If you are turning 73 this year, you face a critical financial milestone that requires immediate action. Required minimum distributions force you to withdraw specific amounts from your retirement accounts annually. The IRS heavily monitors these mandatory distributions. A single misstep can trigger an excise penalty that drains up to 25 percent of your required withdrawal. Thousands of retirees accidentally forfeit their savings every year by miscalculating deadlines, confusing account aggregation rules, or misinterpreting the latest legislative guidelines. Protecting your wealth demands a proactive strategy that integrates tax planning and strict regulatory compliance. You must recognize and avoid these eight distribution traps to preserve your hard earned nest egg and keep your retirement timeline completely intact.

The New Economic Reality of Retirement Withdrawals

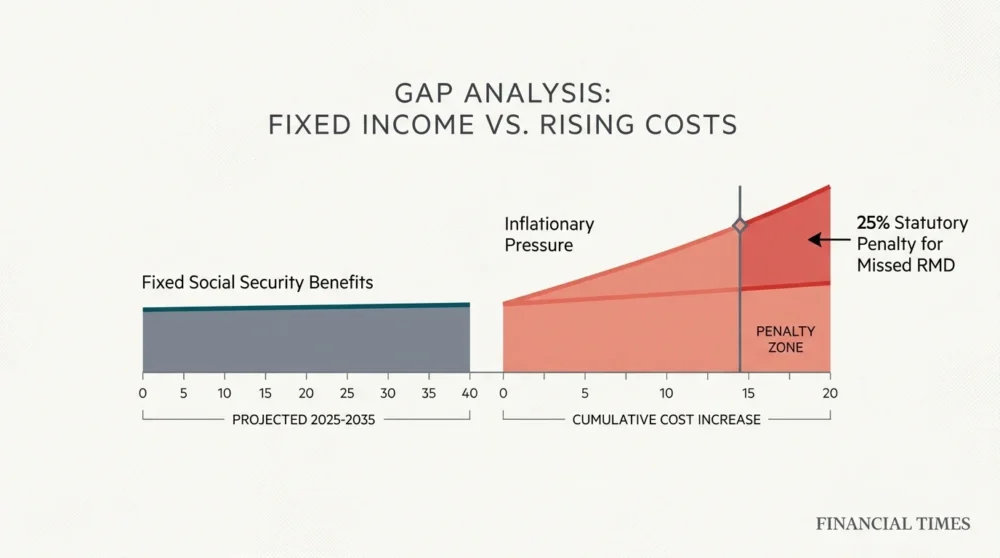

The macroeconomic environment significantly amplifies the consequences of distribution errors. The Bureau of Labor Statistics notes that the Consumer Price Index continually highlights how inflation pressures household budgets and erodes long-term purchasing power. This persistent economic backdrop makes every dollar in your retirement account vital for your ongoing stability. Federal Reserve data routinely demonstrates that retirees depend heavily on their tax-advantaged investment portfolios to bridge the substantial gap between fixed Social Security benefits and actual daily living expenses.

When you combine sustained inflationary pressures with a baseline 25 percent statutory penalty for a missed withdrawal, an administrative error can cost you thousands of dollars in lost wealth. Financial planning in 2026 requires more than simply choosing profitable mutual funds; it requires precise tax engineering. Optimizing your cash flow strategy and understanding the rapidly evolving legislative framework ensures you maintain essential liquidity without surrendering your accumulated wealth to avoidable taxes or steep regulatory penalties. A proactive approach transforms these mandatory distributions from a tax burden into a structured component of your comprehensive wealth management plan.

