Trusting someone with your life savings is one of the most critical financial decisions you make, yet many investors unknowingly lose thousands to hidden fees and conflicted advice. Identifying financial advisor warning signs early can rescue your retirement timeline and protect your hard-earned wealth from self-serving wealth managers. While a fiduciary is legally bound to put your financial needs first, a significant portion of the industry operates under looser suitability standards that allow them to push expensive, underperforming products. Whether you are balancing household budgets, paying down debt, or shifting into retirement, you need to recognize the subtle red flags indicating your advisor prioritizes their commissions over your financial security.

The Current Economic and Regulatory Landscape

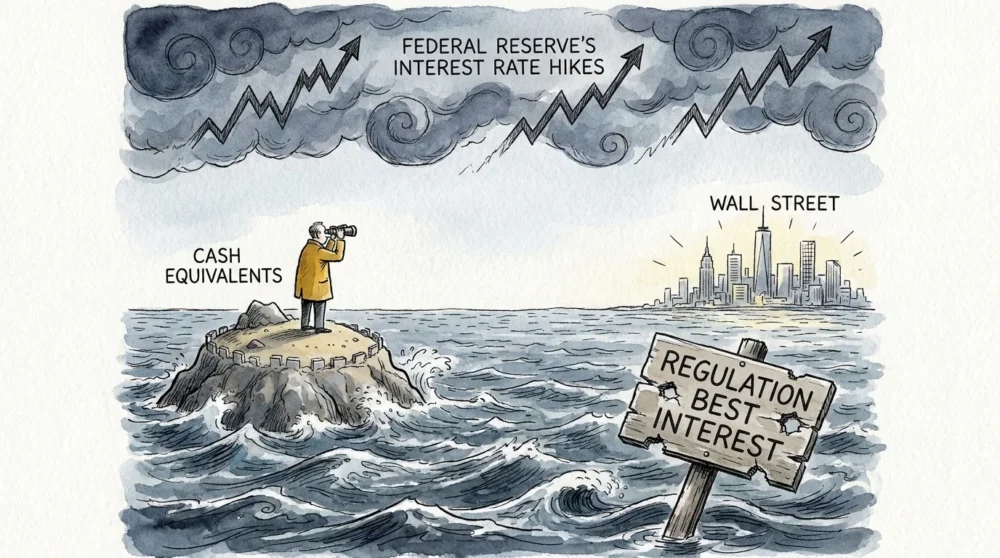

Navigating the modern financial ecosystem requires acute awareness of how economic shifts influence the advice you receive. Over the past few years, aggressive interest rate hikes by the Federal Reserve have dramatically altered the yield landscape, making cash equivalents and fixed-income assets more attractive than they have been in over a decade. Despite this favorable environment for conservative wealth preservation, many financial representatives continue steering clients toward complex, high-risk, and high-fee investment products. This disconnect often stems from a regulatory environment that still permits a dual-standard system of financial advice.

While the Securities and Exchange Commission implemented Regulation Best Interest to elevate the standards for broker-dealers, significant loopholes remain. Regulation Best Interest requires brokers to mitigate or disclose conflicts of interest, but disclosing a conflict does not eliminate the financial damage it inflicts on your portfolio. Wall Street thrives on informational asymmetry; brokerage firms generate billions in revenue by offering proprietary products and collecting revenue-sharing payments from mutual fund companies. As households face persistent inflation and work to maximize their limited discretionary income, understanding the precise legal obligations of your financial representative is your primary defense against wealth extraction.

