Securing your financial future requires more than just aggressive saving; it demands strict avoidance of IRS penalties that can erode decades of hard-earned growth. You need a precise understanding of the tax code to keep your nest egg intact and compounding effectively. As inflation squeezes household budgets and regulatory changes alter the investing landscape, a simple paperwork error can suddenly trigger severe tax liabilities. Countless investors inadvertently forfeit thousands of dollars to the government each year because they misunderstand a rollover rule or miss a required withdrawal threshold. Protecting your wealth means mastering the intricate rules governing your accounts. You can confidently preserve your capital and maximize your financial independence by identifying and sidestepping these eight costly missteps.

The Current Economic Snapshot of Retirement Savings

The macroeconomic environment presents profound challenges for American savers navigating the complex tax code. Rising living costs and prolonged high interest rates tempt households to tap retirement savings prematurely, setting the stage for severe penalties. According to the Survey of Consumer Finances, families rely heavily on tax-advantaged accounts to build long-term wealth, making these portfolios the bedrock of financial security. However, fluctuating inflation strains household cash flow, leading many to improperly view workplace savings as an emergency fund. With recent legislative changes under the SECURE 2.0 Act altering contribution limits and distribution schedules, staying compliant has never been more difficult. You must understand how the broader economy interacts with federal tax laws to shield your portfolio from unnecessary taxation and administrative fines. Mastering these regulations ensures your money remains invested during market volatility.

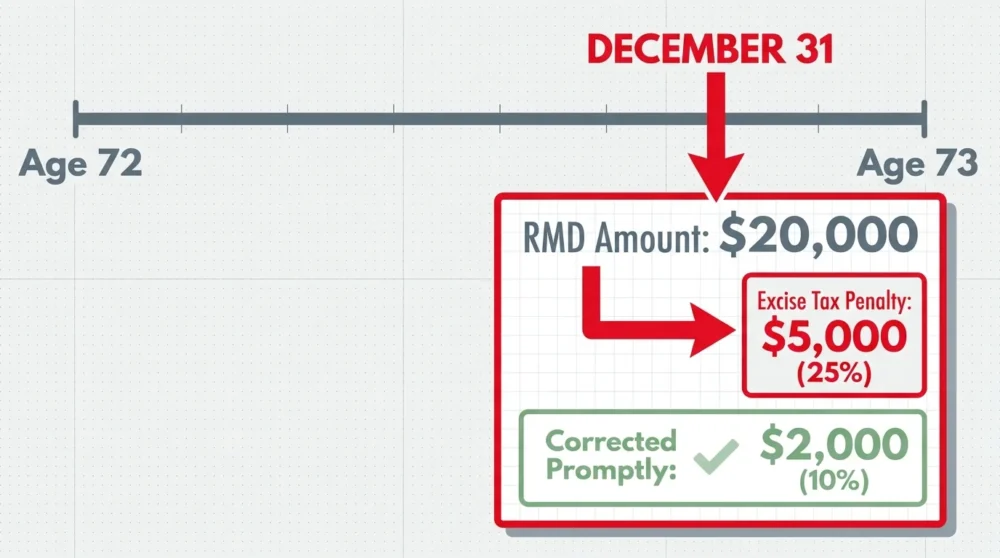

Mistake 1: Ignoring Required Minimum Distributions

One of the most severe penalties embedded in the federal tax code stems from missing your mandatory withdrawals. Once you reach age 73, the government requires that you begin withdrawing a calculated amount from your traditional pre-tax accounts annually. Failing to withdraw the correct minimum amount by the December 31 deadline triggers a steep excise tax. While recent reforms reduced this penalty from 50 percent to 25 percent of the shortfall—and to 10 percent if corrected promptly—it remains a devastating blow. If your required distribution is $20,000 and you forget to take it, you face an immediate $5,000 penalty. You must calculate these figures accurately each year based on your ending account balance and current life expectancy factor. Utilizing the official uniform lifetime table published by the Internal Revenue Service guarantees compliance.