Mistake 1: Ignoring the April 1 Trap for Your First Distribution

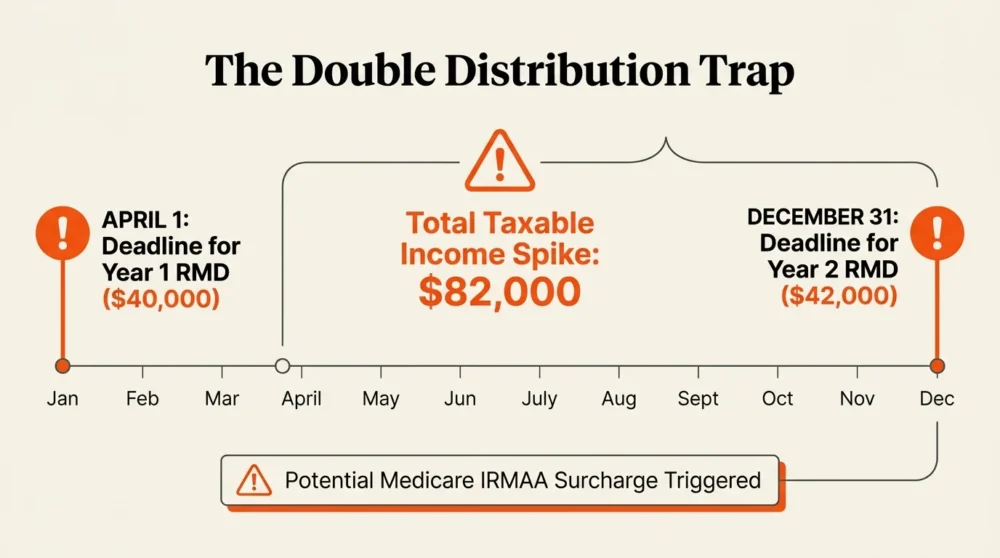

The IRS gives you until April 1 of the year following your 73rd birthday to take your inaugural withdrawal. On the surface, this sounds like an excellent grace period that allows your investments more time to compound tax-deferred. However, deferring your first payment triggers a dangerous tax trap; it forces you to take two distributions in the exact same calendar year. Your delayed first distribution covers your inaugural year, while your second distribution covers the current year and remains strictly due by December 31.

Taking two mandatory withdrawals in a single twelve-month window artificially spikes your adjusted gross income. Consider a scenario where your required annual withdrawal equals $40,000. If you delay your first payment, you must also withdraw your second required distribution—perhaps $42,000—by December 31 of that same year. You suddenly add $82,000 to your taxable income. This artificial income surge easily pushes you into a higher marginal tax bracket and frequently triggers Medicare Income-Related Monthly Adjustment Amount surcharges, dramatically increasing your healthcare premiums. You must calculate the exact tax impact of delaying your first withdrawal before accepting the April 1 extension.

Mistake 2: Combining 401(k) and IRA Calculations Incorrectly

Retirees often hold multiple retirement accounts accumulated across decades of employment and various financial institutions. The IRS allows you to calculate the distribution for each traditional IRA you own, add the respective totals together, and withdraw the aggregate amount from just one of those IRA accounts. This specific flexibility greatly simplifies your cash flow management and consolidates your taxable events into a single, highly trackable transaction.

Unfortunately, many retirees mistakenly assume they can apply this convenient IRA aggregation rule to their employer-sponsored plans. The tax code strictly prohibits aggregating 401(k) or 403(b) distributions. If you possess three different 401(k) accounts from previous employers, you must independently calculate and withdraw the exact required amount from each specific account separately. Mixing these distinct mathematical rules results in a massive shortfall for your employer plans. If you accidentally take the combined sum from just one 401(k), the IRS views the other accounts as severely delinquent, triggering immediate excise taxes on the deficit.

Mistake 3: Overlooking the Workplace Exemption Nuances

If you choose to continue working past age 73, you might logically assume you can delay all your mandatory distributions until you officially retire. The IRS does provide a “still working” exception, but it applies very narrowly and traps thousands of unsuspecting employees who misunderstand the boundary lines. You can only delay distributions from the specific 401(k) plan sponsored by your current, active employer.

