Industry research consistently projects that an average retired couple will require hundreds of thousands of dollars to cover out-of-pocket healthcare costs throughout their later years, completely excluding the exorbitant price of long-term care. Medicare does not cover extended stays in nursing facilities or in-home custodial care, which can easily exceed six figures annually. Ignoring these impending liabilities forces you to drain your core portfolio at an unsustainable velocity. You must integrate a dedicated healthcare funding strategy—such as maximizing a Health Savings Account or securing comprehensive long-term care insurance—long before these inevitable medical crises materialize.

Mistake 9: Falling Victim to Fraud and Predatory Scams

The most perfectly executed withdrawal strategy crumbles instantly if you fall victim to financial exploitation. Cybercriminals and predatory scam artists disproportionately target retirees, knowing that older adults command substantial liquid assets. Sophisticated phishing emails, fraudulent investment opportunities, and aggressive impersonation schemes strip billions of dollars from vulnerable households every year. Unlike market losses, which eventually recover, stolen funds disappear permanently. You must aggressively lock down your digital footprint, utilizing two-factor authentication on every financial platform. The Consumer Financial Protection Bureau resources on elder fraud emphasize that maintaining a healthy skepticism regarding unsolicited financial communications is mandatory to safeguard your life’s work.

Regulatory Risks and Compliance Thresholds

The legislative framework surrounding retirement accounts remains in a constant state of flux, forcing you to remain vigilant to avoid harsh penalties. The SECURE 2.0 Act introduced sweeping changes that directly impact your withdrawal timeline and tax obligations. Beyond the delayed age for mandatory withdrawals, the law also instituted strict new timelines for beneficiaries. If you leave your retirement accounts to your children, the previous lifetime stretch IRA rules no longer apply for most non-spouse beneficiaries. Instead, your heirs must completely empty the inherited account within ten years, potentially triggering a massive tax burden during their highest earning years. You must actively coordinate your beneficiary designations with your current withdrawal strategy to optimize generational wealth transfer. Additionally, Congress regularly adjusts standard deductions, tax brackets, and catch-up contribution limits, meaning a withdrawal strategy drafted five years ago may already be dangerously obsolete. You must conduct an annual compliance review to ensure your distributions align with the most recent federal regulations and state tax laws.

Frequently Asked Questions

Should I stop withdrawing if the stock market crashes?

You should not completely halt withdrawals during a market downturn if you rely on that income to pay for basic living expenses. Instead, you need a cash buffer or a dedicated bucket of safe, short-term investments that you can tap into when equities decline. By spending down your cash reserves during a bear market, you allow your equity investments the time they need to recover without selling shares at a deep discount.

How do dividends factor into my withdrawal rate?

Dividends provide a natural stream of cash flow that can satisfy a portion of your income needs without requiring you to sell underlying shares. When evaluating your overall withdrawal strategy, you must count dividend payments as part of your total withdrawal percentage. If your portfolio yields two percent in dividends and your target withdrawal rate is four percent, you only need to liquidate two percent of your principal to meet your income goals.

Can I change my withholding taxes on retirement distributions?

You maintain full control over the amount of federal and state taxes withheld from your retirement account distributions. By filing a form W-4P with your financial custodian, you can specify exactly how much tax they should set aside from each withdrawal. Adjusting this withholding amount helps you avoid a surprise tax bill in April and prevents you from facing underpayment penalties if your other sources of income push you into a higher tax bracket.

What happens if I withdraw from my 401(k) before age 59 and a half?

Taking money out of a tax-advantaged retirement account before reaching age 59 and a half generally triggers a 10 percent early withdrawal penalty on top of standard income taxes. However, the tax code outlines several specific exceptions to this rule. You can avoid the penalty if you use the funds for qualifying medical expenses, if you separate from service the year you turn 55, or if you establish a series of substantially equal periodic payments based on your life expectancy.

Your Next Steps for a Secure Retirement

Securing your financial independence requires you to transition from a saver mentality to a strategic spender mentality. You must take concrete steps today to fortify your withdrawal strategy against taxes, inflation, and market volatility. First, calculate your baseline living expenses and identify exactly how much income you need to generate from your investment portfolio each month. Second, map out the tax status of every retirement account you own to determine the most efficient sequence for tapping those funds. Third, log into your social security portal to review your earnings record and project your monthly benefits at various claiming ages. Finally, consider sitting down with a fee-only fiduciary financial advisor who can run a sophisticated stress test on your portfolio. By proactively addressing these vulnerabilities now, you build a resilient income plan that allows you to enjoy the retirement you worked so hard to achieve.