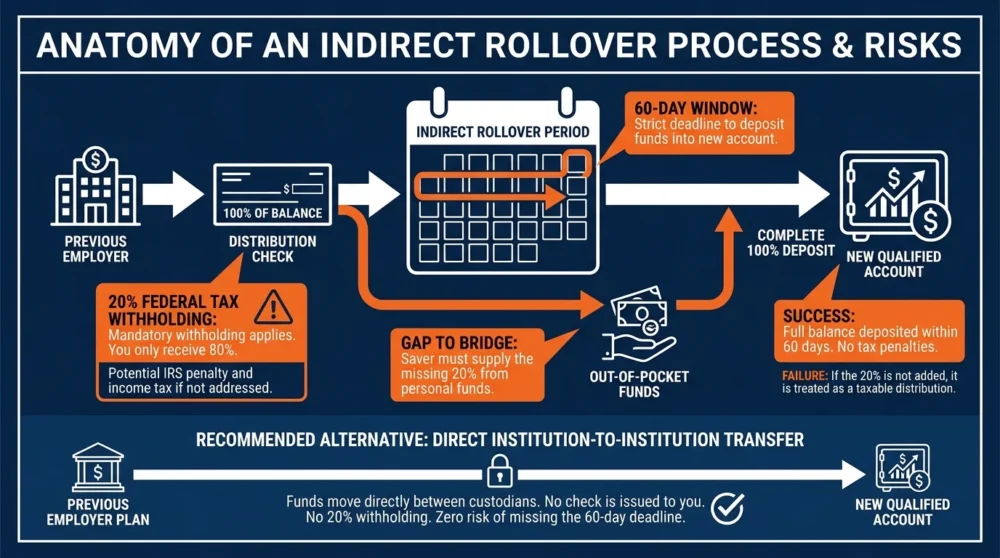

Mistake 2: Executing Indirect Rollovers Improperly

Moving money between different brokerages represents a routine procedure, but executing an indirect rollover carries immense financial risk. During an indirect rollover, your previous financial institution sends the account funds directly to you. You then possess exactly 60 days to deposit the gross amount into a new qualified account. If you miss this strict deadline by a single day, the IRS treats the distribution as fully taxable income. If you are under age 59 and a half, you also incur a 10 percent early withdrawal penalty. Furthermore, your previous employer must legally withhold 20 percent for taxes before cutting the check, meaning you must use out-of-pocket funds to replace the missing 20 percent. Always insist on a direct institution-to-institution transfer to eliminate deadline pressure and bypass mandatory tax withholding.