Your traditional IRAs, SEP IRAs, and any 401(k) accounts left behind at former employers remain entirely subject to standard withdrawal deadlines regardless of your current employment status. Furthermore, this workplace exemption disappears entirely if you own more than 5 percent of the company employing you. Business owners, equity partners, and key shareholders must begin their withdrawals at age 73 even if they work full time. Review your equity ownership stakes and account classifications meticulously to ensure you do not inadvertently skip a legally required payment.

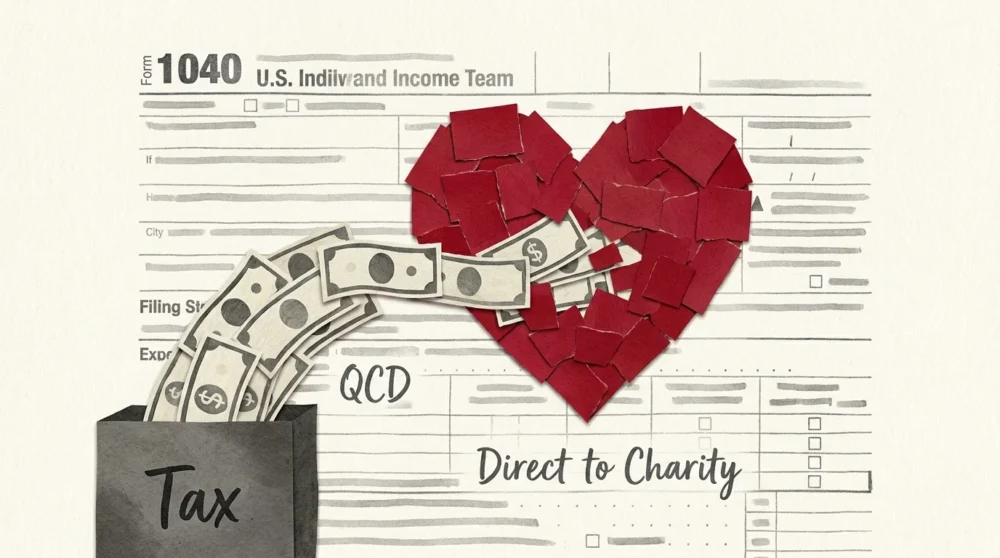

Mistake 4: Missing the Qualified Charitable Distribution Opportunity

The government aggressively taxes traditional retirement account withdrawals as ordinary income, significantly diminishing the actual cash you retain. You can completely neutralize this specific tax liability by directing your distribution straight to an eligible charity. A Qualified Charitable Distribution allows you to transfer up to $111,000 in 2026 directly from your IRA to a qualifying nonprofit organization. This strategic transfer fully satisfies your annual distribution requirement without adding a single dollar to your adjusted gross income.

Lowering your gross income protects you from secondary taxes on your Social Security benefits and keeps your future Medicare premiums entirely in check. However, retirees frequently botch the execution. They withdraw the cash first, deposit it into their personal checking accounts, and then write a personal check to the charity. This routing mistake instantly transforms the withdrawal into taxable income, irreversibly destroying the tax benefit. You must formally instruct your custodian to send the funds directly to the charity to successfully claim this powerful tax advantage.