Reason 1: They Exploit the Suitability Standard

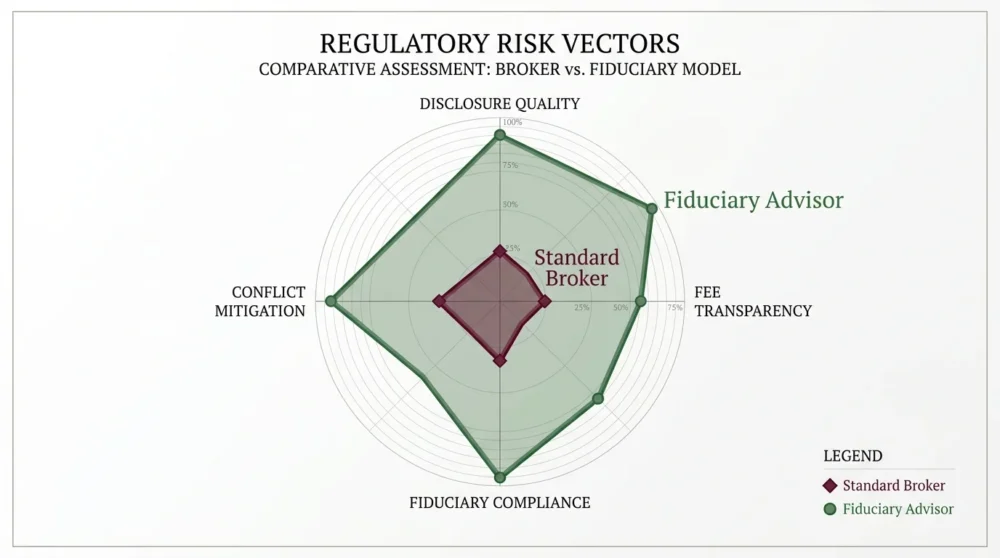

The single most important distinction in wealth management is the difference between a fiduciary and a broker operating under the suitability standard. A legally bound fiduciary must place your financial interests above their own at all times, recommending the most efficient and cost-effective solutions for your specific scenario. Conversely, many advisors are merely registered representatives of broker-dealers. They are only required to recommend investments that are broadly suitable for your age and income bracket, even if those investments pay them a massive commission and cost you significantly more than an available alternative.

Complicating matters further is the rise of the dual-registered advisor. These professionals carry licenses that allow them to act as a fiduciary in one meeting and a commissioned broker in the next. They might build your financial plan under a fiduciary standard and then conveniently switch hats to sell you a commissioned annuity to fund that exact plan. If your advisor refuses to sign a plain-language fiduciary oath covering all aspects of your relationship, they are keeping the door open to sell you out for higher payouts.