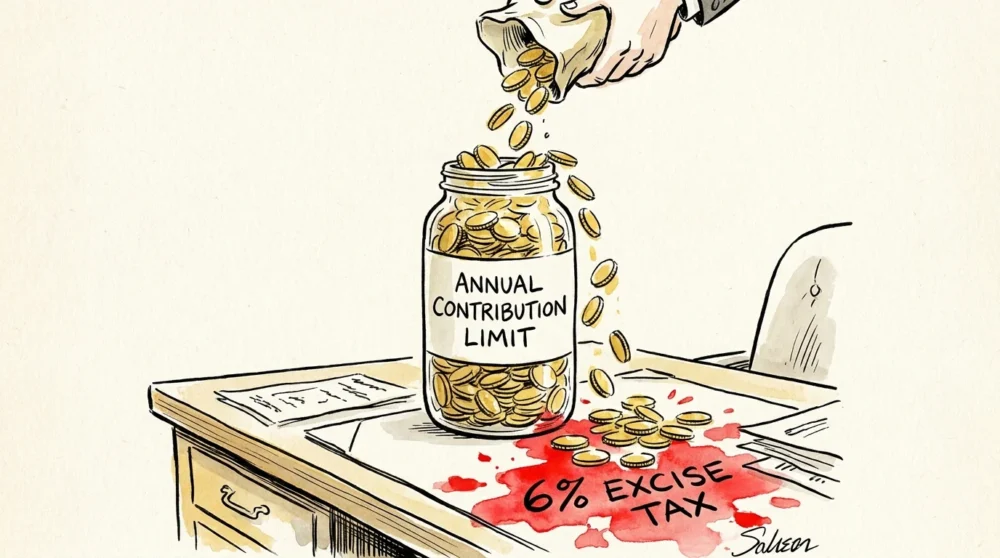

Mistake 3: Overcontributing to Your Tax-Advantaged Accounts

Aggressive saving builds substantial wealth, but depositing more cash than the IRS legally allows creates massive paperwork headaches and recurring fines. The government sets strict annual contribution limits for both individual accounts and workplace plans. If you exceed these legally defined limits, the IRS automatically imposes a 6 percent excise tax on the excess amount for every single year that the extra money remains parked in the account. This penalty compounds annually, silently draining your resources. This costly mistake frequently occurs when individuals change jobs mid-year and accidentally double up on their payroll deductions across two different employers. It also happens when a taxpayer’s adjusted gross income unexpectedly increases, disqualifying them from direct after-tax contributions. You must monitor cumulative contributions across all portfolios and withdraw excess funds before the tax filing deadline.

Mistake 4: Taking Early Withdrawals Without Meeting Exceptions

Tapping into your retirement funds before reaching the critical age threshold of 59 and a half represents a structurally damaging financial error. The IRS broadly imposes a punitive 10 percent early withdrawal penalty on the distributed amount, levied alongside standard federal and state income taxes. If you withdraw $50,000 from your workplace plan to pay off credit card debt, you could lose nearly half of that money to taxes and penalties. While the tax code provides narrow exceptions—such as distributions for qualified first-time home purchases, higher education expenses, or significant medical bills—auditors heavily scrutinize these legal loopholes. Utilizing these exceptions requires flawless documentation. You should exhaust all other available cash flow options, including liquidating standard brokerage assets or utilizing emergency savings funds, before considering a premature withdrawal from a protected account.

Mistake 5: Failing to Understand Prohibited Transaction Rules

Investors who utilize specialized self-directed accounts to purchase alternative assets like commercial real estate face a uniquely dangerous set of regulations. The federal government explicitly forbids using your retirement funds to engage in any prohibited transactions with disqualified persons, which includes yourself, your spouse, your parents, and your lineal descendants. For instance, you absolutely cannot use your protected account to purchase a residential rental property and then allow your child to live there rent-free. If you commit a prohibited transaction, the IRS automatically considers your entire account fully distributed on the first day of the calendar year the transaction occurred. This disastrous outcome makes the total balance immediately taxable. You must consult a credentialed tax attorney or specialized fiduciary before executing any alternative investment strategy within these structures.