Mistake 5: Failing to Adjust for Inherited IRA Mandates

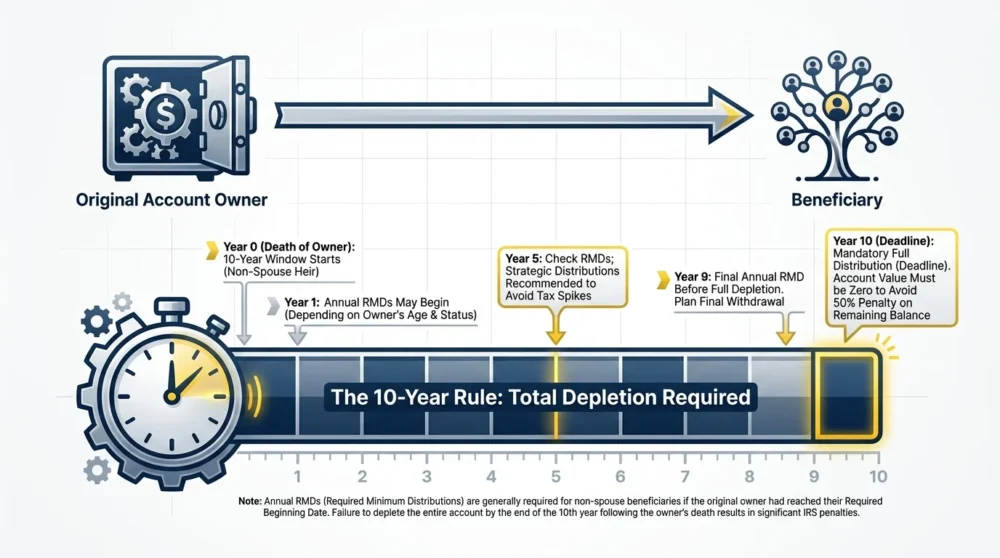

Inheriting a retirement account introduces a labyrinth of secondary rules that completely bypass standard distribution logic. The SECURE 2.0 Act radically altered the financial regulations surrounding inheritance for non-spouse beneficiaries. If you inherit an IRA today, you generally must empty the entire account within ten years of the original owner’s death. This decade-long countdown requires careful tax modeling to avoid massive tax liabilities in year ten.

The trap deepens based on the deceased owner’s age. If the original owner had already reached their mandatory withdrawal age before passing away, you must also take annual distributions during years one through nine of that ten-year window. Neglecting these interim withdrawals results in severe regulatory penalties. Spouse beneficiaries enjoy completely different privileges and can often treat the inherited account as their own, delaying withdrawals until they personally reach age 73. You must definitively identify your exact beneficiary classification to execute the correct withdrawal timeline and avoid unnecessary tax erosion.

“A hand uses a fountain pen to fill out the waiver section on IRS Form 5329.”

16 words.

Let’s try:

“A hand uses a fountain pen to complete the waiver section on IRS Form

Mistake 6: Paying the Excise Penalty Without Requesting a Waiver

Missing a distribution deadline triggers a 25 percent excise tax on the precise amount you failed to withdraw. The IRS automatically lowers this penalty to 10 percent if you correct the error within a two-year window. Remarkably, you can often eliminate the financial penalty entirely by formally requesting a waiver. The IRS frequently grants administrative leniency for oversights caused by serious illness, cognitive decline, family emergencies, or explicitly terrible advice from a financial institution.

Instead of simply paying the steep fine out of guilt or panic, you should immediately withdraw the missed amount and file Form 5329 alongside your tax return. Attach a concise, factual letter explaining the reasonable cause behind your mistake and clearly outlining the rapid steps you took to correct it. Certified Financial Planner professionals consistently advise clients never to concede a massive penalty without fighting for a statutory waiver first, as the IRS processes these requests with surprising understanding when presented logically.