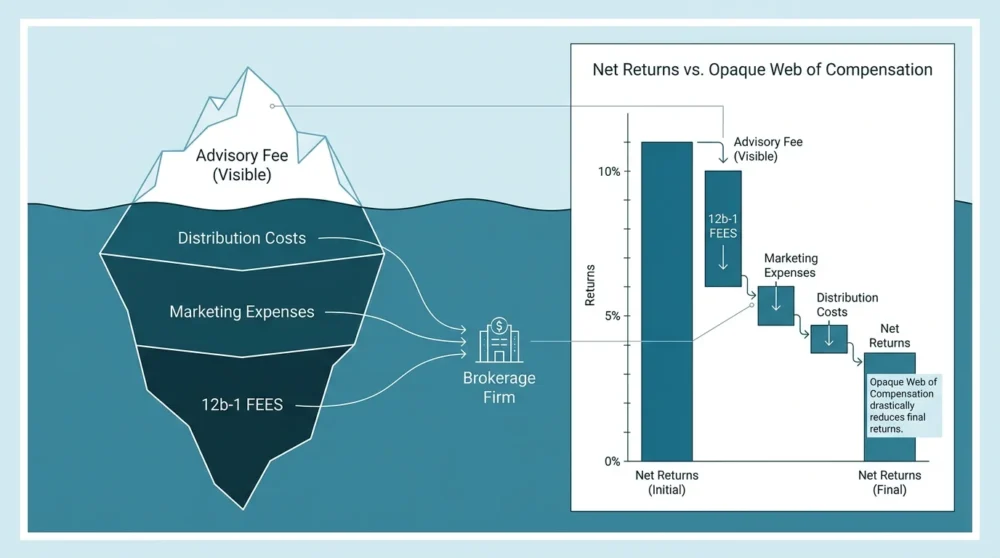

Reason 2: Their Compensation Relies on Hidden Fees

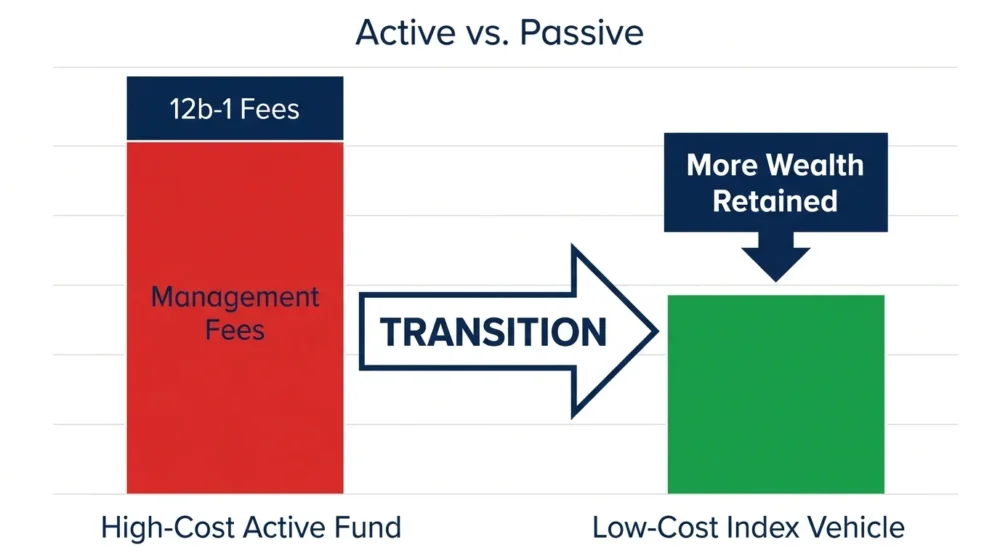

Transparent wealth managers charge a flat fee, an hourly rate, or a straightforward percentage of the assets they manage. Unethical advisors rely on an opaque web of back-end compensation that silently drains your returns. Many mutual funds carry 12b-1 fees—ongoing marketing and distribution expenses extracted directly from your investment balance and paid to your advisor’s firm. You never see a direct bill for these charges; they simply reduce your portfolio’s daily net asset value.

Consider a standard retirement portfolio of $500,000. If your advisor charges a 1.5 percent asset management fee and places you in mutual funds with an additional 1 percent expense ratio, you are surrendering 2.5 percent of your wealth annually. Over two decades, assuming a 7 percent baseline market return, those layered fees will siphon hundreds of thousands of dollars from your future net worth. When an advisor insists their services are virtually free or heavily discounted, they are almost certainly compensating themselves through these hidden structural drains.

Reason 3: They Push Proprietary Investment Products

Major brokerage houses frequently manufacture their own mutual funds, exchange-traded funds, and structured notes. When you sit across the desk from an advisor employed by one of these massive institutions, you are often subjected to a subtle, continuous sales pitch for their in-house products. This presents a massive conflict of interest; the advisor receives pressure from their corporate managers to drive client capital into proprietary funds to boost corporate revenues.

Proprietary funds frequently underperform their benchmark indexes while carrying higher expense ratios than identical funds available on the open market. Your advisor should act as an unbiased buyer traversing the entire investment universe to find the absolute best vehicles for your capital. If you review your monthly statement and notice that the majority of your holdings carry the exact same brand name as the firm holding your accounts, your advisor is operating as a corporate salesperson rather than an objective advocate.

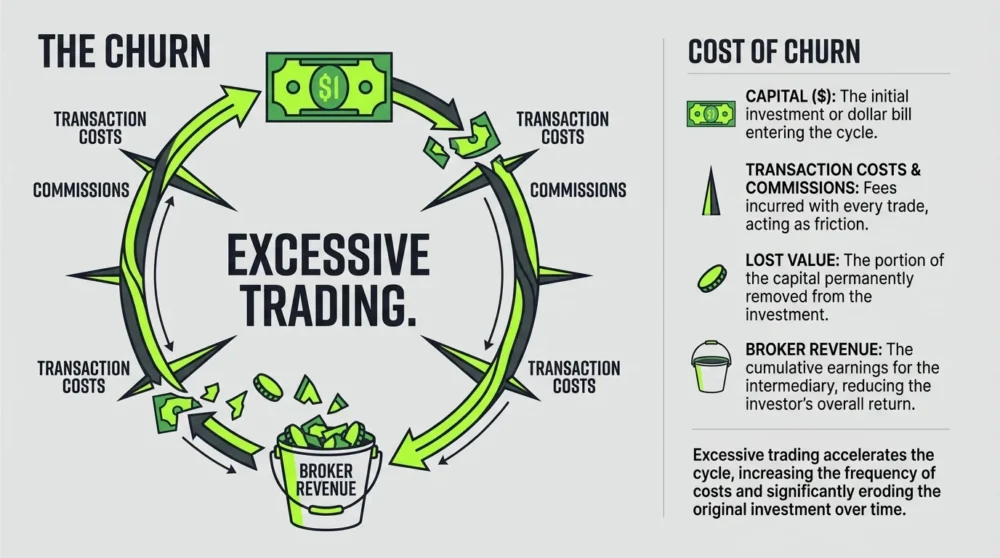

Reason 4: They Recommend Excessive and Unnecessary Trading

In traditional brokerage accounts, representatives generate income every time they execute a buy or sell order. This compensation structure inherently incentivizes churning—the unethical practice of rapidly trading assets in a client’s account solely to generate commissions. While regulatory bodies monitor for extreme cases of churning, subtle over-trading remains a pervasive issue that artificially inflates an advisor’s income while crushing your net returns through transaction costs and tax liabilities.