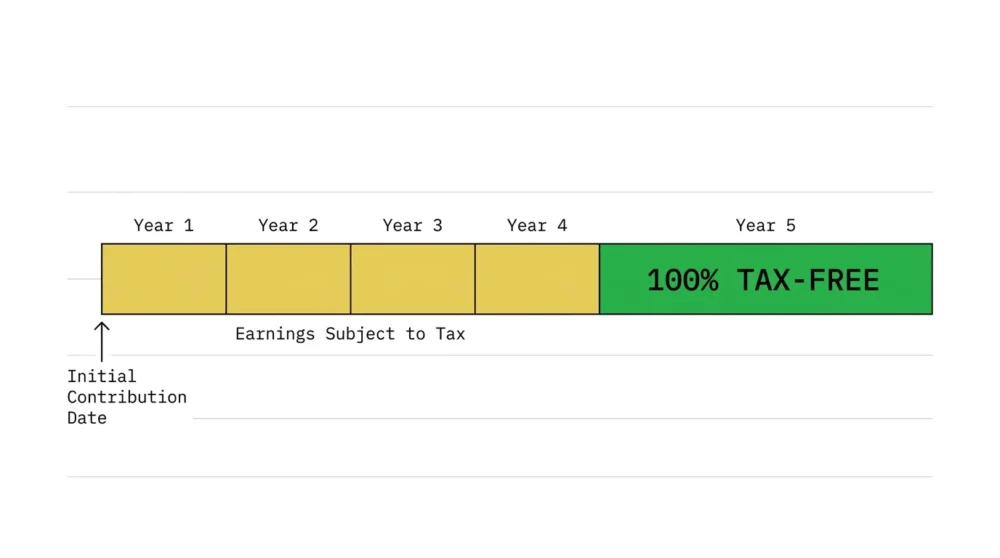

Mistake 6: Missing the Five-Year Rule for Roth Distributions

After-tax accounts offer the ultimate promise of tax-free growth, but these benefits remain completely contingent upon strict adherence to the five-year aging rule. Many investors mistakenly assume they can withdraw their investment earnings tax-free at any time after reaching retirement age. However, the IRS dictates that your very first after-tax account must remain open and funded for a minimum of five distinct tax years before you can pull out the accumulated earnings tax-free. Furthermore, a completely separate five-year rule applies to each individual tax conversion you execute; you must wait five full years to withdraw the specifically converted principal penalty-free if you are currently under age 59 and a half. Misunderstanding these complex, overlapping requirements frequently results in unexpected tax bills. Keep meticulous, long-term records of your initial account opening dates to avoid taxation.

Mistake 7: Triggering the Wash Sale Rule Across Portfolios

The wash sale rule represents a familiar concept for active investors, but its application across different types of financial accounts frequently catches individuals off guard. The IRS states that if you sell a security at a capital loss in a standard taxable account and then purchase a substantially identical security within 30 days, you cannot claim the capital loss deduction. The most critical mistake occurs when investors sell a losing stock in their taxable account and subsequently buy that exact same stock inside their tax-advantaged retirement account. When this cross-account violation happens, the capital loss is permanently and irreversibly disallowed. Your cost basis in the protected account cannot adjust upward to absorb the loss, meaning the intended tax benefit of your losing trade is completely destroyed. You must coordinate your trading strategies holistically to avoid this penalty.