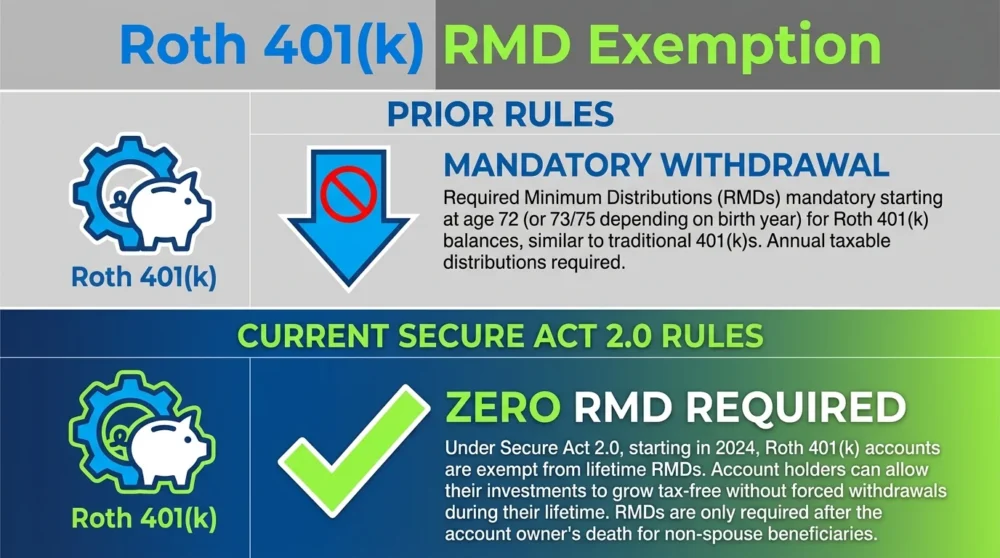

Mistake 7: Misunderstanding Roth 401(k) Rule Changes

Roth IRAs provide incredible flexibility because they never demand mandatory distributions during the original owner’s lifetime. Historically, Roth 401(k) accounts did not share this vital protection, forcing retirees to empty their tax-free employer accounts prematurely and disrupt their compounding growth. Fortunately, recent legislative updates eliminated this frustrating discrepancy across retirement accounts.

Starting in 2024, the government officially abolished mandatory distributions for Roth 401(k) plans. Despite this highly publicized legislative update, many retirees continue draining their Roth employer plans unnecessarily simply out of habit or bad advice. Leaving those funds untouched allows your investments to generate tax-free compound growth for your heirs. You must audit your account structures immediately and halt any automated distributions from your Roth 401(k) unless you actually need the capital for your daily living expenses.

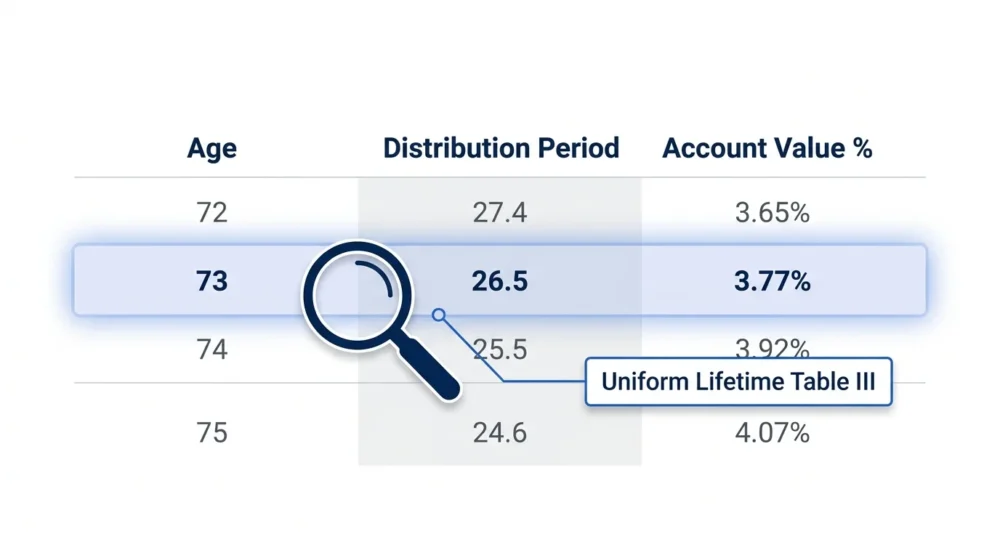

Mistake 8: Using the Wrong Life Expectancy Table

The exact dollar amount of your mandatory withdrawal changes every single year based on statistical life expectancy calculations. The IRS publishes three separate life expectancy tables, and choosing the wrong one guarantees a mathematical error that will invite regulatory scrutiny. Most unmarried retirees and married couples of similar ages must strictly use the Uniform Lifetime Table to determine their specific withdrawal mandate.