Even if you utilize a wrap-fee account where individual trades do not generate commissions, advisors often engage in unnecessary portfolio complexity to justify their ongoing management fee. They might divide your wealth across thirty different niche funds when a simple three-fund portfolio of broad market index funds would yield superior historical performance. This manufactured complexity ensures you feel completely reliant on their expertise, trapping you in a perpetual cycle of paying for an illusion of sophistication.

Reason 5: They Ignore Your Broader Household Balance Sheet

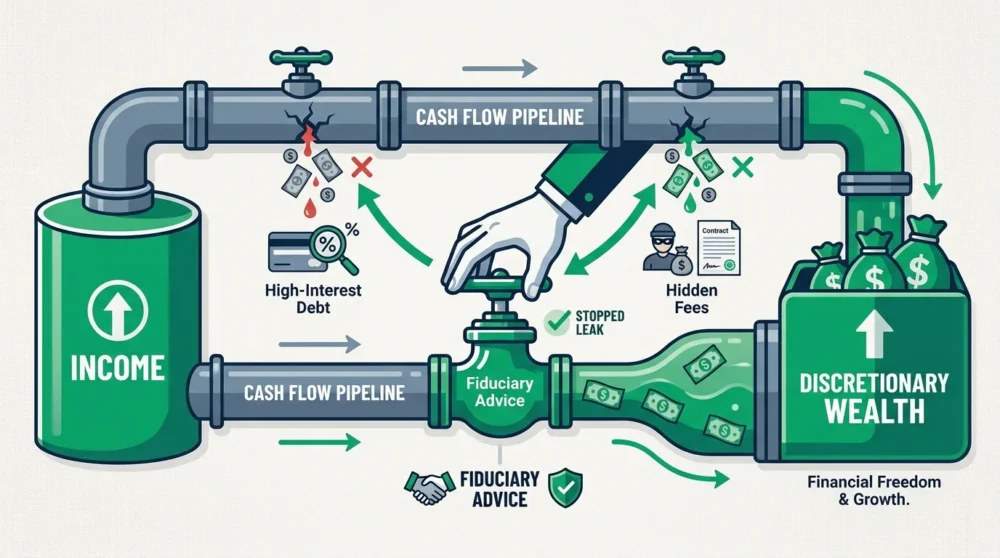

True financial planning encompasses every element of your financial life, from optimizing your emergency fund to accelerating your debt payoff strategy. A self-serving advisor exhibits tunnel vision, focusing entirely on the investable assets you can transfer to their direct management. Because their compensation is strictly tied to the assets under management, they have no financial incentive to advise you to pay off a burdensome 8 percent auto loan or a 24 percent annual percentage rate credit card balance.

If you ask your advisor whether you should liquidate a portion of your portfolio to eliminate high-interest household debt and they immediately push back to keep the assets invested, their motivations are compromised. A fiduciary recognizes that a guaranteed double-digit return realized by eliminating credit card debt is vastly superior to the speculative returns of the stock market. An advisor ignoring your liabilities is actively working against your long-term solvency.

Reason 6: They Target Older Adults with Aggressive Sales Tactics

Cognitive decline and the natural anxieties surrounding outliving one’s savings make older adults prime targets for predatory financial practices. When selecting a financial advisor trust seniors place in their representatives must never be exploited, yet unethical brokers frequently manipulate this dynamic. One of the most glaring seniors financial advisor red flags is the sudden, aggressive recommendation of complex, illiquid annuities tailored specifically to older clients.

These annuity contracts often feature staggering upfront commissions for the broker—sometimes reaching 7 to 10 percent of the total investment—while locking the client’s money into surrender periods that can last over a decade. If a senior needs to access their capital to pay for unexpected medical emergencies or assisted living facilities, they are penalized with exorbitant surrender fees. Advisors pushing these rigid products onto elderly clients are securing their own massive paydays at the direct expense of the client’s necessary liquidity.