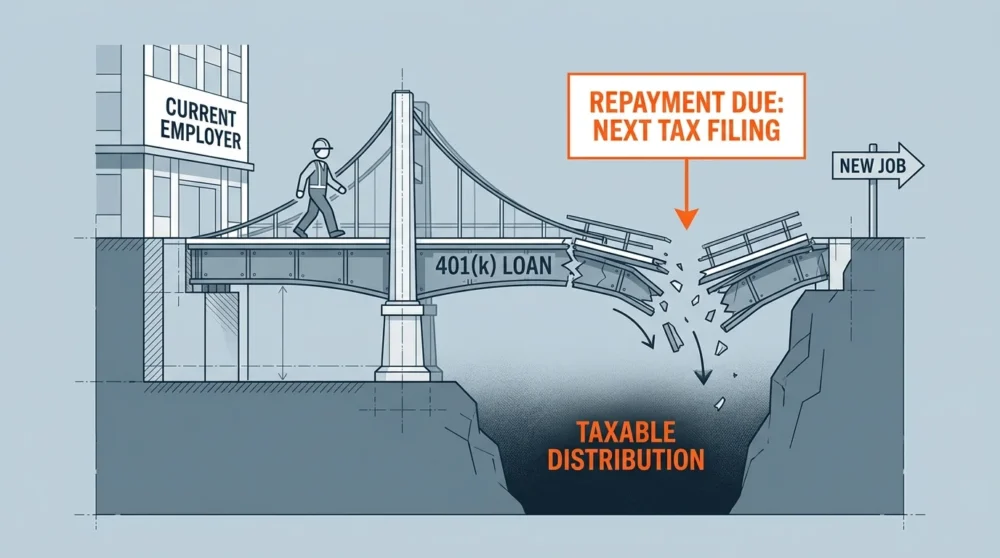

Mistake 8: Defaulting on a Workplace Loan

Borrowing cash directly against your workplace retirement plan seems like a convenient way to access capital, but these loans harbor hidden structural dangers that trigger massive tax consequences. When you take out a loan against your portfolio, you borrow your own invested money and pay yourself back with interest. However, if you leave your current job—whether you voluntarily resign, face a layoff, or experience termination—the outstanding loan balance usually becomes due almost immediately. If you cannot rapidly repay the full remaining amount by the strict deadline set by your plan administrator, the loan officially defaults. The IRS treats the entire defaulted balance as a permanent, taxable distribution. You owe standard ordinary income tax on the total unpaid amount, plus the standard 10 percent early withdrawal penalty if you remain under the qualifying age.

Strategy Pillars for Penalty-Free Retirement Planning

Building a highly resilient financial plan requires integrating cash flow management, credit utilization, disciplined investing, and strict asset protection. Your foundational pillar must involve cash flow optimization. Maintain a highly liquid emergency fund outside of your retirement portfolios to handle unexpected expenses without resorting to early withdrawals. By building a cash reserve equal to at least six months of baseline living costs, you create a protective buffer between immediate needs and long-term wealth compounding.

Regarding your credit strategy, strategically utilize low-interest debt instruments to bridge temporary liquidity gaps rather than taking out dangerous workplace loans. On the broader investing front, your asset location strategy holds equal importance to your asset allocation; deliberately decide which investments belong in taxable accounts versus protected accounts to avoid devastating wash sales. Finally, securing robust consumer protections involves working with verified fiduciaries and thoroughly vetting all self-directed alternative investments to ensure you never cross the line into highly penalized transactions.

Expert Voices and Consumer Protection

Navigating the labyrinth of federal tax law requires professional guidance and a healthy dose of skepticism toward aggressive wealth-building schemes. According to guidance from the Consumer Financial Protection Bureau, older Americans frequently face targeting by predatory advisors pushing highly complex alternative investments within self-directed structures. These aggressive marketing schemes routinely gloss over the severe regulatory risks associated with prohibited transactions, opaque valuation metrics, and massive illiquidity. Certified Financial Planner professionals consistently warn against making major portfolio shifts based on unverified internet advice or high-pressure sales tactics. You should always demand full transparency regarding an advisor’s compensation structures and seek independent verification from a qualified tax professional before executing complex maneuvers like indirect rollovers. Protecting your vulnerable nest egg involves rigorous due diligence and relying on objective economic data rather than emotional market reactions.