However, if your spouse is the sole primary beneficiary of your account and happens to be more than ten years younger than you, you must use the Joint Life and Last Survivor Expectancy Table. This alternative table significantly reduces your annual required payout, keeping substantially more money sheltered in your tax-deferred account where it can continue growing. Calculating your obligation with outdated data or incorrect longevity metrics leaves you vulnerable to underpayment penalties or unnecessary, accelerated taxation.

Regulatory Protections and Avoiding Scams

Navigating this complex compliance landscape demands intense vigilance against both regulatory missteps and outright financial fraud. Scam artists frequently target older adults during tax season with aggressive marketing pitches promising secret loopholes to eliminate distribution requirements entirely. According to the consumer protection resources provided by the CFPB, these malicious schemes often involve transferring your hard-earned funds into high-fee, illiquid annuities or fraudulent offshore accounts.

You must firmly recognize that the IRS offers no secret, unlisted exemptions beyond the clearly defined statutory rules. Furthermore, you must independently verify that your financial institution calculates your distribution accurately. While many brokerages offer automated calculation tools, the ultimate legal liability rests entirely on your shoulders, not your brokerage firm. Always independently verify regulatory thresholds, utilize official government worksheets, and consult a fiduciary advisor before moving substantial assets or adopting complex tax avoidance strategies.

Frequently Asked Questions

Can I put my required minimum distribution back if I do not need the money?

No, you generally cannot return the distribution to your tax-deferred retirement account once it executes. The government mandates these withdrawals specifically to tax the capital, and rolling the funds back into a traditional IRA directly violates tax laws. However, if you do not need the cash for immediate living expenses, you can reinvest the money into a standard taxable brokerage account. While the initial withdrawal remains fully taxable, redirecting the capital into a taxable account allows you to keep your wealth invested in the market rather than sitting idle in a checking account.

Do I have to take distributions from my Roth IRA?

If you are the original owner of a Roth IRA, you never have to take required minimum distributions during your lifetime. The funds can remain in the account indefinitely, continuing to grow tax-free. This protection makes Roth IRAs incredibly powerful estate planning tools. However, if you inherit a Roth IRA from someone else, you will likely face distribution mandates depending on your relationship to the deceased and the specific rules enacted under the SECURE 2.0 Act.

What happens if my distribution falls during a severe market downturn?

You must still withdraw the required monetary amount regardless of broader market conditions. The IRS calculates your mandate based on your account balance at the end of the previous calendar year, not the current market value. Selling assets during a downturn locks in permanent losses. To mitigate this damage, you can utilize an in-kind distribution. This strategy involves moving shares of stock or mutual funds directly from your IRA to a taxable brokerage account without selling them. You still owe taxes on the monetary value of the transferred shares, but you avoid liquidating your positions at market bottoms.

How does a mandatory distribution affect my Medicare premiums?

Because traditional retirement withdrawals count as ordinary income, they directly increase your modified adjusted gross income. Medicare calculates your Part B and Part D premiums based on your income from two years prior. If your mandatory withdrawal pushes your income above specific regulatory thresholds, Medicare imposes an Income-Related Monthly Adjustment Amount. This surcharge can significantly increase your healthcare costs. Proactive tax planning, such as utilizing charitable transfers or strategic Roth conversions earlier in retirement, helps manage your taxable income and control future Medicare premiums.

Your Next Steps to Protect Your Retirement Income

Taking control of your retirement distributions requires immediate and precise action. Start by cataloging every tax-deferred account to your name, noting the specific custodian, account classification, and current market balance. Download the correct IRS life expectancy table and calculate your baseline distribution target for the current calendar year. Review your designated beneficiaries to ensure your wealth transfer strategy completely aligns with the latest SECURE 2.0 Act regulations.

Next, analyze your projected tax bracket with a qualified professional and evaluate whether a direct charitable transfer makes sense for your household cash flow. Finally, automate your required withdrawals well before the December deadline to completely eliminate the risk of a catastrophic late penalty. By executing these proactive steps today, you secure your financial independence, maintain your critical liquidity, and keep your retirement assets exactly where they belong.