Reason 7: They Are Evasive About Their Compensation Structure

Clarity is the bedrock of any successful professional relationship. You possess the absolute right to know exactly how much money your financial professional earns from your account each year, expressed in actual dollar amounts rather than vague percentages. If your representative dismisses your concerns about underperformance, shifts the conversation when asked about kickbacks, or refuses to explain their compensation in plain language, you have an advisor not working for you.

Ethical professionals gladly provide a transparent breakdown of their management fees, trading costs, and underlying fund expenses. They deliver this information in writing and welcome your scrutiny. Evasive behavior, gaslighting, or claims that the financial markets are simply too complex for you to understand are deliberate tactics designed to maintain an imbalanced power dynamic. You are the employer in this relationship; if the employee refuses to provide a clear invoice, it is time to terminate their services.

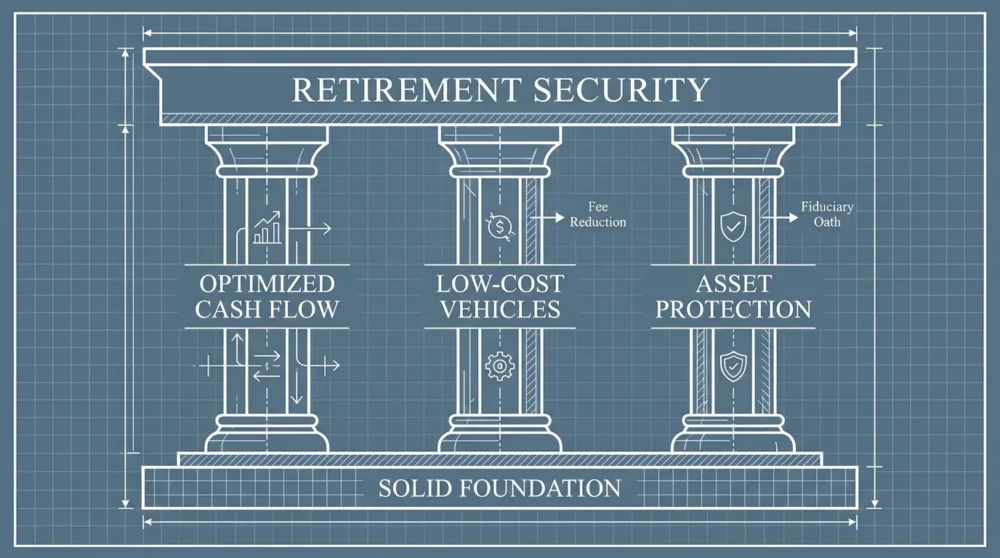

Strategy Pillars for Course Correction

Optimizing Cash Flow and Debt Management

Reclaiming control of your financial trajectory begins with integrating your investment strategy into your daily cash flow and debt management. Stop viewing your investment portfolio as an isolated bucket of money. Calculate the carrying cost of all your household liabilities, paying special attention to variable-rate credit cards and personal loans. Divert excess capital away from taxable brokerage accounts charging management fees and directly assault your high-interest debt. By extinguishing a debt carrying a 10 percent interest rate, you secure a guaranteed, tax-free return on your capital that no financial advisor can reliably match in the public equity markets.

Transitioning to Low-Cost Investment Vehicles

Once you stabilize your household balance sheet, transition your wealth-building strategy toward high-efficiency, low-cost investment vehicles. Academic research and economic consensus overwhelmingly demonstrate that actively managed mutual funds fail to outperform basic market indexes over long time horizons. Fire your commissioned broker and migrate your assets into broad-market index funds or exchange-traded funds. If you require professional guidance for complex tax planning or estate organization, hire a fee-only, flat-rate fiduciary. You will purchase objective advice by the hour, eliminating the structural incentive for the advisor to endlessly churn your portfolio or hoard your assets.

Establishing Institutional Asset Protection

You must sever the physical custody of your wealth from the individual providing the advice. Never write a check directly to an independent financial advisor’s personal or corporate LLC account. Legitimate advisors require you to house your assets at a major, third-party discount brokerage firm—such as Charles Schwab, Fidelity, or Vanguard—while granting the advisor limited trading authorization. This institutional separation guarantees that your advisor can execute trades on your behalf but cannot physically withdraw funds or transfer your assets to unauthorized accounts. This structural firewall is non-negotiable for safeguarding your life savings.