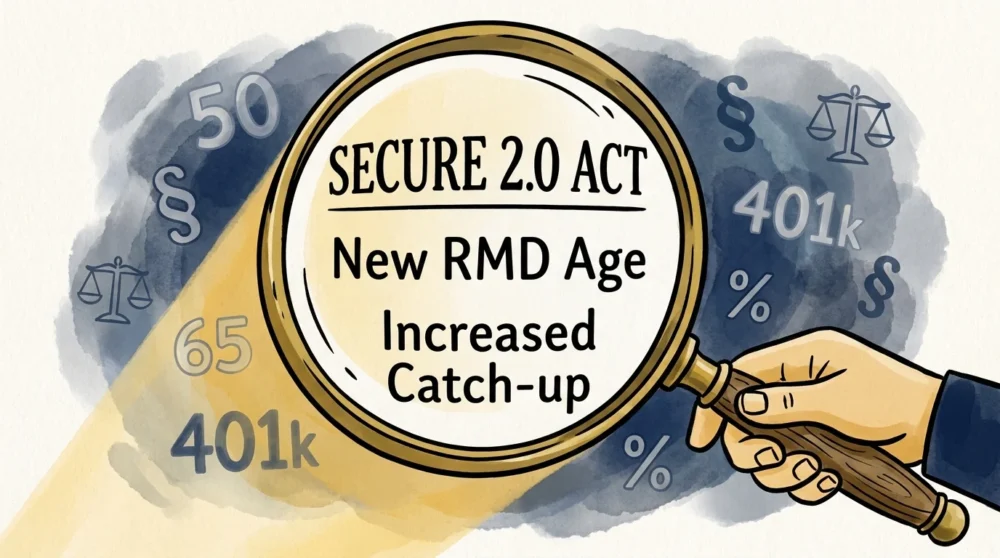

Risk and Compliance Changes You Need to Watch

The regulatory landscape governing your long-term savings constantly shifts, requiring you to remain consistently vigilant to avoid administrative compliance failures. The rollout of the SECURE 2.0 Act introduced complex, phased-in legislative changes that fundamentally impact American savers. One critical upcoming shift involves specific catch-up contributions for high-earning professionals; individuals making over a designated income threshold will soon legally need to direct catch-up contributions exclusively into after-tax accounts rather than traditional, pre-tax environments. Failing to proactively update your automated payroll deductions easily leads to disallowed contributions and administrative headaches. Furthermore, the IRS frequently updates the income phase-out ranges for specific tax deductions based on shifting inflation metrics. Thoroughly review your account settings annually and coordinate closely with your human resources department to ensure your automated investments align perfectly with the latest federal compliance standards.

Frequently Asked Questions

Readers often encounter highly specific financial scenarios that require nuanced interpretations of complex IRS rules. Below are four of the most common questions regarding account penalties and legal compliance.

Can I reverse an early withdrawal from my retirement account if I realize it was a mistake? Generally, you cannot undo a cash distribution once the financial institution officially disburses the funds. However, if you operate within the strict 60-day legal window, you can treat the withdrawal as an indirect rollover. You must deposit the identical gross amount into another qualified account to avoid impending taxes and penalties.

Does the IRS ever waive the financial penalty for missing a mandatory annual distribution? Yes, the IRS provides a specific mechanism for penalty relief if you successfully demonstrate that the financial shortfall occurred due to reasonable human error and that you are taking immediate steps to rectify it. You must file Form 5329 and attach a detailed letter explaining the issue that directly caused the delay.

Are inherited portfolios subject to the exact same early withdrawal penalties as standard individual accounts? No, the standard 10 percent early withdrawal penalty absolutely does not apply to distributions taken from an inherited portfolio, regardless of your current physical age. However, you still owe ordinary income tax on distributions taken from a traditional inherited account, and complex rules dictate when the account must be fully emptied.

How do I accurately report a corrected excess contribution on my annual tax return? If you remove an accidental excess contribution and its associated investment earnings before the federal tax filing deadline, you must report the earnings as taxable income for the year the original contribution occurred. Your financial institution issues a Form 1099-R detailing the exact corrective distribution amounts.

Your Next Steps for a Secure Retirement

Protecting your hard-won financial independence requires continuous oversight and proactive management of your investment accounts. Your immediate next step is conducting a comprehensive audit of your entire retirement portfolio. Log into your brokerage accounts today and strictly verify your year-to-date contribution totals to ensure you remain well under mandated IRS limits. Next, thoroughly review your assigned beneficiary designations and deliberately consolidate lingering accounts from former employers via direct, institution-to-institution transfers to drastically streamline your administrative oversight. If you are rapidly approaching your seventies, actively schedule a planning meeting with a fiduciary advisor to map out a precise withdrawal strategy that perfectly satisfies all federal distribution mandates. By taking deliberate control of your tax strategy today, you effectively fortify your household wealth against unnecessary government penalties. Do not let administrative oversights drain the wealth you spent a lifetime building; take decisive action this week to permanently safeguard your financial future.