Navigating Risk and Regulatory Compliance

Protecting your household from financial exploitation requires an aggressive stance on compliance verification and background research. The financial services industry is highly regulated, but enforcement heavily relies on consumer reporting and personal vigilance. To actively protect money from advisor mismanagement, you must routinely audit your account statements for unauthorized trading and hidden fee deductions. Demand that your advisor provide their Form ADV Part 2A—a legally required disclosure document filed with the government that details their specific fee structures, conflicts of interest, and disciplinary history.

If you discover that your representative has a history of regulatory infractions, customer disputes, or questionable bankruptcies, you must act decisively. Utilize the FINRA BrokerCheck database to investigate your advisor’s permanent record before signing any account transfer paperwork. Furthermore, families must proactively safeguard their elderly members from predatory exploitation. The Consumer Financial Protection Bureau explicitly warns that elder financial abuse frequently originates from trusted professionals. Establish a trusted contact person on all senior investment accounts to ensure the brokerage firm has an independent family member to notify if suspicious, uncharacteristic withdrawals or high-commission product purchases occur.

Expert Perspectives on Fiduciary Duty

Leading economists and consumer advocates maintain a unified stance regarding the critical importance of a fiduciary standard. Representatives from the Certified Financial Planner Board of Standards strictly enforce a duty of loyalty and a duty of care, meaning their credentialed professionals must actively avoid conflicts of interest and disclose any unavoidable conflicts transparently. According to prominent academic studies published in major financial journals, the compounded drag of conflicted, high-fee advice can reduce a household’s total retirement wealth by over 20 percent compared to optimized, low-cost index investing. Financial consumer advocates strongly advise investors to demand a signed fiduciary pledge before committing a single dollar, reinforcing that verbal promises hold absolutely no legal weight when an advisor decides to pivot into a high-commission sales pitch.

Frequently Asked Questions

How do I reliably verify if my advisor is a legal fiduciary?

You verify their legal standing by demanding written documentation. Do not accept verbal assurances. Ask the advisor to provide and sign a fiduciary oath stating they will act as a fiduciary for all aspects of your account at all times. Additionally, use the SEC’s Investor.gov portal to review their Form ADV, which explicitly outlines their business practices, their precise registration status, and whether they accept third-party compensation for recommending specific products.

What should I do if I suspect my advisor is overcharging me?

Immediately request a comprehensive, written breakdown of all fees you paid over the past calendar year expressed in total dollars. This must include direct management fees, transaction costs, and all underlying fund expense ratios. If the total drag exceeds 1 percent of your total assets, or if the advisor refuses to provide a clear dollar amount, halt all new contributions. Open a self-directed account at a major discount brokerage and initiate a direct transfer of your assets.

Can I transfer my investments to a new institution without paying massive penalties?

In most standard brokerage and individual retirement accounts, you can transfer your investments directly to a new firm using an Automated Customer Account Transfer Service without liquidating your holdings. However, if your current advisor trapped you in proprietary funds or complex annuities with surrender charges, you may face tax consequences or early withdrawal penalties to escape those specific products. A fee-only fiduciary can help you analyze the mathematical breakeven point to determine if taking the penalty now is cheaper than paying the hidden fees for another decade.

What protections exist to help older adults combat financial exploitation?

Federal and industry regulations mandate several protective mechanisms for vulnerable adults. Financial institutions are required to ask clients to name a trusted contact—a person the firm can reach out to if they suspect the client is experiencing cognitive decline or active financial exploitation. Furthermore, under FINRA Rule 2165, broker-dealers possess the authority to place temporary holds on disbursements of funds or securities if they maintain a reasonable belief that financial exploitation of a senior investor is occurring or has been attempted.

Next Steps for Securing Your Wealth

Taking control of your financial destiny requires immediate, deliberate action to sever ties with conflicted advisors. Begin by logging into your investment portal today and downloading your most recent quarterly statement to identify exactly what you are paying in management fees and underlying fund expenses. Next, draft a direct email to your current financial representative asking them to clarify their fiduciary status in writing and requesting a dollar-amount summary of their compensation. If their response is evasive, defensive, or overly complicated, start interviewing fee-only, hourly fiduciaries to build a transition plan. Finally, initiate an institutional transfer of your assets to a discount broker, permanently locking predatory salespeople out of your retirement timeline and securing your capital for the future.